Commission, July 28, 2021, No M.10153

EUROPEAN COMMISSION

Decision

ORANGE / TELEKOM ROMANIA COMMUNICATIONS

Dear Sir or Madam,

(1) On 8 June 2021, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Orange S.A. (“Orange”, France) acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of Telekom Romania Communications S.A. (“TKR”, Romania), currently controlled by Deutsche Telekom AG (“DT”, Germany) (the “Transaction”)3. Orange and TKR are designated hereinafter as the “Parties” and Orange is referred to as the “Notifying Party”.

1. THE PARTIES

(2) Orange is a global telecommunications operator, providing a wide range of electronic communications services mainly in the area of fixed-line, internet and mobile telephony in 27 countries worldwide. In Romania, through its subsidiary Orange Romania, it offers mobile telecommunications services relying on its own mobile network. Orange Romania also offers, to a very limited extent, fixed telephony, fixed internet and TV services relying almost exclusively on third-party infrastructures. Orange is listed on the NYSE Euronext Paris industry and on the New York Stock Exchange. No shareholder has sole or joint control over Orange within the meaning of the Merger Regulation.

(3) TKR is a provider of fixed telecommunications services, TV services and multipleplay bundles to residential and non-residential customers, wholesale services to other telecommunications operators and, to a very limited degree, mobile telecommunications services as a Mobile Virtual Network Operator relying on an agreement with Telekom Romania Mobile Communications S.A. (“TRMC”), all in Romania. TKR is currently under the sole control of DT, through DT’s subsidiary Hellenic Telecommunications Organizations S.A. (“OTE”), which indirectly (through its 100% subsidiary OTE International Investments Ltd) owns 54.01% of TKR shares and voting rights. The remaining shares (45.99%) belong to the Romanian State, but do not confer joint control over TKR within the meaning of the Merger Regulation.

(4) TKR holds a 30% non-controlling minority shareholding in TRMC, the third largest mobile network operator in Romania. TRMC is solely controlled by DT via OTE, which holds 70% of the shares.

2. THE OPERATION

(5) Pursuant to the Share Sale and Purchase Agreement (“the Agreement”) signed on 6 November 2020, Orange Romania will acquire 100% of the shares of OTE International Ltd, and thus indirect control over TKR. The Romanian State will retain its non-controlling minority shareholding in TKR. TKR’s Shareholders’ Agreement will not be affected by the Transaction. Therefore, as a result of the Transaction, Orange will solely control TKR within the meaning of Article 3(1)(b) of the Merger Regulation.

(6) Additionally, as a consequence of the acquisition of TKR, Orange will indirectly acquire 30% of the share capital of its direct competitor TRMC, together with the relating voting and other corporate governance rights.

3. UNION DIMENSION

(7) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million (Orange: EUR 42 270 million; TKR: EUR […])4. Each of them has a Union-wide turnover in excess of EUR 250 million (Orange: EUR […]; TKR: EUR […]), but each does not achieve more than two-thirds of its aggregate Union-wide turnover within one and the same Member State. The notified operation therefore has a Union dimension pursuant to Article 1(2) of the Merger Regulation.

4. RELEVANT MARKETS

(8) In Romania, the Parties’ main activities are complementary. Orange primarily provides retail mobile telecommunications services. It offers retail fixed telephony and retail fixed internet services, mainly through a wholesale access agreement […], as well as business connectivity services through “ad hoc” broadband access agreements with TKR, each addressing the specific needs of its business customers. Orange also offers retail TV services through its own satellite service and via cable based on its wholesale agreement with TKR.

(9) TKR on the other hand is mainly active in the retail supply of fixed telephony and fixed internet access services. It offers mobile telecommunications services based on a wholesale mobile virtual network operator (“MVNO”) agreement with TRMC. TKR also offers retail audio-visual (“AV”) services through cable, satellite and IPTV, as well as business connectivity services. TKR also provides third parties with commercial (non-regulated) wholesale access to its fibre network and cable TV network.

