Commission, December 21, 2017, No M.8633

EUROPEAN COMMISSION

Decision

LUFTHANSA / CERTAIN AIR BERLIN ASSETS

To the notifying party:

Dear Sir or Madam,

Subject: Case M.8633 – LUFTHANSA / CERTAIN AIR BERLIN ASSETS Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

1. INTRODUCTION

(1) On 31 October 2017, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Deutsche Lufthansa AG ("Lufthansa", Germany) would acquire within the meaning of Article 3(1)(b) of the Merger Regulation control of the whole of NIKI Luftfahrt GmbH ("NIKI", Austria) and Luftfahrtgesellschaft Walter mbH ("LGW", Germany), by way of purchase of shares from Air Berlin plc ("Air Berlin").3 Prior to the closing of the acquisition, additional aircraft, crew and an airport slot4 package would be transferred from Air Berlin to LGW. These operations were to take place in the context of Air Berlin's insolvency proceedings, initiated on 15 August 2017.

(2) On 13 December 2017, Lufthansa decided not to acquire NIKI, pursuant to a clause in the sale and purchase agreement allowing Lufthansa to exclude, inter alia, NIKI from the acquisition, notably if, in Lufthansa's reasonable assessment, the acquisition would not be approved by the relevant competition authorities by 29 December 2017.5 As a result of this modification, the proposed concentration no longer included the acquisition of NIKI, but only the acquisition by Lufthansa of all shares in LGW and of additional aircraft, crew and an airport slot package that would be transferred from Air Berlin to LGW prior to closing (the "Transaction"). Lufthansa and LGW are collectively referred to as the "Parties".

(3) The slots that would be transferred by Air Berlin to LGW and, subsequently, to Lufthansa include slots at Zurich airport, thus affecting air transport in Switzerland. The bilateral Agreement between the European Union and the Swiss Confederation on Air Transport ("the ATA")6 gives the Commission the power to control concentrations between undertakings which may affect air transport in Switzerland.

2. THE PARTIES

(4) Lufthansa is the holding company of Lufthansa Group which is headquartered in Cologne, Germany. Lufthansa's passenger air transport business includes Lufthansa Passenger Airlines, Swiss International Air Lines Ltd., Brussels Airlines S.A./N.V., Austrian Airlines AG ("Austrian"), Air Dolomiti S.p.A., Eurowings GmbH ("Eurowings"), Germanwings GmbH ("Germanwings"), Edelweiss Air AG and SunExpress Deutschland GmbH ("SunExpress").7

(5) Lufthansa is also a member of Star Alliance,8 which includes Adria Airways, Aegean Airlines, Air Canada, Air China, Air India, Air New Zealand, All Nippon Airways, Asiana, Austrian Airlines, Avianca, Brussels Airlines, Copa Airlines, EgyptAir, Ethiopian Airlines, EVA Air, LOT Polish Airlines, Scandinavian Airlines, Shenzhen Airlines, Singapore Airlines, South African Airways, Swiss International Air Lines, TAP Portugal, Thai Airways, Turkish Airlines and United Airlines.

(6) Lufthansa is Germany's, Austria's and Switzerland's largest airline by both passenger numbers and revenue and it is Europe's largest airline by revenue. It operates flights to 301 destinations in 100 countries, with a fleet of about 600 aircraft. Lufthansa's principal hubs for international operations are at Brussels, Frankfurt, Munich, Vienna and Zurich airports. Lufthansa also has a number of bases across the world. In 2016, Lufthansa carried approximately 109.6 million passengers.

(7) LGW is a wholly-owned subsidiary of Air Berlin, which was Germany's second-largest airline, after Lufthansa. Air Berlin filed for insolvency on 15 August 2017 and ceased operations on 28 October 2017. Although Air Berlin entered into insolvency proceedings on 15 August 2017, its subsidiaries LGW and NIKI did not. LGW is still solvent, while NIKI9 filed for insolvency on 13 December 2017.

(8) LGW is headquartered in Dortmund, Germany, and operated 18 Dash 8 Q400 turbo-prop aircraft that were wetleased to Air Berlin and served short-haul routes into Duesseldorf and Berlin Tegel airports. LGW's role in the Air Berlin group was primarily to provide feeder traffic for Air Berlin's short and long-haul operations. Its aircraft were deployed where demand was not sufficient for larger aircraft, be it because of limited overall traffic on the route or because demand for a particular time (e.g. in the early afternoon) was limited. On 28 October 2017, when Air Berlin ceased its operations, LGW stopped operating its aircraft as a wetlessor for Air Berlin.

3. THE OPERATION

(9) On 13 October 2017, Lufthansa entered into an agreement to purchase all shares in LGW and NIKI and other assets and rights from Air Berlin.10 As explained in paragraph 2, on 13 December 2017, the scope of the acquisition was modified and, as a result, the Transaction was limited to the acquisition by Lufthansa of all shares in LGW and the additional aircraft, crew and airport slots that would be transferred to LGW prior to closing.

(10) Prior to closing of the acquisition, Air Berlin would transfer to LGW up to […] A320 aircraft and corresponding crew, as well as airport slots at notably Duesseldorf, Hamburg, Munich, Berlin Tegel and Zurich airports, which are further described in the next paragraph. As a result of the Transaction, Lufthansa would also acquire the aircraft, crew and airport slots that would have thus been transferred to LGW.11

(11) The slots that would be transferred by Air Berlin to LGW are slots for the Winter 2017/18 IATA12 Season and the Summer 2018 IATA Season. They consist of two different groups of slots. One group is made up of the slots that were held by Air Berlin but used by LGW for its flights with the Dash 8 Q400 turbo-prop aircraft before Air Berlin ceased operations on 28 October 2017 (the "LGW slots"). The second group is made up of some of the slots that were held by Air Berlin and used by Air Berlin (not LGW) on various routes, including in particular slots at Duesseldorf and Berlin Tegel airports, before Air Berlin ceased its operations (the "surplus slots").

(12) According to Lufthansa, the acquisition of LGW is designed to ensure continuity of the cooperation between Air Berlin and Lufthansa (through its subsidiaries Eurowings and Austrian) under the wetlease agreement established in December 2016 (the "Roof Wetlease"). Under the Roof Wetlease, Air Berlin is leasing a total of […] crewed aircraft to Eurowings ([…] aircraft) and Austrian ([…] aircraft). In addition, Air Berlin leases […] spare aircraft to Eurowings. The Roof Wetlease did not confer any slots or other assets to Lufthansa in relation to these […] aircraft. The overall term of the Roof Wetlease was intended to run for up to […] years. Under the Transaction, LGW will be the vehicle which will continue to operate the flight programme currently served under the Roof Wetlease.13

4. THE CONCENTRATION

(13) As a result of the Transaction, Lufthansa would acquire sole control over LGW and the aircraft, crew and slots that have been transferred to it. LGW is a legal entity which operates aircraft and has an operating licence, including an air operator's certificate (AOC), allowing it to operate these aircraft. LGW did not hold any slots but used Air Berlin's slots for its operations. However, the slots transferred to LGW by Air Berlin, together with the other transferred assets and resources, would form part of the undertaking that would, subject to compliance with the Slot Regulation, be acquired by Lufthansa. Together, the legal entity LGW and the assets, resources and rights transferred to it prior to closing constitute a business with a market presence, to which a market turnover can clearly be attributed. LGW and the additional aircraft, crew and slots that would be transferred to it thus constitute an undertaking or part of an undertaking within the meaning of the Merger Regulation.

(14) The Transaction therefore constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

(15) On 10 October 2017, Lufthansa requested, pursuant to Article 7(3) of the Merger Regulation, a derogation from the suspension obligation provided for in Article 7(1) of the Merger Regulation. More specifically, Lufthansa requested that it be allowed to replace Air Berlin as dry lessee of several aircraft (or to purchase them), to avoid that the lessors of these aircraft would repossess the aircraft because of Air Berlin's failure to pay the amounts due under the lease agreements. In addition, Lufthansa requested that it be allowed to enter into wetlease agreements with LGW and NIKI as lessors and Lufthansa as lessee. This way, LGW and NIKI would be able to perform the services performed by Air Berlin under the Roof Wetlease.

(16) On 27 October 2017, the Commission granted a derogation on the basis of Article 7(3) of the Merger Regulation, subject to conditions aimed at ensuring that the measures taken by Lufthansa would not negatively affect NIKI and LGW or make it more difficult for NIKI and LGW to be sold, in whole or in parts, to any other buyers, should this happen in the future.14

5. EU DIMENSION

(17) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (Lufthansa: EUR 31 660 million; LGW and NIKI combined: EUR […] million).15 Each of them has an EU-wide turnover in excess of EUR 250 million (Lufthansa: EUR […] million; LGW and NIKI combined: EUR […] million),16 and they do not achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State.

(18) The Transaction therefore has an EU dimension within the meaning of Article 1(2) of the Merger Regulation.

(19) On 13 December 2017, Lufthansa decided not to acquire NIKI. The Transaction therefore changed from an acquisition of control over LGW and NIKI to an acquisition of control over LGW alone. The Transaction, which was modified by Lufthansa after the notification, remains within the Commission's jurisdiction. It follows from the principles underlying the Merger Regulation (importantly, the principle of a clear division of competences between the authorities of the Member States and the Commission), that partial amendments to the contemplated transaction occurring after the notification of a transaction cannot require the Commission to re-examine its competence. As the Court of Justice has ruled,

"the competence of the Commission to make findings in relation to a concentration must be established, as regards the whole of the proceedings, at a fixed time. Having regard to the importance of the obligation of notification in the system of control put in place by the Community legislature, that time must necessarily be closely related to the notification of the concentration." 17

(20) This avoids that the Commission's competence, once established, can be challenged at any time or be in a state of constant flux.18

(21) According to the Commission's Consolidated Jurisdictional Notice, the relevant date for establishing the Commission's jurisdiction over a concentration is the date of the conclusion of the binding legal agreement, the announcement of a public bid or the acquisition of a controlling interest or the date of the first notification, whichever date is earlier.19 Since the Transaction had an EU dimension at the time of the conclusion of the agreement, the Commission has jurisdiction to assess the Transaction. The change in the scope of the Transaction which occurred on 13 December 2017 does not deprive the Commission of its jurisdiction.

6. DESCRIPTION OF LGW'S ACTIVITIES

(22) According to Lufthansa, the proposed acquisition of LGW has different objectives: (i) the discontinuation of the services that LGW provided to Air Berlin and the replacement of Air Berlin by LGW in the framework of the Roof Wetlease between Air Berlin and Lufthansa;20 (ii) the permanent integration of the aircraft and crew deployed under the Roof Wetlease into Lufthansa; and (iii) the takeover of an additional slot package (the LGW slots and the surplus slots).21

(23) Prior to the Transaction, LGW operated as a wetlease provider for Air Berlin, and thus mainly acted as a production platform within the Air Berlin Group.22 The slots used to operate the flights were held by Air Berlin and the tickets for those flights were marketed and sold by Air Berlin. This means that Air Berlin had a position on the markets (routes) for passenger air services, while LGW was active on the market for the wetleasing of aircraft, although on an intra-group basis only.

(24) As a result of the grounding of Air Berlin's fleet on 28 October 2017, Air Berlin lost its position on the markets for passenger air services. LGW no longer operated as an in-house wetlessor for Air Berlin, but continued its activities, this time as wetlessor on the merchant market, replacing Air Berlin as Lufthansa's wetlessor. LGW thus operated Eurowings' flights previously performed by Air Berlin under the Roof Wetlease. For that purpose, Lufthansa requested and was granted by the Commission a derogation from the standstill period under Article 7(3) of the Merger Regulation on 27 October 2017, the day before the grounding of Air Berlin. The derogation was granted subject to conditions to preserve NIKI and LGW, in case the whole or parts of NIKI or LGW would be acquired by any other purchaser than Lufthansa.23

(25) In view of the above, the Commission considers that prior to, and independently of, the Transaction, Air Berlin and LGW had ceased to operate on, respectively, the markets for passenger air transport and for wetleasing of aircraft. Moreover the entering into the wetlease agreement between Lufthansa and LGW has a very limited impact on these two markets, to the extent that it replaces the Roof Wetlease that was already in place between Lufthansa and Air Berlin.

(26) In this context, the integration of the aircraft and crew assigned to the continuity of the Roof Wetlease, via the acquisition of LGW, has a very limited impact on the markets for passenger air transport and wetleasing of aircraft compared to the situation which prevailed pre-Transaction under the Roof Wetlease. Moreover, the Roof Wetlease has been examined and approved under German merger rules by the German Federal Cartel Office.24 The Commission therefore considers that it is not necessary, for the purpose of this Decision, to further assess the acquisition by Lufthansa, via LGW, of aircraft and crew assigned to the Roof Wetlease (or to the wetlease agreements that Lufthansa has entered into for the strict replacement of the Roof Wetlease).

(27) However, the transfer of slots through the acquisition of LGW is unrelated to the Roof Wetlease, which is operated with Eurowings slots only.25 This holds true for both (i) the LGW slots, which are held by Air Berlin and used on routes operated by LGW, and (ii) the surplus slots, which are held by Air Berlin and used on routes operated by Air Berlin (and not LGW) prior to Air Berlin's termination of its operations. Therefore, the structural effects on competition brought about by the Transaction stems from the transfer of slots from Air Berlin to Lufthansa.

7. ANALYTICAL FRAMEWORK

(28) Proper examination of the competitive effects of a transaction under the Merger Regulation rests in particular on a sound understanding of (i) the competitive constraints under which the merged entity will operate, and (ii) the specific causal effects of the transaction on the development of competition in the market.

(29) Along those lines, and taking account of the forward-looking nature of merger control, the Commission will, as an introduction, describe the EU slot system (section 7.1). Next, it will define the relevant markets (section 7.2). The Commission will then determine the circumstances likely to prevail on the relevant markets absent the Transaction (the relevant "situation absent the Transaction", section 7.3).

(30) The Transaction relates to passenger air transport, considering that (i) Lufthansa provides passenger air transport services, and (ii) LGW, to which additional aircraft, crew have been transferred prior to closing, is used as a vehicle for the transfer of slots (see section 6), which are essential to operate air transport services.

7.1. Introduction

(31) The Commission will describe the relevance of slots as an input for air transport services (section 7.1.1) and the EU rules that govern their allocation at EU airports (section 7.1.2).

7.1.1. Slots as an input for air transport services

(32) By virtue of the Slot Regulation, slots, i.e. the permission to land and take-off at a specific date and time at congested airports, are essential for airlines' operations. Indeed, only air carriers holding slots are entitled to get access to the airport infrastructure services delivered by airport managers and, consequently, to operate routes from or to those airports.

(33) The Commission has, in its prior decision practice on mergers involving air carriers, highlighted that the lack of access to slots constitutes a significant barrier to entry or expansion at Europe's busiest airports.26

(34) The Commission has also insisted, in the framework of its airport policy, that "slots are a rare resource" and "access to such resources is of crucial importance for the provision of air transport services and for the maintenance of effective competition."27

(35) In addition, the Slot Regulation recalls that, with the increase of air traffic, there is a continuously growing demand for capacity at congested airports.28 Therefore, the lack of available slots has become a prominent feature of the EU airline industry and is expected to become an even more critical issue for air carriers in the near future.

7.1.2. Rules for the allocation of slots

(36) In the context of imbalance between demand and supply of airport capacity, the Slot Regulation defines the rules for the allocation of slots at EU airports. It aims at ensuring that, where airport capacity is scarce, the latter is used in the fullest and most efficient way and slots are distributed in an equitable, non-discriminatory and transparent way.

(37) Under the Slot Regulation, the general principle regarding slot allocation is that an air carrier having operated its particular slots for at least 80 % during the summer or winter scheduling period is entitled to the same slots in the equivalent scheduling period of the following year (the "grandfather rights").29 Consequently, slots which are not sufficiently used by air carriers are reallocated (the "use it or lose it" rule).

(38) The Slot Regulation also provides for the setting up of "pools" containing newly-created time slots, unused slots and slots which have been given up by a carrier or have otherwise become available. 50% of the slots from the slot pool shall be first offered to new entrants. The other 50% of the slots from the slot pool shall be placed at the disposal of other applicant airlines (incumbent airlines). If applications by new entrants amount to less than 50% of the capacity made available through slots from the pool, this remaining capacity shall also be placed at the other applicants' disposal.30

(39) Under the Slot Regulation, slots cannot be traded. They may however be exchanged or transferred between airlines in certain specified circumstances. If the Transaction is consummated, the transfer of slots from Air Berlin to Lufthansa could, subject to the explicit confirmation from the coordinator under the Slot Regulation,31 take place in the framework of this exception.

7.2. Relevant markets

(40) The Commission will first address the relevance of the markets, defined in previous cases as passenger air transport on city pairs, for the Transaction in the light of the fact that the Transaction concerns the transfer of slots from a bankrupt air carrier (section 7.2.1). Second, the Commission will define the markets relevant for the assessment of the Transaction (section 7.2.2).

7.2.1. Relevance of markets defined as passenger air transport on city pairs

(41) The Commission has, in its prior decision practice related to airlines, defined the relevant market for scheduled passenger air transport services on the basis of the "point of origin/point of destination" ("O&D") city-pair approach.32 Under the O&D approach, every combination of an airport or city of origin to an airport or city of destination is defined as a distinct market. The effects of a transaction on competition are thus assessed for each O&D separately.

(42) Lufthansa submits that it intends to use the slots to be transferred in the context of the Transaction to implement its growth plans and that it will not in any sense take over the flights that Air Berlin used to operate.33 Therefore, Lufthansa considers that, at least as far as the surplus slots are concerned, the Transaction does not give rise to affected markets corresponding to the routes on which Air Berlin happened to use the slots.34

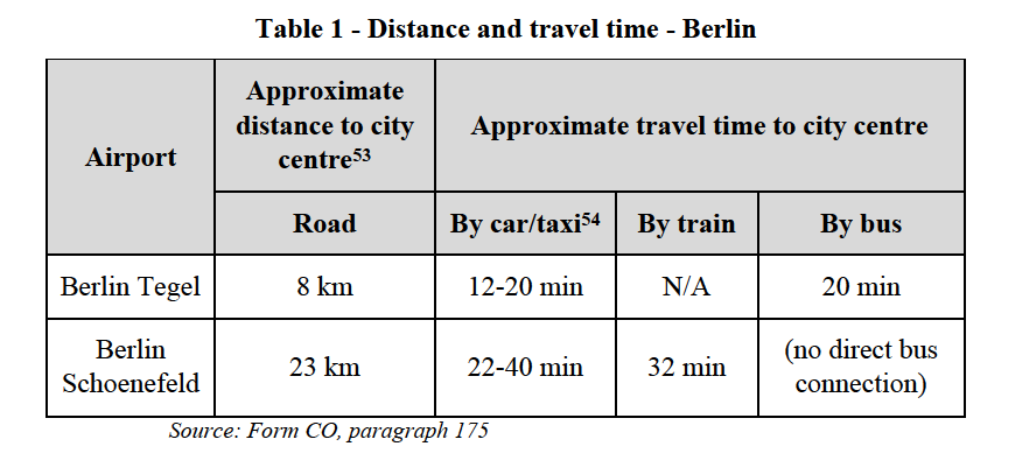

(43) A number of respondents to the market investigation indicate that the traditional O&D approach is not sufficient to fully address the effects of the Transaction.35 In particular, some competitors point to the necessity to address the reinforcement of Lufthansa's position at airports, submitting that "a comprehensive approach shall also include the assessment of the entire market strength of an airline at any respective airport (…);" "[a]n approach which also takes into account local effects at certain airports, separated from a view on certain routes, should be used;" or "[b]esides the O&D approach, it might be necessary to assess also the overall share (or share’s increases) of Lufthansa Group’s operations in each of the airports."36

(44) The Commission considers that the traditional O&D approach, under which each O&D city-pair is assessed separately, would fail to capture the structural effects on competition brought about by the Transaction, in view of (i) the termination of Air Berlin's (including LGW's) operations prior to the Transaction, hence its exit from all O&D markets, and (ii) the fact that LGW is used in particular as a vehicle for the transfer of Air Berlin's slots.

(45) First, Air Berlin ceased its flight operations prior to the Transaction and exited all the routes on which it used the slots forming part of LGW. As a consequence, LGW also exited the routes on which it deployed its fleet on behalf of Air Berlin. Such a situation is independent of the Transaction and it is highly unlikely that Air Berlin or LGW would resume operations.

(46) Considering that Air Berlin and LGW, prior to and independently of the Transaction, stopped their activities as air carriers, it would be inappropriate in the present case to use an analytical framework designed to address the loss of O&D competition following the merger between two air carriers.

(47) In prior airline cases for which the target was expected to discontinue its operations absent the transaction but had not stopped its operations pre-transaction, the Commission assessed both the route-by-route effects of the transaction (as justified by the on-going operations of the target air carrier) and the transaction's impact on the competitive threat posed by other carriers, which is not necessarily linked to specific routes.37 Thus, in those cases, the Commission also performed a detailed analysis of the impact of the transaction on the distribution of slots at each congested airport and, therefore, of the impact of the transaction on all the markets (i.e., aggregating all routes) for passenger air transport from or to the congested airport.38

(48) Second, the Transaction mainly entails the transfer of slots. As explained in section 7.1.1, slots are attached to an airport but are not attached to any specific route. This is particularly clear in this case considering that Air Berlin and LGW do not use those slots anymore on any route. Consequently, the Transaction entails the transfer to Lufthansa of certain inputs (i.e. slots) needed to operate routes from or to certain airports, without limiting Lufthansa to use these inputs on specific routes. In this regard, a respondent to the market investigation notes that the appropriateness of the O&D approach "depends on whether the slots and capacity continue to be allocated in future in the same way as they were under Air Berlin." Another air carrier believes that "the O&D approach is a less appropriate way to assess the effects of the Transaction than an approach by airport." It provides the following example of two different routes served from Berlin Tegel airport, illustrating that, although the barriers to enter or expand on these two routes are the same, an O&D assessment would result in diverging conclusions: "Whereas the route TXL-PMI [Berlin Tegel-Palma de Mallorca] could be considered problematic under the “O&D” approach regarding the competitive situation, the route TXL-VAR [Berlin Tegel-Varna] might appear less problematic. In general, an airport slot can be used for any kind of service and is not bound to a certain route. Nevertheless, an operation on the route TXL-VAR [Berlin Tegel-Varna] would be very difficult due to the slot situation and other dominance effects in TXL [Berlin Tegel]."39

(49) In light of the above, considering that Air Berlin and LGW exited all the routes and that the Transaction primarily relates to slots, that is to say the right to operate at airports, the Commission considers that the Transaction does not result in the take-over by Lufthansa of Air Berlin's or LGW's position on any specific routes. Therefore, the Commission will not carry out an O&D assessment of the effects of the Transaction.

(50) By contrast, the Transaction results in the take-over by Lufthansa of Air Berlin and LGW's positions at certain airports, corresponding to the slots, i.e. the rights to operate flights from or to airports, that have been transferred to LGW before their transfer to Lufthansa.

7.2.2. Markets relevant for the assessment of the transfer of slots

(51) According to the Explanatory Memorandum for the Commission Proposal for a Regulation of the European Parliament and of the Council on common rules for the allocation of slots at European Union airports,40 "the emergence of a strong competitor at a given airport requires it to build up a sustainable slot portfolio to allow it to compete effectively with the dominant carrier (usually the “home” carrier)."