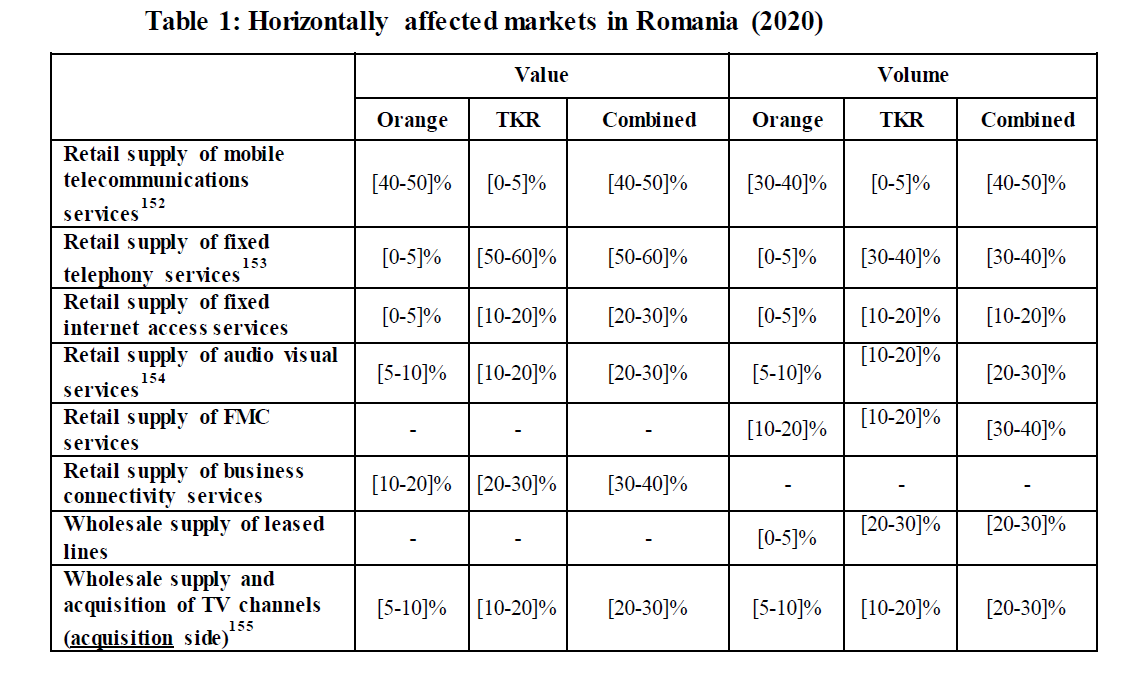

(10) The Parties’ activities mainly overlap in the areas of: (i) fixed-mobile convergent (“FMC”) bundles; (ii) business connectivity services; (iii) retail supply of AV services; and (iv) wholesale supply and acquisition of TV channels (acquisition side). Besides, there are minor horizontal overlaps between the Parties’ activities in: (i) retail fixed telephony services; (ii) retail fixed internet access services; (iii) retail mobile telecommunications services; and (iv) wholesale leased lines.