(52) In this context, as regards the transfer of slots, the Commission has previously aggregated all routes originating or terminating in an airport for the purpose of defining the relevant situation absent the Transaction.41

(53) Accordingly, the Commission has assessed the impact of the Transaction in terms of Lufthansa's resulting slot holding in relation to the markets for passenger air transport services from or to the relevant airports (section 7.2.2.1). On these markets, the Parties, as slot holders, are both present on the supply side.

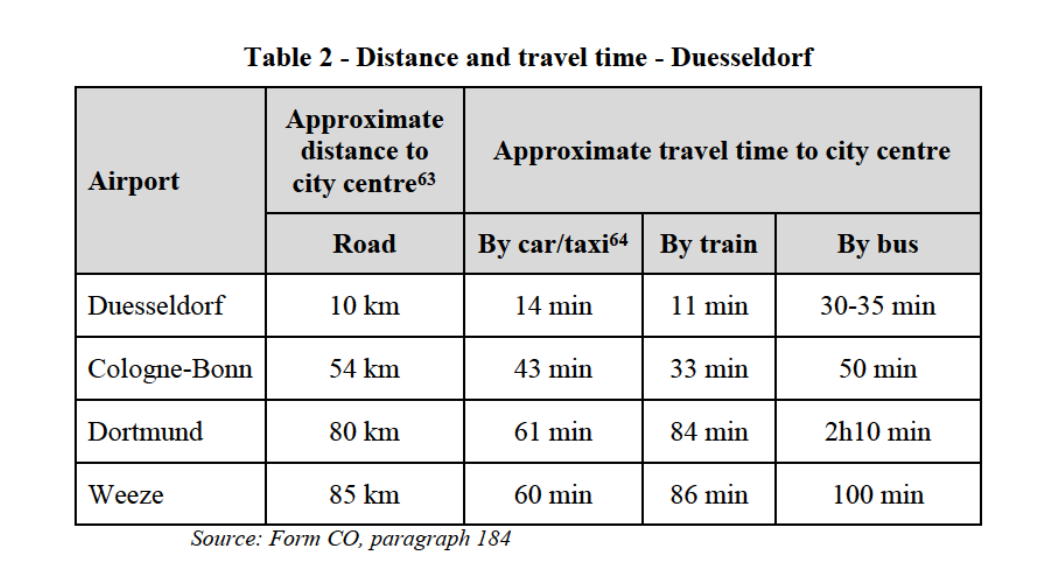

(54) In addition, slots relate to air carriers' ability to operate flights from or to the relevant airports, since air carriers, through slots, get access to airport infrastructure, notably to the available runway and terminal capacity, so that there is a market for airport infrastructure services to airlines. On this market, the Parties are both present on the demand side (section 7.2.2.2).

7.2.2.1. Passenger air transport services

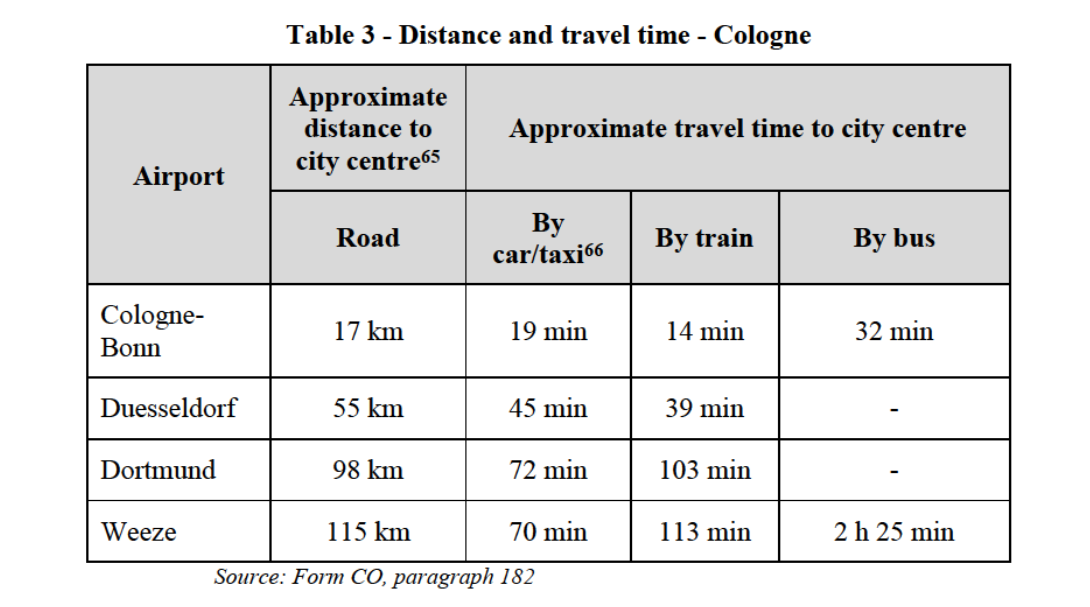

(a) Product market

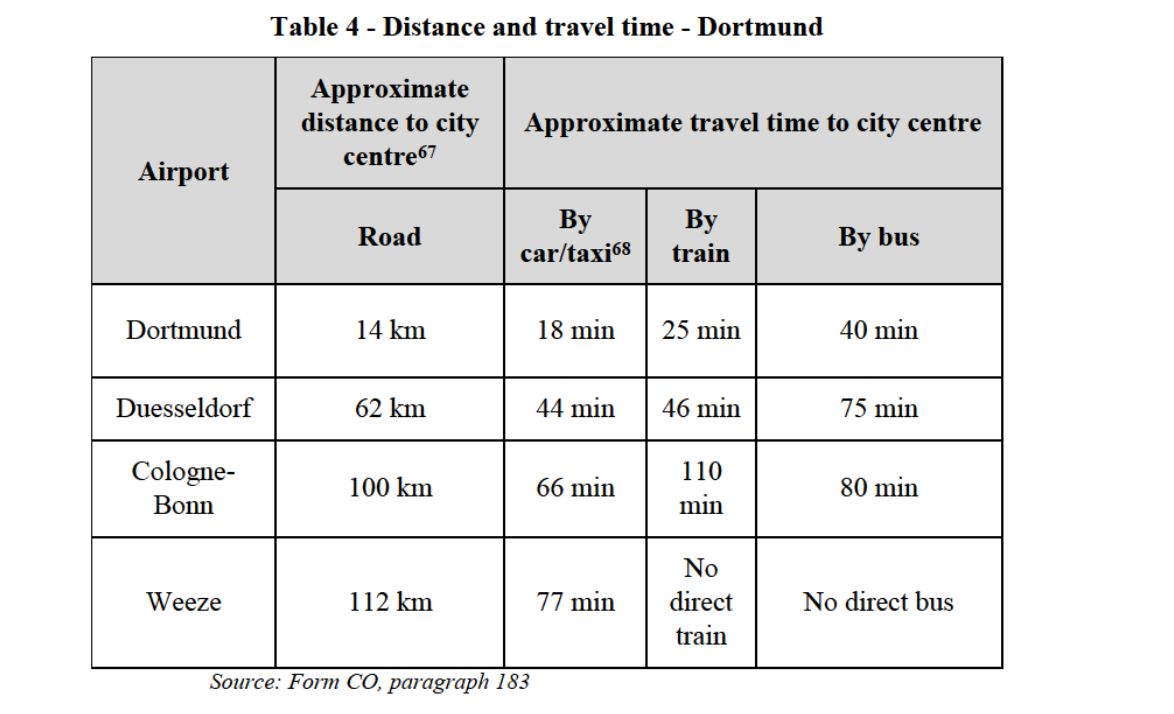

(55) In several prior decisions, the Commission has considered the effects of a transaction on the flight operations of air carriers at an airport, without distinguishing between the specific routes served from or to that airport. Such an approach has notably been adopted to assess the risks of foreclosure entailed by a concentration between an airport manager and an air carrier at Prague airport,42 or the effects of the strengthening of an airline's position at Heathrow airport.43

(56) In those decisions, the Commission has not deemed it necessary to consider the same distinctions as those considered when each O&D market is examined separately (e.g. time sensitive vs. non-time sensitive passengers, direct vs. indirect flights, charter flights vs. scheduled flights, air transport vs. train transport, wholesale vs. retail supply of airline seats, feeder traffic).44

(57) In this case, the Transaction results in a concentration of slots at certain airports in the hand of a single undertaking. As described in section 7.1.1, airline carriers need these slots in order to compete in the various O&D markets originating and arriving at a specific airport. The Transaction's impact on competition, if any, will therefore occur on the various O&D markets originating and arriving at the airport at which slots are acquired. For the purposes of assessing the Transaction, it is, however, not necessary to analyse each of these O&D markets separately.45 As will be explained in section 8.2, the Transaction potentially only has an impact on the ability of air carriers to operate on these markets in view of their access to slots. As mentioned before, these slots are not linked to specific routes and can be used to operate in any relevant O&D market.

(58) For the purpose of this Decision, the Commission therefore considers the markets for the provision of passenger air transport services from or to an airport taken together.

(b) Geographic market

(59) The Commission has, in its prior decision practice related to the definition of O&D markets, considered flights to or from airports with sufficiently overlapping catchment areas to be substitutable with each other (particularly if the airports serve the same main city).46 The evidence used to characterise airport substitutability includes inter alia a comparison of actual distances and travelling times to the indicative benchmark of 100 km/1 hour driving time, the outcome of the market investigation (views of the airports, the competitors, and other market participants), and the parties' practices in terms of monitoring.

(60) The Commission will assess the position of the Parties at each relevant airport to which the LGW and surplus slots relate, although it will not perform a traditional O&D analysis in this case. For the purposes of analysing the Transaction, it is necessary to consider whether some of the relevant airports are substitutable with other airports in view of their overlapping catchment areas.

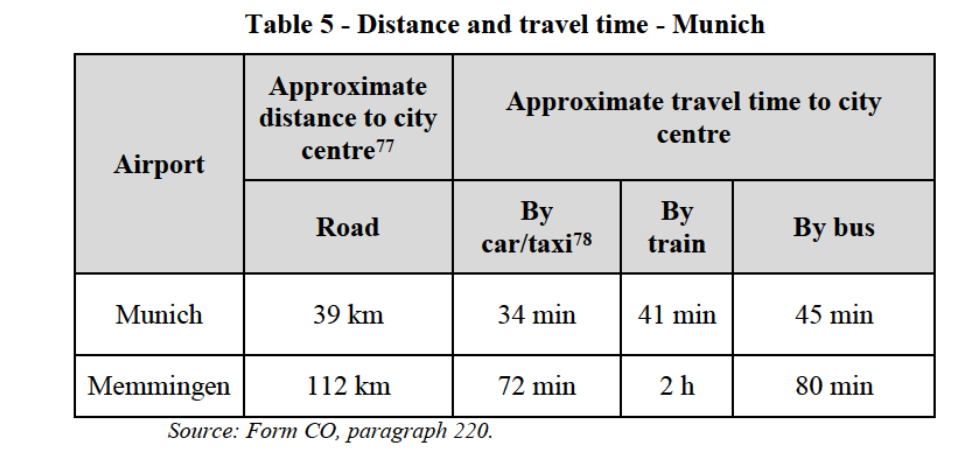

Overview of the relevant airports

(61) The slots to be transferred to LGW for the purpose of its acquisition by Lufthansa relate to 11 airports in Germany, Austria and Switzerland47 and to 8 other EU airports.48 Of these 19 airports, 1449 are coordinated airports.50 The question of substitutability is relevant only for 7 airports, which serve cities or regions also served by at least one other airport.51 These airports are discussed below.

Substitutability of Berlin Tegel and Berlin Schoenefeld airports

(62) Berlin currently has two airports, Berlin Schoenefeld and Berlin Tegel, from which Lufthansa operates and to which the slots to be transferred through the Transaction relate. Berlin Tegel airport is scheduled to close when all Berlin flights move to the Berlin-Brandenburg International Airport, which is, in effect, an extension of Berlin Schoenefeld. However, Berlin-Brandenburg International Airport is still under construction.

(63) The Commission has found, in a prior decision, that Berlin Tegel and Berlin Schoenefeld airports are substitutable from the point of view of passengers.52

(69) Finally, the airport manager of the two Berlin airports indicates that the two airports have different customer bases.60

(70) In any case, for the purpose of this Decision, the question of whether Berlin Tegel and Berlin Schoenefeld airports belong to the same geographic markets for passenger air transport can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either plausible market definition (see section 8.2.4.5).

Substitutability of Duesseldorf, Cologne-Bonn, Dortmund, and Weeze airports

(71) According to Lufthansa, the Rhine-Ruhr catchment area comprises at least four airports: Duesseldorf, Cologne-Bonn, Dortmund and Weeze.61 The slots to be transferred through the Transaction relate to Duesseldorf and Cologne-Bonn airports, while Lufthansa operates from Duesseldorf, Cologne-Bonn and Dortmund airports.

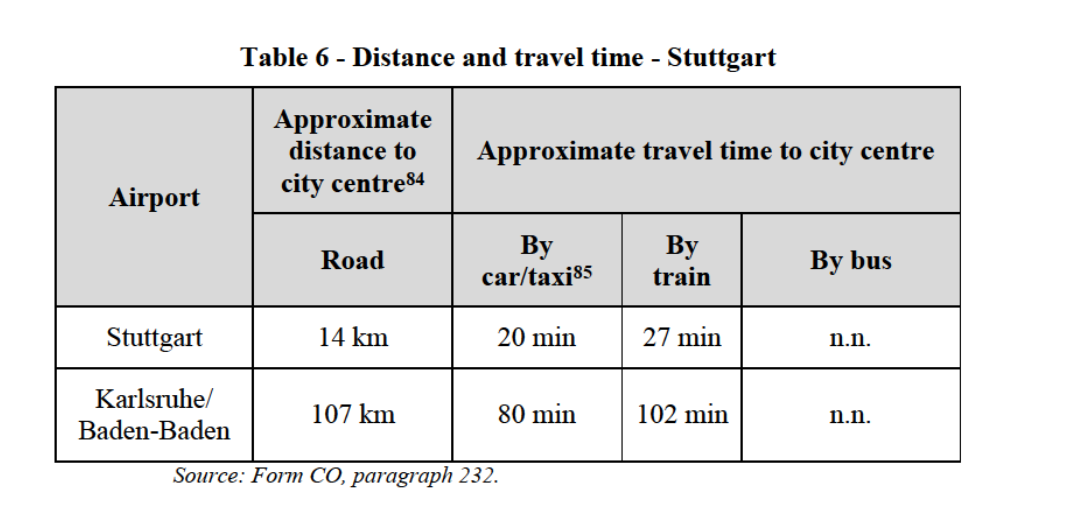

(72) In prior decisions, the Commission's assessment on whether Duesseldorf and Cologne-Bonn airports are substitutable depended on the type of passengers.62

(73) Taking Duesseldorf as the centre of the catchment area, the distances and travel times are as follows:

(80) The responses of airport managers are also inconclusive.71

(81) The results of the market investigation addressed to tour operators are more clear-cut. A majority of those having expressed an opinion do not consider any of the four airports as substitutable with another one for the relevant routes.72

(82) Similarly to tour operators, a minority of travel agents consider the different airports as substitutable with each other for the relevant routes and would propose, for a relevant route, flights from another airport to customers wanting to fly from either Duesseldorf, Cologne-Bonn, Dortmund or Weeze airport.73

(83) In any case, considering that, for the purpose of this Decision, the geographic scope of the market for airport infrastructure services to which slots give access is found to be limited to Duesseldorf airport (see section 7.2.2.2), the Commission's assessment of the impact of the Transaction on competition in the markets for passenger air transport services will be limited to Duesseldorf airport.

Substitutability of Munich and Memmingen airports

(84) According to Lufthansa, Munich airport and Memmingen airport are substitutable for the vast majority of passengers in the greater Munich region.74 Both Lufthansa's operations and the slots to be transferred through the Transaction relate to Munich airport.

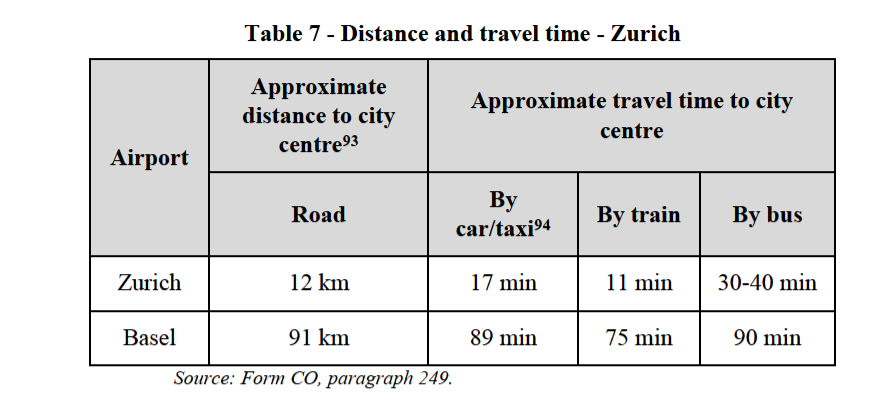

(85) In two prior decisions, the Commission reached different conclusions depending on the routes, air carriers and customers. While Munich and Memmingen airports were found to belong to the same market for routes between Dublin and Munich,75 Memmingen airport was deemed unlikely to be substitutable to Munich airport, except for a very limited number of particularly non-time sensitive passengers.76

(86) Taking Munich as the centre of the catchment area, the distances and travel times are as follows:

travel agent having responded to the market investigation considers that the two airports are substitutable.89 In this context, no travel agent would propose flights from or to Karlsruhe/Baden-Baden airport to passengers wanting to fly from or to Stuttgart airport (and vice versa).90

(97) Finally, the manager of Stuttgart airport states that passengers and tour operators barely consider Stuttgart airport and Karlsruhe/Baden-Baden airports as substitutable, and their catchment areas overlap only to a small extent, due to geographic and infrastructure reasons.91

(98) In any case, considering that, for the purpose of this Decision, the geographic scope of the market for airport infrastructure services to which slots give access is found to be limited to Stuttgart airport (see section 7.2.2.2), the Commission's assessment of the impact of the Transaction on competition in the markets for passenger air transport services will be limited to Stuttgart airport.

Substitutability of Zurich and Basel airports

(99) According to Lufthansa, the Northern Switzerland catchment area comprises at least Zurich airport and Basel airport. Lufthansa operates from both Zurich and Basel airports, while the slots to be transferred through the Transaction relate to Zurich airport only.

(100) In prior decisions, the Commission assessed routes from or to Zurich and Basel airports separately.92

(101) Taking Zurich as the centre of the catchment area the distances and travel times are as follows:

Prat airport brought about by the Transaction is de minimis, as explained in section 8.2.4.7.

(107) Therefore, the question of whether Barcelona-El Prat, Reus and Girona airports belong to the same geographic markets for passenger air transport can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either plausible market definition (see section 8.2.4.7).

Substitutability of Venice and Treviso airports

(108) For Venice airport, (i) Lufthansa has no operations at Treviso airport, and (ii) the increment in Lufthansa's operations at Venice airport brought about by the Transaction is de minimis, as explained in section 8.2.4.7.

(109) Therefore, the question of whether Venice and Treviso airports belong to the same geographic markets for passenger air transport can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either plausible market definition (see section 8.2.4.7).

Conclusion

(110) For the purpose of this Decision, the question of whether the geographic scope of the markets for passenger air transport services from or to a relevant airport is limited to an airport or encompasses airports in the same catchment area can be left open for Berlin, Barcelona and Venice airports, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either plausible market definition (see section 8.2.4).

(111) For the purpose of this Decision, for Duesseldorf, Munich, Stuttgart and Zurich airports, considering that the geographic scope of the market for airport infrastructure services to which slots give access is limited to the airport, the Commission will analyse the effects of the Transaction on the markets for passenger air transport services from or to each of these airports.

7.2.2.2. Airport infrastructure services

(112) For the purpose of providing passenger air transport services at congested airports, airlines have to source infrastructure services at those airports. As indicated in section 7.1, at congested airports, infrastructure capacity is managed through the allocation of slots, which enable air carriers to fly to and from the airports. Slots are therefore defined, from the point of view of airports, as "a planning tool for rationing capacity at airports where demand for air travel exceeds the available runway and terminal capacity."99 From the point of view of airlines, the granting of a slot at an airport means that the airline may use the entire range of infrastructure necessary for the operation of a flight at a given time (runway, taxiway, stands and, for passenger flights, terminal infrastructure). This in turn enables the air carriers to provide passenger air transport services to and from that airport.

(113) As a consequence, through the transfer of Air Berlin's slots via LGW, Lufthansa obtains a right to access to a higher share of airport infrastructure capacity. The Transaction therefore has an impact on (the demand-side of) the markets for airport infrastructure services at the relevant airports and further on the markets for passenger air transport to and from those airports.

(a) Product market

(114) The Commission has, in its prior decision practice, delineated a product market for the provision of airport infrastructure services to airlines, which includes the development, maintenance, use and provision of the runway facilities, taxiways and other airport infrastructure.100 The Commission has considered sub-dividing the market for airport infrastructure services on the basis of airline customers (i.e. charter operators, scheduled full service carriers and scheduled low cost carriers) and on the basis of the type of flights (i.e. short haul and long haul).101

(115) For the reasons set out above in section 7.1.1, the Commission considers that slots are an essential input to enable air carriers to get access to airport infrastructure. As such, via slot holdings, air carriers are present on the demand side of the market for airport infrastructure services.

(116) Considering that the effects of the Transaction relate only to the reinforcement of Lufthansa's portfolio of slots and that the latter give access to all infrastructure services necessary to operate at the airport, the Commission considers that, for the purpose of this Decision, it is not necessary to further distinguish within the market for airport infrastructure services.

(b) Geographic market

(117) The Commission has, in its prior decision practice, defined the geographic scope of the market for airport infrastructure services as the catchment area of individual airports.

(118) The Commission has also considered additional criteria relevant for assessing airport substitutability in relation to the market for airport infrastructure services, while acknowledging that the airlines' choice of airports ultimately depends on passengers' demand. In addition to the catchment area of a particular airport, the Commission has notably analysed the costs of operating from a particular airport, capacity constraints for slots and facilities, passenger volumes or the positioning of the airport (e.g. a niche airport serving high yield time-sensitive passengers or an airport serving mainly leisure, less time-sensitive passengers).102

Overview of the relevant airports

(119) As indicated in section 7.2.2.1, the slots to be transferred through the Transaction relate to 19 airports, out of which 7 raise the issue of substitutability with other airports.

Substitutability of Berlin Tegel and Berlin Schoenefeld airports

(120) The question of the catchment area of Berlin Tegel and Berlin Schoenefeld airports is addressed in section 7.2.2.1.

(121) In terms of congestion, the two airports have limited slot availability at peak times.103 In addition, the two airports are large airports with more than one terminal, used in 2016 by over 21 million passengers for Berlin Tegel airport and approximately 12 million passengers for Berlin Schoenefeld airport.