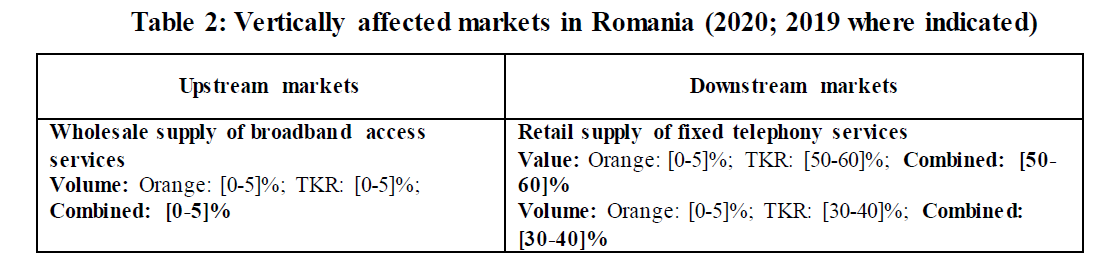

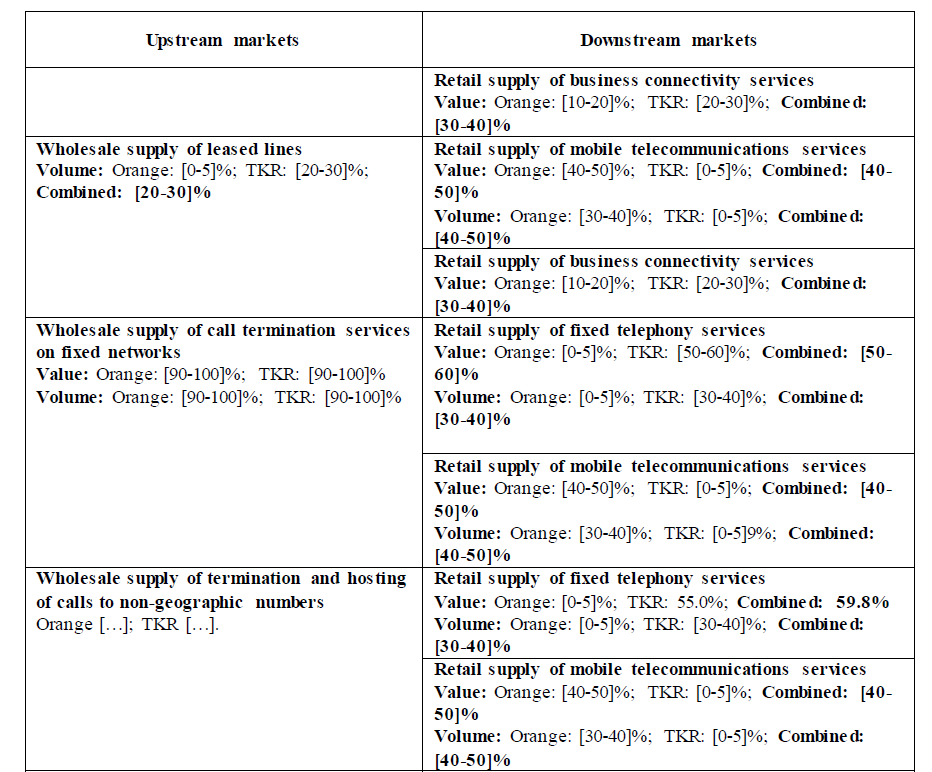

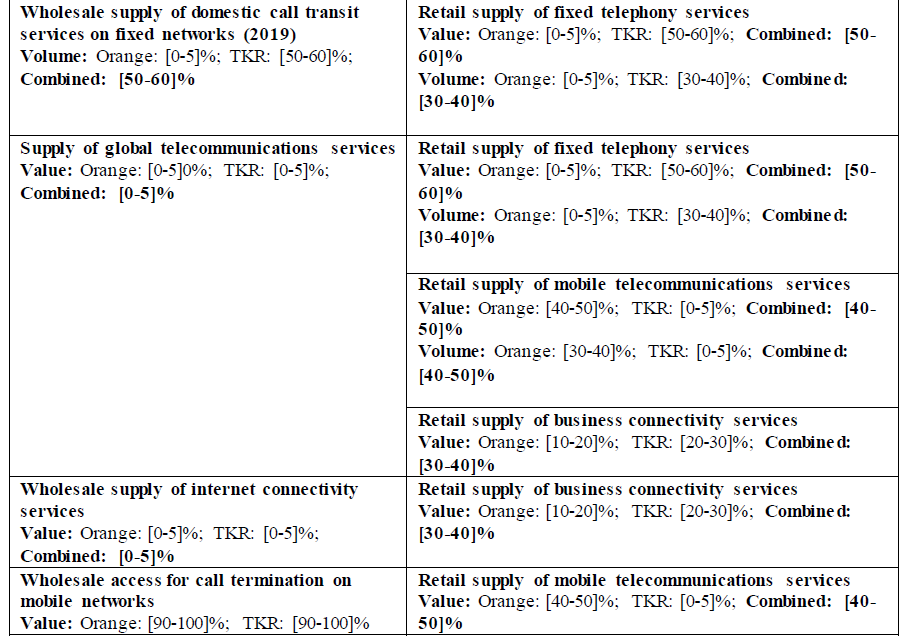

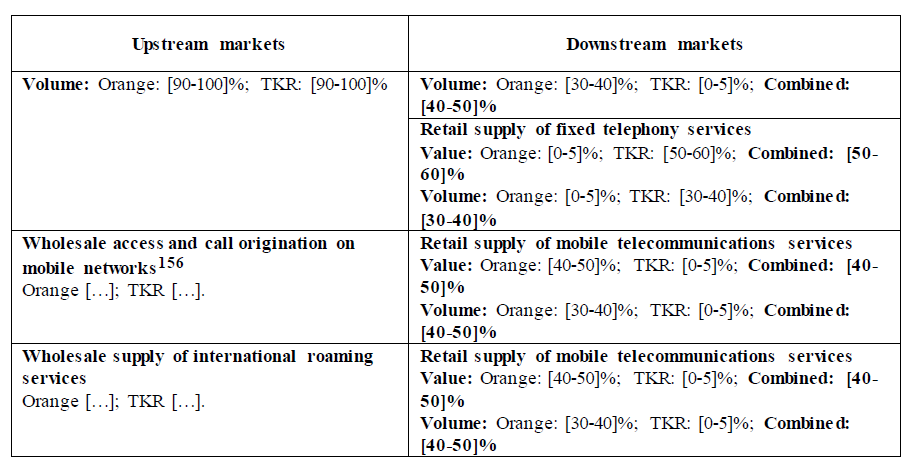

(11) In addition, Orange and/or TKR are present upstream in: (i) wholesale broadband access (TKR); (ii) wholesale services for fixed backhaul (TKR); (iii) wholesale fixed call termination services (Orange and TKR); (iv) wholesale termination and hosting of calls to non-geographic numbers (TKR); (v) wholesale provision of domestic call transit services on fixed networks (TKR); (vi) global telecommunications services (Orange); (vii) wholesale internet connectivity services (Orange); (viii) wholesale mobile call services (Orange and TKR); and (ix) wholesale international roaming services (Orange). Those services are vertically linked to (i) retail mobile telecommunications services, (ii) retail fixed telephony services, and (iii) retail business connectivity services. Further details on the vertical relationships between the Parties are in Table 2 under section 5.2.2.

4.1. Retail supply of mobile telecommunications services

4.1.1. Product market definition

4.1.1.1. Commission precedents

(12) In previous decisions, the Commission has identified an overall retail market for mobile telecommunications services constituting a separate market, distinct from retail fixed telecommunication services. The Commission considered that the retail mobile market does not need to be further segmented based on the type of service (voice calls, SMS, MMS, mobile Internet data services), or the type of network technology (2G, 3G, 4G).5 The Commission considered a number of possible segmentations of the overall retail market for mobile telecommunication services (pre-paid vs post-paid services;6 private customers vs. business customers;7 highvalue vs low-value customers;8 sim-card only (“SIMO”) and handset subscriptions;9 different distribution channels10) but considered that they do not constitute separate product markets but rather segments of the same market .

(13) The Commission considered that Over-the-top (“OTT”) services, whether provided over Wi-Fi or via mobile telecommunications data networks, were not part of the market for mobile telecommunications services, as OTT rely on mobile telecommunications (data) services and/or fixed broadband services to function.11 Finally, the Commission excluded Machine-to-Machine (“M2M”) services from the overall retail mobile market, due to the particular characteristics of the demand for and supply of these services.12

4.1.1.2. The Notifying Party’s view

(14) With respect to the retail market for the supply of mobile telecommunications services, the Notifying Party considers that the relevant product market to be taken into account is the market for the retail supply of mobile telecommunications services.

(15) With respect to M2M services, the Notifying Party considers that the definition of the relevant product market should be left open given the rapid technological and usage changes that this market is still experiencing.