(122) Nevertheless, Berlin Tegel airport appears more congested than Berlin Schoenefeld airport during peak periods and for longer periods throughout the day.104 The single airport manager of the two Berlin airports notes that the two airports have different particularities, Berlin Schoenefeld being a more low cost airport than Berlin Tegel, and Berlin Tegel being more used for business traffic and long-haul destinations.105

(123) In any case, for the purpose of this Decision, the question of whether Berlin Tegel and Berlin Schoenefeld airports belong to the same geographic market for airport infrastructure services can be left open, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either plausible market definition (see section 8.2.4.5).

Substitutability of Duesseldorf, Cologne-Bonn, Dortmund, and Weeze airports

(124) The question of the catchment area of Duesseldorf, Cologne-Bonn, Dortmund, and Weeze airports is addressed in section 7.2.2.1.

(125) In terms of congestion, Duesseldorf airport presents very different features from the other three airports. It is coordinated (Level 3)106 during summer and winter, while Cologne-Bonn is schedules facilitated107 (Level 2).108 Dortmund and Weeze are neither coordinated nor schedules facilitated. As acknowledged by Lufthansa, potential entrants face different barriers to entry at Duesseldorf airport compared to the three other airports of the Rhine-Ruhr area.109

(126) In terms of size, Duesseldorf airport is, with 24 million passengers in 2016,110 larger than Cologne-Bonn (12 million passengers),111 Dortmund and Weeze (2 million passengers each).112 Duesseldorf airport has three terminals, Cologne-Bonn two, Dortmund and Weeze one.

(127) The airports have different positionings and marketing strategies vis-à-vis passenger traffic, which are reflected by the ranking of the airlines present at the airports and the destinations they serve. In 2016, the main customers of Duesseldorf airport services were Air Berlin, the Lufthansa Group (Eurowings/Germanwings, Lufthansa and SunExpress) as well as Condor. The 72 airlines operating at Duesseldorf airport served 52 countries and 204 destinations, showing that air carriers use Duesseldorf airport for connections and long-haul traffic, as well as for the supply of wholesale seats to tour operators.113 By contrast, Cologne-Bonn airport is mainly oriented towards low-cost carriers, with the Lufthansa Group (Eurowings) and Ryanair being the first two air carriers at the airport. Eurowings started operating long-haul routes only in 2016.114 As to Dortmund and Weeze, they almost exclusively depend on low-cost carriers, in particular Wizz Air for Dortmund115 and Ryanair for Weeze.116

(128) The above elements demonstrate that the demand from airlines is consistently higher at Duesseldorf airport than in the other airports and that the services sourced from Duesseldorf airport are more comprehensive than those provided by other airports. The market investigation has provided indications that demand of airport services by airlines is relatively price-inelastic.117 This is particularly true at capacity constrained hubs like Dusseldorf airport, for which air carriers would not easily switch their operations to other airports due to the need to protect slots and to recoup their investments.118 As a consequence, most air carriers present at Duesseldorf airport would unlikely switch to other airports if Duesseldorf airport were to increase its airport charges by 5-10% on a permanent basis.

(129) Lufthansa itself does not seem to consider Cologne-Bonn airport as an adequate substitute for Duesseldorf airport, since […].119

(130) Considering that (i) only Duesseldorf airport is a coordinated airport, and (ii) Duesseldorf airport has a different positioning and market strategy (serving in particular full service carriers offering intercontinental flights), the Commission concludes that, for the purpose of this Decision, the geographic scope of the market for the provision of airport infrastructure services to airlines is limited to Duesseldorf airport.

Substitutability of Munich and Memmingen airports

(131) The question of the catchment area of Munich and Memmingen airports is addressed in section 7.2.2.1.

(132) Munich airport is a coordinated (Level 3) airport during summer and winter, while Memmingen airport is neither coordinated nor schedules facilitated. According to Lufthansa, slot utilisation at Munich airport is 72%, whereas Memmingen airport is not subject to any slot constraints.120 The number of passengers at Munich airport reached 42 million in 2016,121 compared to 1 million for Memmingen airport in 2016.122

(133) Munich airport is a European hub, serving 100 airlines, 73 countries and 257 destinations and accounting for the highest share of business travellers in Germany in 2016,123 while Memmingen airport is a regional airport targeting low-cost or destination air carriers (Wizz Air, Ryanair, Corendon or Fly Egypt).

(134) Considering that (i) only Munich airport is a coordinated airport, and (ii) Munich airport has a different positioning and market strategy (serving in particular full service carriers offering intercontinental flights), the Commission concludes that, for the purpose of this Decision, the geographic scope of the market for the provision of airport infrastructure services to airlines is limited to Munich airport.

Substitutability of Stuttgart and Karlsruhe/Baden-Baden airports

(135) The question of the catchment area of Stuttgart and Karlsruhe/Baden-Baden airports is addressed in section 7.2.2.1.

(136) Stuttgart airport is a coordinated (Level 3) airport during summer and winter, while Karlsruhe/Baden-Baden airport is neither coordinated nor schedules facilitated. Lufthansa notes that there are no slot constraints at Karlsruhe/Baden-Baden airport and that all slot requests were accommodated in 2017.124 The number of passengers at Stuttgart airport reached 11 million in 2016,125 compared to 1 million for Karlsruhe/Baden-Baden airport in 2016.126

(137) Stuttgart airport serves 55 airlines and 100 destinations,127 while Karlsruhe/Baden-Baden markets itself as a "regional airport of short distances", targeting leisure or low cost air carriers.128

(138) Considering that (i) only Stuttgart airport is a coordinated airport, and (ii) Stuttgart airport has a different positioning and market strategy (serving in particular full service carriers), the Commission concludes that, for the purpose of this Decision, the geographic scope of the market for the provision of airport infrastructure services to airlines is limited to Stuttgart airport.

Substitutability of Zurich and Basel airports

(139) The question of the catchment area of Zurich and Basel airports is addressed in section 7.2.2.1.

(140) Zurich airport is a coordinated (Level 3) airport during summer and winter, while Basel airport is neither coordinated nor schedules facilitated. As indicated by Lufthansa, there are no slot constraints at Basel airport, while there are at Zurich airport.129 The number of passengers at Zunich airport reached 28 million in 2016,130 compared to 7 million for Basel airport in 2016.131

(141) Zurich airport serves 68 airlines to 178 airports, including 53 intercontinental destinations representing 23% of the total number of passengers,132 while 25 airlines operate at Basel airport to 70-100 short-haul destinations.133

(142) Considering that (i) only Zurich airport is a coordinated airport, and (ii) Zurich airport has a different positioning and market strategy (in particular, it has a more developed intercontinental network), the Commission concludes that, for the purpose of this Decision, the geographic scope of the market for the provision of airport infrastructure services to airlines is limited to Zurich airport.

Substitutability of Barcelona-El Prat, Reus and Girona airports

(143) As mentioned in section 7.2.2.1, the question of airport substitutability does not need to be assessed in detail for Barcelona-El Prat airport, as it would not change materially the assessment of the effects of the Transaction on Lufthansa's slot holding at the airports (see section 8.2.4.7).

Substitutability of Venice and Treviso airports

(144) As mentioned in section 7.2.2.1, the question of airport substitutability does not need to be assessed in detail for Venice airport, as it would not change materially the assessment of the effects of the Transaction on Lufthansa's slot holding at the airports (see section 8.2.4.7).

Conclusion

(145) For the purpose of this Decision, the question of whether the geographic scope of the market for airport infrastructure services is limited to the airport or encompasses airports in the same catchment area can be left open for Berlin Tegel, Barcelona-El Prat and Venice airports, as the Transaction would not raise serious doubts as to its compatibility with the internal market under either plausible market definition (see section 8.2.4).

(146) For the purpose of this Decision, for Duesseldorf, Munich, Stuttgart and Zurich airports, the Commission considers that, in view of the evidence available to it, the market for airport infrastructure services is limited to the airport.

7.2.2.3. Conclusion

(147) In light of the above, for the purpose of this Decision, the Commission will leave the question of the geographic market definitions for Berlin Tegel, Barcelona-El Prat and Venice airports open.

(148) Considering that Lufthansa's slots and the slots to be transferred through the Transaction overlap at Berlin Tegel airport only, the Commission's competitive assessment will be conducted under the assumption that Berlin Tegel airport is a market distinct from Berlin Schoenefeld airport.

(149) Considering that Lufthansa's slots and the slots to be transferred through the Transaction overlap at Barcelona-El Prat airport only, the Commission's competitive assessment will be conducted under the assumption that Barcelona-El Prat airport is a market distinct from Reus and Girona airports.

(150) Considering that Lufthansa's slots and the slots to be transferred through the Transaction overlap at Venice airport only, the Commission's competitive assessment will be conducted under the assumption that Venice airport is a market distinct from Treviso airport.

(151) In addition, in light of the above, for the purpose of this Decision, the Commission will assess whether the Transaction has anticompetitive effects on the markets for passenger air transport from or to Duesseldorf, Munich, Stuttgart and Zurich airports, under the geographic market definition corresponding to a single airport.

(152) In order to assess the effects of the Transaction on the markets for passenger air transport from or to airports, the Commission will take account of the reinforcement of Lufthansa's slot holding at those airports, hence of the reinforcement of its position on the demand-side of the market for airport infrastructure services.

7.3. Relevant situation absent the Transaction

(153) Pursuant to paragraph 9 of the Horizontal Merger Guidelines,134 "[i]n assessing the competitive effects of a merger, the Commission compares the competitive conditions that would result from the notified merger with the conditions that would have prevailed without the merger. In most cases the competitive conditions existing at the time of the merger constitute the relevant comparison for evaluating the effects of a merger. However, in some circumstances, the Commission may take into account future changes to the market that can reasonably be predicted."

(154) Lufthansa underlines that LGW's operations were heavily dependent on Air Berlin's hub operations (in particular long-haul traffic), which Air Berlin has already discontinued irrespective of the Transaction.135 Therefore, LGW's operations prior to Air Berlin's insolvency proceedings were unsustainable and cannot be viewed as the relevant situation absent the Transaction.136

(155) The Commission acknowledges that Air Berlin's on-going insolvency proceedings will most likely lead Air Berlin to be eventually wound up. In the light of the fact that Air Berlin has already exited the passenger air transport markets at the relevant airports (see section 6), the Commission considers that the most likely scenario absent the Transaction is that Air Berlin no longer operates from these airports and that the slots that it currently holds (including the LGW slots and the surplus slots) would be made available to third parties.

(156) More specifically, absent the Transaction, Air Berlin's slots to be transferred to Lufthansa via LGW (the LGW slots and the surplus slots) would either be made available to other third parties than Lufthansa through the sale of all or parts of an air carrier during the insolvency proceedings, or, in the absence of acquirers, fall back to the slot pools and be subsequently reallocated by the relevant slot coordinators (see section 7.1.2).

(157) Based on the information received by the Commission during its market investigation about the credible bids submitted for the air operations of LGW or Air Berlin (excluding NIKI), the Commission considers that, for the purpose of this Decision, the LGW slots and the surplus slots would likely fall back to the slot pools in the situation absent the Transaction.137

(158) These scenarios impact the situation absent the Transaction in two respects. First, the number of slots that Lufthansa would obtain is impacted, as Lufthansa would likely obtain slots in the second scenario through the reallocation process of slots returned to the pool, but not in the first scenario. This, in turn, has an impact on the difference between the number of slots obtained through the Transaction and the number of slots that Lufthansa would have obtained in the situation absent the Transaction (i.e. the "net increment" brought about by the Transaction, see section 8.2.3.1).