(16) With respect to OTT services, the Notifying Party disagrees with the Commission’s past practice of excluding such services from the retail market for the supply of mobile telecommunications services.

(17) In that respect, the Notifying Party argues that OTT messaging and voice services are used interchangeably with traditional mobile voice and SMS services, and constitute a competitive threat to traditional services offered by mobile network operators (“MNOs”), including voice telephony and SMS. This is the case, in particular, as they are often very cheap or free for consumers, may entail strong networks effects and profit from increasing availability of data access (mobile high speed data and private/public Wi-Fi) and better interoperability while changing between infrastructures (handover and mesh technology).

(18) In that respect, the Notifying Party considers that the market for the retail supply of mobile telecommunications services should include OTT services but however submits that the exact product market can be left open in the present case as the assessment of the Transaction would remain the same.

4.1.1.3. The results of the market investigation and the Commission’s assessment

(19) A majority of respondents to the market investigation indicated that the market for the retail supply of mobile telecommunications services would be distinct from the market for the retail supply of fixed telecommunications services; and that no further segmentation of such market would be warranted.13

(20) With respect to M2M services, as suggested by the results of the market investigation, the Commission considers that such services would fall into a market distinct from the market for the retail supply of mobile telecommunications services. Relevant factors include the fact that M2M services and retail mobile services are characterized by different usage patterns and pricing models. Respondents to the market investigation thus suggested that M2M services are currently mainly used by business customers and not on a large scale. M2M services also usually include data but not voice services and appear to be especially dedicated for the Internet-of- Things (“IoT”) domain.14

(21) With respect to OTT services, the results of the market investigation were mixed. Some competitors suggested that OTT services today would be used interchangeably with traditional mobile telecommunications services while providing additional functionalities. While OTT services would rely on mobile data, mobile devices could also access data services provided via Wi-Fi. In that context, developments such as automatic, SIM-based authentication, multipath TCP protocol and the implementation of seamless handover between Wi-Fi and LTE would suggest enhanced substitutability and would enable the use of OTT services at home, at work as well as on the go.