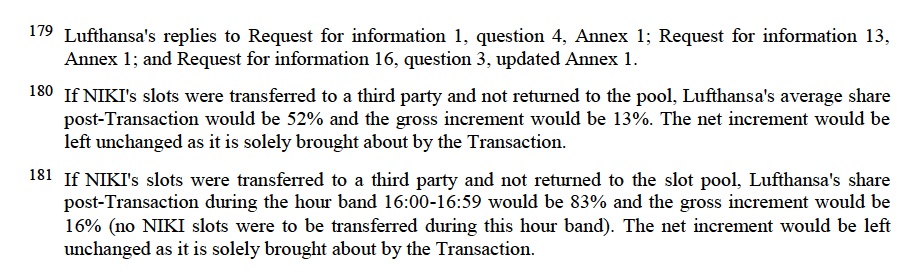

(159) Second, the question of the distribution of the LGW slots and of the surplus slots absent the Transaction has an impact on the slot holding of Lufthansa's competitors at the relevant airports (as they would also obtain slots through a possible reallocation process), hence on the competitive constraint they would be able to exert on Lufthansa absent the Transaction.

8. COMPETITIVE ASSESSMENT

(160) According to Lufthansa's internal documents, one of the rationales for entering into a purchase agreement with Air Berlin was […]. Competitors, especially low cost carriers, could have taken such opportunity to grow and could have expanded their market position in the DACH region (Germany, Austria and Switzerland). This rationale has supported the decision by Lufthansa's Board to initiate the purchase of Air Berlin's assets138 and is illustrated by the following table:139

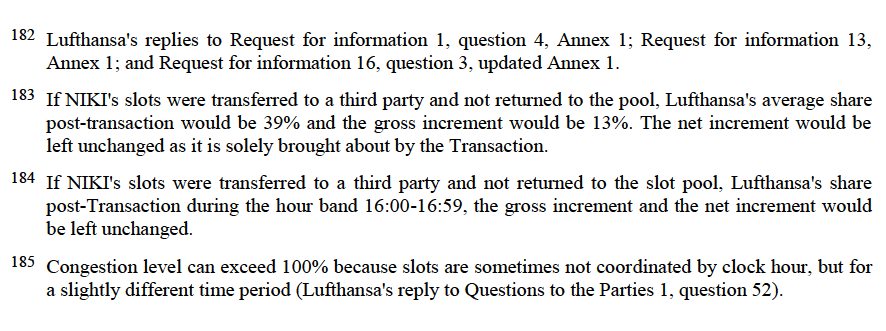

[…]

Source: Form CO, Section 5.4 Documents, […].

(161) In particular, Lufthansa intends to use LGW as […].140

(162) In this context, the Commission will assess whether the Transaction is likely to lead to the creation or strengthening of a dominant position in slot holding having anti-competitive effects on passenger air transport at the airports where, as a result of the Transaction, Lufthansa will obtain additional slots.

8.1. Legal framework

(163) According to paragraph 36 of the Horizontal Merger Guidelines,141 "some proposed mergers would, if allowed to proceed, significantly impede effective competition by leaving the merged firm in a position where it would have the ability and incentive to make the expansion of smaller firms and potential competitors more difficult or otherwise restrict the ability of rival firms to compete. In such a case, competitors may not, either individually or in the aggregate, be in a position to constrain the merged entity to such a degree that it would not increase prices or take other actions detrimental to competition. For instance, the merged entity may have such a degree of control, or influence over, the supply of inputs or distribution possibilities that expansion or entry by rival firms may be more costly."

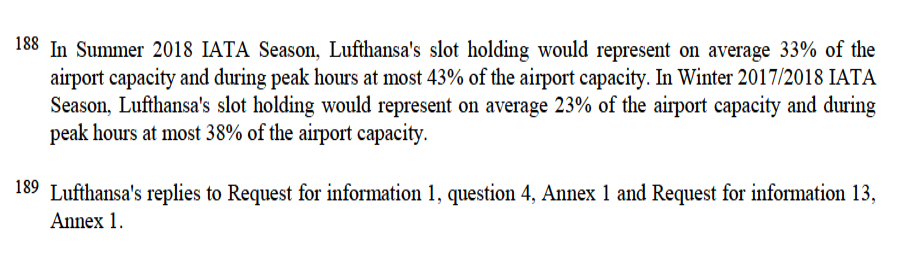

(164) Accordingly, the Commission will first assess whether the Transaction, by reinforcing Lufthansa's slot holding at a number of airports and granting it broader access to their infrastructure, gives Lufthansa the ability and incentive to prevent other air carriers from getting access to airports' infrastructure and therefore to the markets for the provision of passenger air transport services from those airports, preventing or reducing competition on those markets (sections 8.2 and 8.3). The Commission will then analyse the overall effects of Lufthansa's dominant slot holding position, if any, on the ability of Lufthansa's rivals to compete at the relevant airports (section 8.4).

8.2. Ability of Lufthansa to foreclose access to the markets for the provision of passenger air transport services

8.2.1. Link between a dominant slot holding position and the ability to foreclose access

(165) To be able to provide passenger air transport, an air carrier needs access to airport infrastructure. At congested airports, an air carrier must thus hold slots to operate routes from or to those airports.

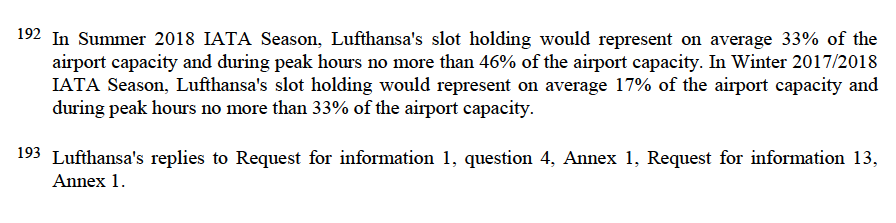

(166) Lack of access to slots is therefore a barrier to an air carrier's ability to compete for passengers between an airport and the destinations served from the airport. Lufthansa itself considers that slot constraints are relevant barriers to entry in the airline industry.142 An airline's slot holding at an airport provides a measure of its ability to compete on the passenger air transport market to or from that airport.

(167) In the present case, the market investigation unambiguously confirmed that there are advantages in the holding of a large portfolio of slots at an airport.143 An airport manager notably underlined that "[t]he more capacity that an airline has at an airport gives it more market power to compete with other airlines", while another noted: "For airlines a high market shares gives following advantages: High market presence and market penetration; Efficient operations at the airports; Operational flexibility through swapping slots within their own operation; Higher negotiating power with the airports and other service providers."144 Air carriers and tour operators also point out the economies of scale, greater flexibility to react to changes in demand as well as the maximisation of passenger load factors granted by a large slot portfolio, e.g.: "[w]ith a large slot portfolio an airline can offer a hub and spoke network connecting SH and LH flights; or a broad p2p route network with an efficient cost structure and optimised to changing customer demand"145 or "may be the airline can gain better prices for handling from the airport authorities and it is easier/cheaper for their marketing activities as the airline can concentrate on a certain (limited) area."146

(168) In addition, the market investigation demonstrated the link between the holding of a large portfolio of slots at an airport and the ability to influence access of competitors to the passenger air transport markets at the airport. An air carrier referred to the ability of large slot holders to operate the highest number of, and most demanded flights at congested airports: "Slots are used to allocate the right to operate a flight at a certain time of a day to an airline. Assuming that the number of available slots at an airport is limited, the airline holding the largest slot portfolio at that airport will have the chance to operate the most flights at that airport. Furthermore, this airline will have the highest flexibility to build an ideal schedule. The airline could offer flight times that matches perfectly the demand of the market,"147 while another mentioned more directly the possibility to block entry or expansion: "this massive slot portfolio will prevent other competitors from entering new routes or grow existing offers."148

(169) Air carriers holding a large slot portfolio may adopt practices aimed at preventing entry or expansion by other carriers at airports, such as predatory pricing, "slot hoarding", "slot babysitting",149 or use of their "slot shuffling power"150 to engage into exclusionary conduct.

(170) A number of airport managers confirmed the link between the breadth of a slot portfolio and the ability to prevent access of other airlines to airport infrastructure services, in particular for competitors wishing to base an aircraft and therefore, requiring the slots necessary to build sustainable rotations. As examples, two airport managers stated the following: "The bigger the slot portfolio, the bigger is the flexibility, i.e. in getting the best slot: (i) For high yield destination; (ii) To secure connectivity at their hub; (iii) To be able to get the best possible Slot at Destination by the possibility to adjust the departure time from their base; (iv) To keep your competitors out" and "Large slot portfolios and therefore high market shares at the airport leads to more market power and makes it easier to keep out competitors."151

(171) An air carrier indicated that a large portfolio of slots reinforces the bargaining power of airlines vis-à-vis airports, which would be less open to new entrants: "Controlling a large slot portfolio and the operations associated therewith also enables airlines to exercise significant pressure on the respective airport. LH Group has for instance used its market share at FRA to criticize FRA’s openness to low cost carrier and has criticized FRA for trying to become more independent of LH Group. In addition it has announced that it will grow at other hubs. This can be understood as LH Group’s message to airports to minimize their incentives to new airlines as they would otherwise need to fear upsetting their main customer. Such behavior clearly limits the commercial freedom of the airports, potential new airline entrants and thus ultimately the choice of customers – individual passengers and tour operators alike."152

(172) Another air carrier notes that "a dominant airline has numerous possibilities to use its influence at an airport in order to foreclose the airport for competitors", notably using its negotiating power "this influence to develop the airport’s infrastructure even more in its own favour."153

(173) An air carrier also elaborates on Lufthansa's practice of cross-subsidisation of routes: "LH already cross-subsidizes routes that are subject to competition. (…) The low prices on routes subject to competition can be offset by high revenues on routes subject to a LH-monopoly, especially regarding the German domestic market. This unfair advantage over smaller competitors leads to a high risk of squeeze out on the routes concerned, thus leading to a further weakening of fair competition."154

(174) Furthermore, under the current regulatory framework, the current system of slot allocation does not have a sufficiently strong deterrent effect against the anticompetitive use of slots.155 As noted by an air carrier, the use-it-or-lose-it rule156 is easier to comply with by large slot portfolio holders: "[A]irlines that hold a large slot portfolio can better ensure that all slots are at least utilized to 80% by shifting departures and origins to slots running a risk to be underutilized. This practice is easier if an airline uses the same airport for many destinations and with a larger slot portfolio. If an airline only controls one weekly slot at an airport and wants to offer a weekly service to that airport it will fully utilize that slot. However, if an airline controls five slots it only requires four services to ensure the 80% utilization rate required to trigger the Slot Regulation's grandfathering rights. Airlines controlling a large slot portfolio can thus reserve a 20% contingency pool that allows reacting quickly to increased demand or changes in the demand from one destination to another."157

(175) Finally, Lufthansa's internal documents indicate that […].

(176) [Lufthansa's slot holding strategy].158 […].159 […].

(177) [Example at Frankfurt airport].160

(178) [Example at Munich airport].161[…].162

(179) [Example at Zurich airport].163

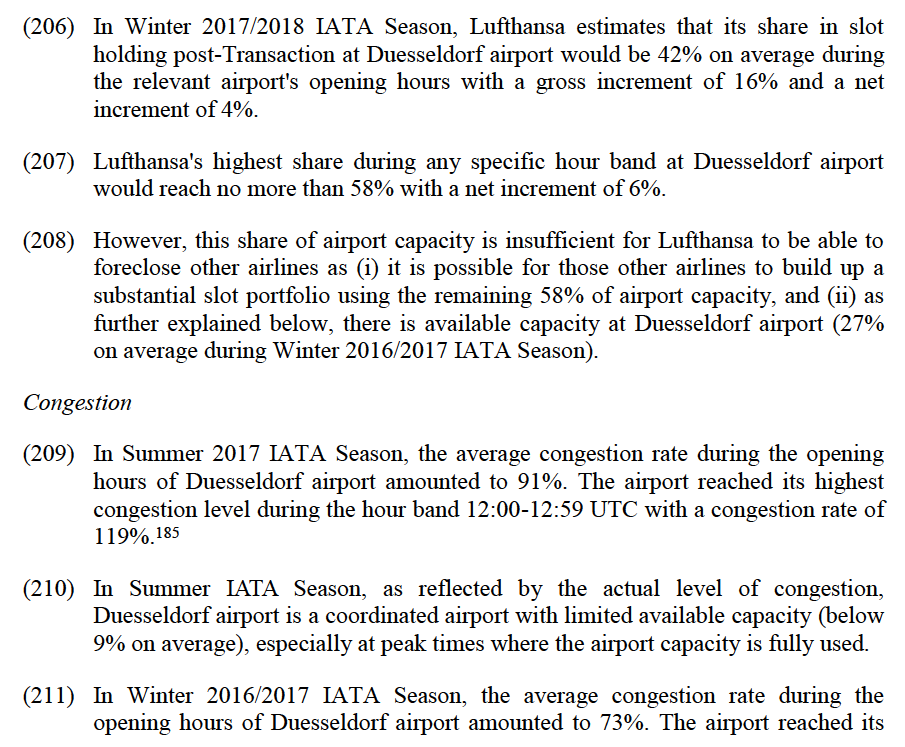

(180) [Lufthansa's commercial strategy].164

(181) [Example at Duesseldorf airport].165 […].166

8.2.2. Conditions for the ability for foreclose access

(182) For Lufthansa to be able to foreclose its competitors post-Transaction, the following conditions must be fulfilled: (i) the slots that Lufthansa would hold post-Transaction represents a significant share of the airport capacity, in particular at peak times; (ii) the Transaction has a material impact on Lufthansa's slot holding at the airport, in particular at peak times; and (iii) Lufthansa's slot holding could negatively affect the overall availability of input for the passenger air transport markets from or to the relevant airport.

(183) This third criterion requires that (i) the airport at which Lufthansa would hold a large portfolio of slots does not have sufficient available capacity (i.e. its level of congestion is high); and (ii) the airports considered as substitutable by air carriers (if any, see section 7.2.2) do not have sufficient available capacity either.

(184) The Commission also considered whether rival firms would be likely to deploy effective and timely counter-strategies in case of foreclosure. In this case, the Commission notes that there are limited effective and timely counter-strategies that Lufthansa's competitors would be likely to deploy in case of foreclosure strategy by Lufthansa. There is no possibility for an air carrier to be less reliant on access to airport infrastructure and very limited possibility to sponsor the expansion of airport capacity or the opening of new airports.167

(185) In light of the above, the Commission will assess the ability of Lufthansa post-Transaction to foreclose access to the markets for the provision of passenger air transport at the relevant airports by taking account of the following three factors together: (i) the share of slots held by Lufthansa post-Transaction at the airport or at substitutable airports being high, in particular at peak times;168 (ii) the net increment in Lufthansa's slot holding brought about by the Transaction at the airport or at the substitutable airports being material, in particular at peak times; and (iii) the level of congestion at the airport or at the substitutable airports being high. Considering that Lufthansa's slot holdings and the levels of congestion of the relevant airports vary between the Summer and Winter IATA Seasons, the Commission will carry out separate assessments for each IATA Season.

(186) Before an airport-by-airport assessment of Lufthansa's ability to foreclose access to the markets for the provision of passenger air transport (section 8.2.4), the Commission will detail the methodologies for determining airport congestion, Lufthansa's slot holding post-Transaction and the increment brought about by the Transaction.

8.2.3. Methodologies

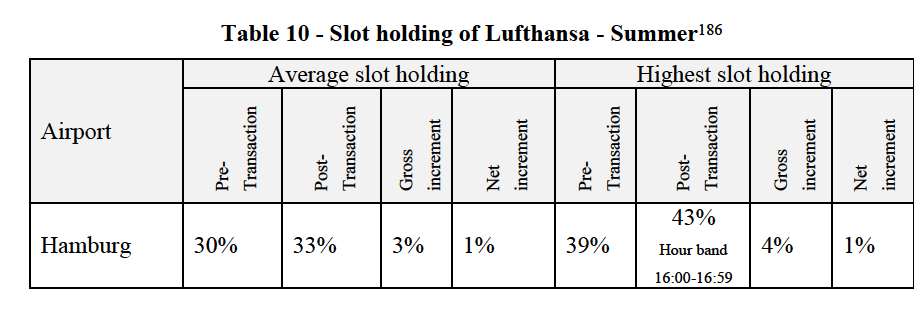

8.2.3.1. Slot holding and increment brought about by the Transaction

(187) A slot holding is defined as the ratio between the number of slots held by an air carrier (or the air carriers that are part of the same group) at an airport and the total available slots at that same airport (i.e. the airport capacity).

(188) Lufthansa has estimated its slot holding and Air Berlin's slot holding (including the LGW and surplus slots) at an airport on the basis of statistical data collected by the Online Coordination System and e-Airportslots.aero.169

(189) The Commission has checked the overall accuracy of the data submitted by Lufthansa against the information gathered from airport managers and slot coordinators during the market investigation.170

(190) The Commission has calculated two values for Lufthansa's slot holding post-Transaction: (i) its average slot holding during the opening hours of the airport, and (ii) its average slot holding during peak times.

(191) In order to adopt a conservative approach, the Commission has calculated Lufthansa's highest slot holding at any given hour band throughout the whole week (including any peak hour), which exceeds its average slot holding during peak times.

(192) The "gross increment" of Lufthansa's slot holding corresponds to the difference between Lufthansa's slot holding post-Transaction and Lufthansa's slot holding pre-Transaction. Lufthansa's slot holding post-Transaction takes account of (i) the slots to be transferred to Lufthansa through the Transaction, and (ii) the slots held by Air Berlin (including NIKI) that will be returned to the slot pools, which Lufthansa could obtain through the regular allocation process referred to in section 7.1.2.

(193) The "net increment" brought about by the Transaction corresponds to the difference between Lufthansa's slot holding post-Transaction and Lufthansa's slot holding in the situation absent the Transaction. Lufthansa's slot holding in the situation absent the Transaction takes account of the slots held by Air Berlin (including NIKI) to be returned to the slot pools, which Lufthansa could obtain through the regular allocation process referred to in section 7.1.2.171

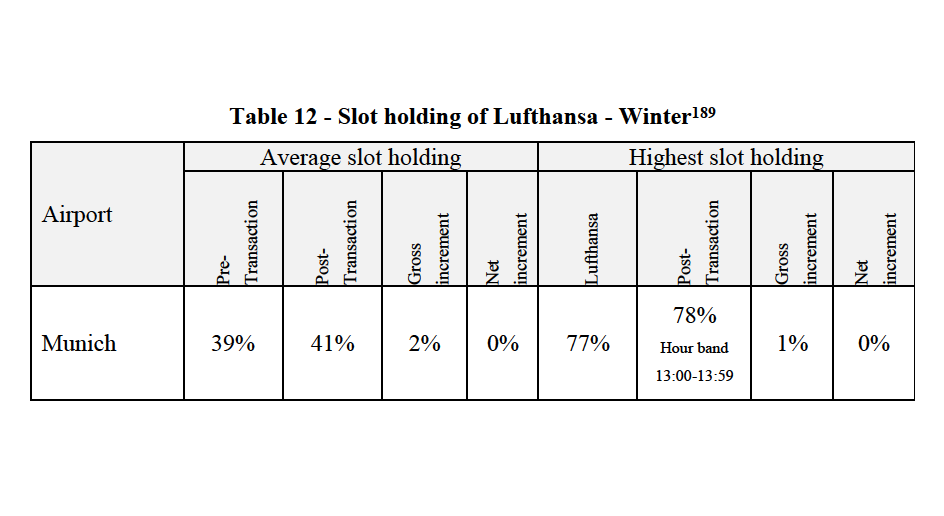

(194) To assess the impact of the Transaction, one should consider Lufthansa's slot holding post-Transaction, as well as the net increment of Lufthansa's slot holding as a result of the Transaction.

8.2.3.2. Airport congestion

(195) The Commission used the qualification as a coordinated airport under the Slot Regulation or, for non-EU airports, as a Level 3 airport under the IATA Worldwide Slot Guidelines172 as a first proxy of the high congestion level of an airport. Indeed, such qualification means that, at these airports, the demand for airport infrastructure, notably slots, significantly exceeds the airport's capacity and the expansion of airport infrastructure to meet demand is not possible in the short term.

(196) For coordinated and Level 3 airports, the Commission has further calculated the actual congestion rate during the opening hours of an airport by dividing the number of slots allocated to all airlines at the airport in a week of the relevant IATA season by the total capacity of the airport in a week (in terms of slots) in the relevant IATA season. The congestion rate of the airport has also been calculated for each hour band by dividing the number of slots allocated to all airlines during the relevant hour band throughout the whole week by the total capacity of the airport during the same hour band throughout the whole week. An average congestion rate during the opening hours of less than 60% would not be prima facie problematic.

(197) The Commission has qualified as "peak times" the hour bands for which the congestion rate at a given airport is very high, and therefore very limited, or no, capacity for entry or expansion is left.

8.2.4. Airport-by-airport assessment

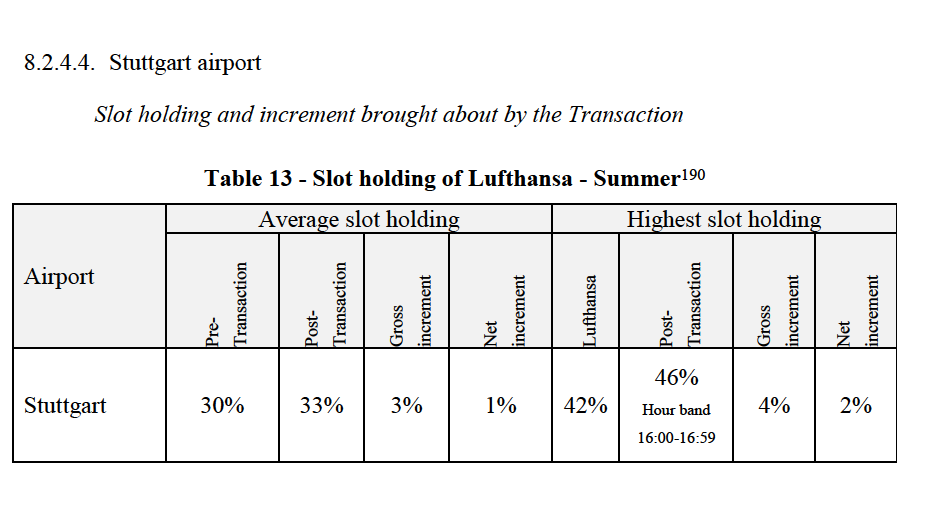

(198) Through the Transaction, Lufthansa would be transferred slots at 19 airports, either for one or both IATA Seasons, as described in paragraph 61. More precisely, Lufthansa would be transferred slots at (i) 16 airports for Summer 2018 IATA Season,173 and (ii) 18 airports for Winter 2017/2018 IATA Season.174 Lufthansa already operates at all these airports, and would thereby expand its portfolio of slots at these airports during the relevant IATA Season.

(199) Among the 16 airports at which Lufthansa would be transferred slots through the Transaction for Summer IATA Season, 12 are coordinated or Level 3 airports.175

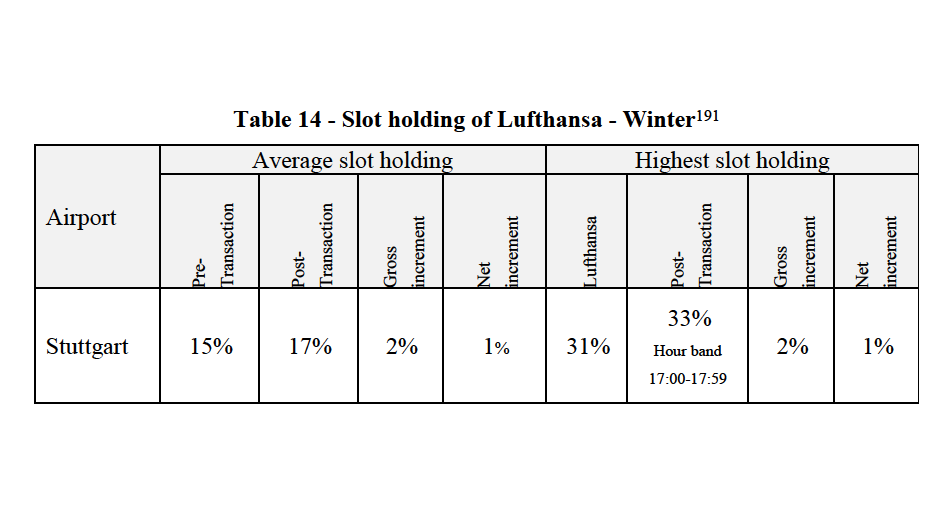

(200) Among the 18 airports at which Lufthansa would be transferred slots through the Transaction for Winter IATA Season, 13 are coordinated or Level 3 airports.176

(201) Therefore, the Commission will assess Lufthansa's slot holding in Summer IATA Season at the 12 Level 3 airports177 and in Winter IATA Season at the 13 Level 3 airports.178

substantial slot portfolio using the remaining 59% of airport capacity, and (ii) as further explained below, there is available capacity at Munich airport (40% on average during Winter 2016/2017 IATA Season). Furthermore, this limited incremental share of slots is unlikely to have any material impact on Lufthansa's slot holding at Munich airport in view of Lufthansa's current slot portfolio, which accounts on average for 39% of the available capacity at this airport.

(225) Lufthansa's highest share during any specific hour band at Munich airport would reach no more than 78% with a net increment of 0%. This hour band corresponds to the most congested hour band at Munich airport (see paragraph 226 below). The Commission considers that this immaterial incremental share of slots is unlikely to have any material impact on Lufthansa's slot holding at Munich airport in view of Lufthansa's current slot portfolio, which accounts on average for 79% at most during any hour band in Winter IATA Season.

Congestion

(226) In Winter 2016/2017 IATA Season, the average congestion rate during the Munich airport's opening hours amounted to 60%. The Munich airport reached its highest congestion level during the hour band 13:00-13:59 UTC with a congestion rate of 93%.

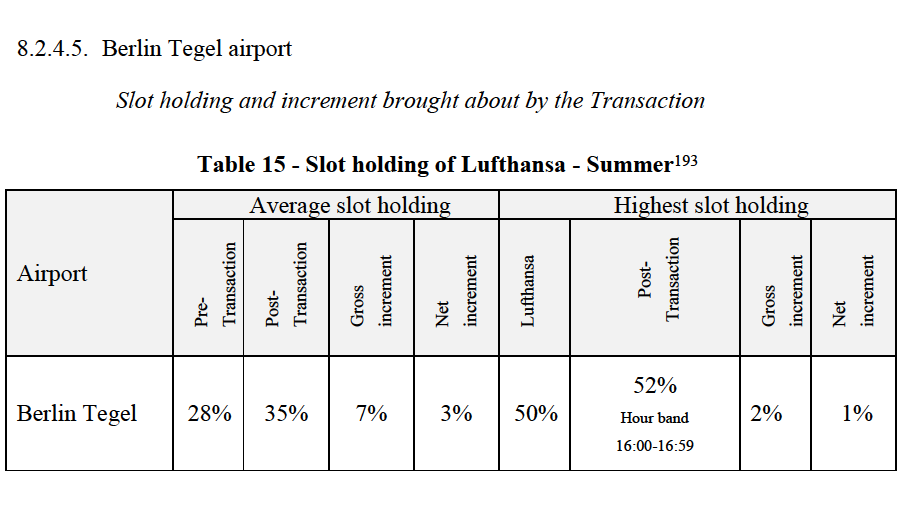

(227) As a consequence, although the Munich airport is coordinated, the actual level of congestion indicates that there are still available slots for entry or expansion at the airports, corresponding to, on average, 40% in winter of available airport capacity.

Conclusion

(228) In Winter IATA Season, given (i) Lufthansa's limited slot holding position at Munich airport post-Transaction (no more than 41% on average), (ii) the limited impact of the Transaction on Lufthansa's slot holding (immaterial net increment), and (iii) the available slot capacity at Munich airport, the Transaction would not materially affect Lufthansa's degree of market power foreclose access of other carriers to the markets for the provision of passenger air transport services.

Congestion

(241) In Summer 2017 IATA Season, the average congestion rate during the opening hours of Berlin Tegel airport amounted to 62%. The Berlin Tegel airport reached its highest congestion level during the hour band 10:00-10:59 UTC with a congestion rate of 83%.

(242) In Winter 2016/2017 IATA Season, the average congestion rate during the Berlin Tegel airport's opening hours amounted to 54%. The Berlin Tegel airport reached its highest congestion level during the hour band 7:00-7:59 UTC with a congestion rate of 73%.

(243) As a consequence, although Berlin Tegel airport is coordinated, the actual level of congestion indicates that there are still available slots for entry or expansion at the airports, corresponding to, on average, 38% in summer and 46% in winter of available airport capacity.

Conclusion

(244) Given (i) Lufthansa's limited slot holding position at Berlin Tegel airport post-Transaction,197 and (ii) the available slot capacity at Berlin Tegel airport in both IATA Seasons, Lufthansa is not likely to have post-Transaction a sufficient degree of market power to foreclose access of other carriers to the markets for the provision of passenger air transport services.

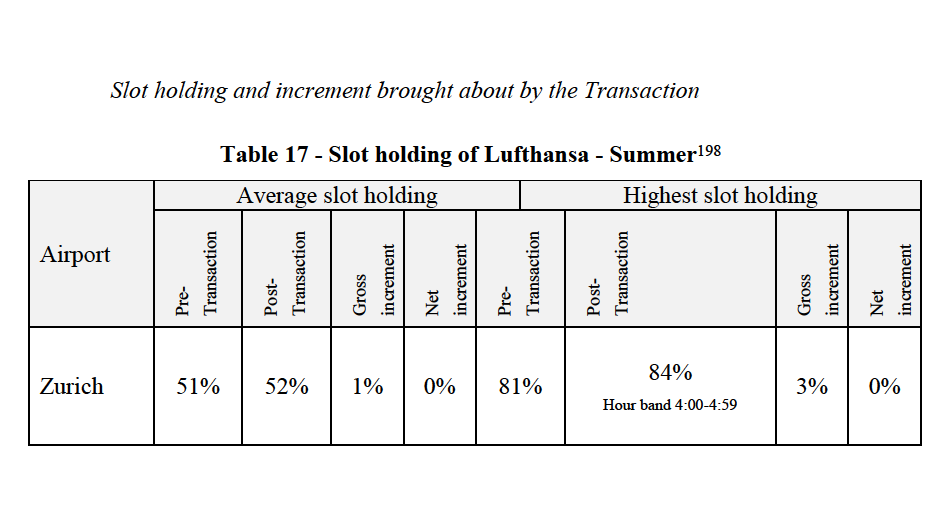

8.2.4.6. Zurich airport

(245) Slots would be transferred to Lufthansa through the Transaction at Zurich airport for Summer IATA Season only. Therefore, the Commission will only assess Lufthansa's ability to foreclose access to the markets for the provision of passenger air transport from or to Zurich airport in Summer IATA Season.

(252) In Summer 2018 IATA Season, Lufthansa estimates that its share in slot holding post-Transaction at each destination airport would be below 17% on average during the relevant airport's opening hours with a net increment inferior to 1%.

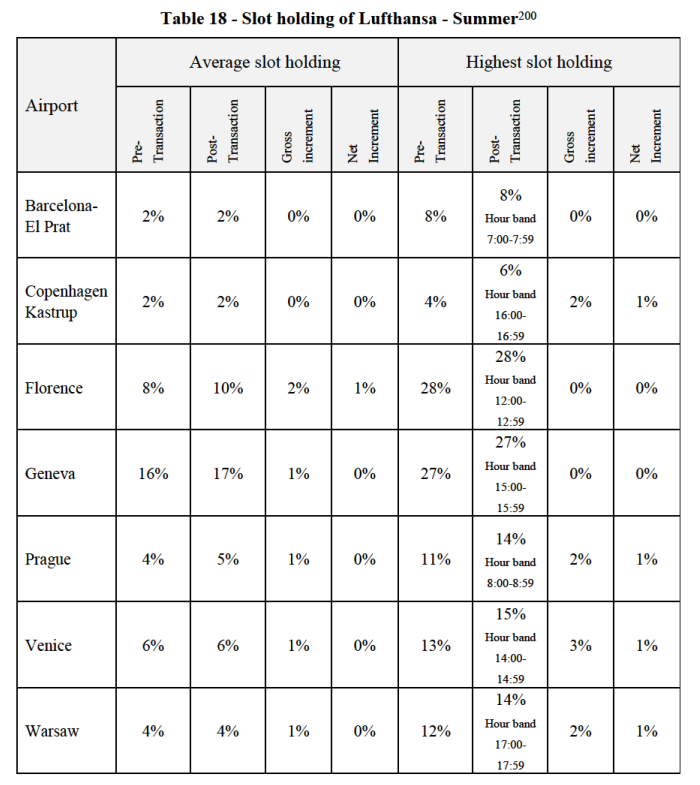

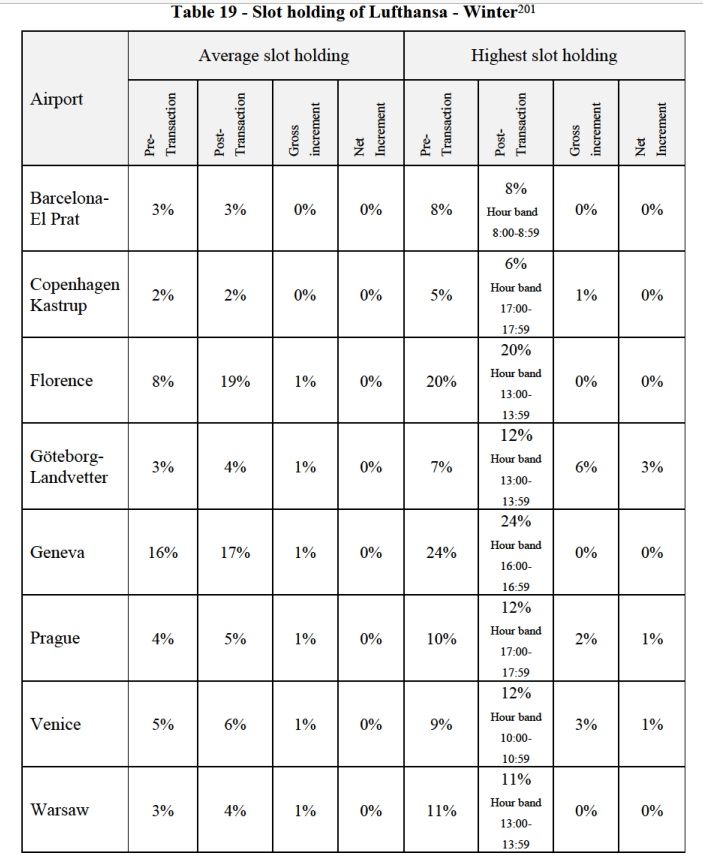

(253) Lufthansa's highest share during any specific hour band at each of the destination airports would reach no more than 28% with a net increment below 1%.