(22) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the retail supply of mobile telecommunication services, excluding M2M services. The question whether such product market should include OTT services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any considered product market definition.

4.1.2. Geographic market definition

(23) In previous decisions, the Commission found that the market for the retail supply of mobile telecommunications services is national in scope.15

(24) The Notifying Party considers that the relevant geographic market for the retail provision of mobile telecommunications services corresponds to the territory of Romania.

(25) A majority of the respondents to the market investigation indicated that - in line with Vodafone/Certain Liberty Global Assets16 - it would be appropriate to consider that the geographic scope of the market for the retail supply of mobile telecommunications services in the present case is the territory of Romania.17

(26) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the retail supply of mobile telecommunication services is the territory of Romania.

4.2. Retail supply of fixed telephony services

4.2.1. Product market definition

4.2.1.1. Commission precedents

(27) In previous decisions, the Commission considered whether to distinguish between residential and non-residential customers in the market for the retail supply of fixed telephony services.18 While the Commission left the precise scope of the market for the retail supply of fixed telephony services open in several decisions,19 it found in recent decisions that such market does not contain further segmentations20 and that the overall product market for fixed telephony services includes VoIP services.21

4.2.1.2. The Notifying Party’s view

(28) The Notifying Party considers that the exact product market definition can be left open in this case. Additionally, the Notifying Party notes that fixed telephony services are becoming increasingly obsolete, compared with alternative voice services, and have become of little relevance for Romanian customers.

4.2.1.3. The results of the market investigation and the Commission’s assessment

(29) A majority of respondents to the market investigation indicated that an overall market for the retail supply of fixed telephony services both through fixed telephony lines and through VoIP is appropriate.22

(30) With respect to a distinction between local/national and international calls, the results of the market investigation were mixed. While certain submissions from competitors suggested that such distinction would be appropriate due to the often significantly higher international termination rates vis-à-vis national interconnection rates, other respondents indicated that there would be no significant distinctions between such calls.23

(31) With respect to a segmentation between residential and non-residential customers, the results of the market investigation were also inconclusive. While certain competitors suggested that, unlike services to residential customers, services to nonresidential customers would usually include private branch exchange (“PBX”) or Virtual PBX connectivity; others indicated that there are no significant differences between the services provided to either residential or non-residential customers.24

(32) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the retail supply of fixed telephony services including VoIP services, and that the market does not need to be segmented further. In any event, the Transaction does not raise serious doubts as to its compatibility with the internal market or the functioning of the EEA Agreement under any possible product market definition.

4.2.2. Geographic market definition

(33) In Iliad/Play Communications,25 the Commission found the market for the retail supply of fixed telephony services to be national in scope, in particular due to the importance of national regulation in the telecommunications sector and the national basis upon which upstream wholesale services are provided. The Commission has also found such market to be national in scope several other decisions,26 including one decision concerning Romania in 2019.27 At other occasions, the Commission left open the exact geographic market,28 including for Romania in 2008.29

(34) The Notifying Party considers that the relevant geographic market for the retail supply of fixed telephony services corresponds to the territory of Romania.

(35) A majority of respondents to the market investigation indicated that – in line with Vodafone/Certain Liberty Global Assets30 – it is appropriate to consider that the geographic scope of the market for the retail supply of fixed telephony services in the present case is the territory of Romania.31

(36) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the retail supply of fixed telephony services is the territory of Romania.

4.3. Retail supply of fixed internet access services

4.3.1. Product market definition

(37) Internet access services consist of the provision of a telecommunications link enabling customers to access the internet. Internet access may be provided as dial-up ("narrowband") access, as higher bandwidth ("broadband") access via xDSL, a cable modem or mobile broadband technology, or in the form of dedicated access involving leased lines linking one point to the internet and guaranteeing higher levels of performance and security.32

4.3.1.1. Commission precedents

(38) In recent cases (including specifically for Romania33), the Commission has considered that the relevant product market is the overall retail market for the provision of fixed internet access services, including all product types (narrowband, broadband, dedicated access), distribution modes (DSL, cable, fibre, fixed-wirelessaccess (“FWA”)) and speeds/bandwidths, to residential and small business customers, excluding the supply of fixed internet services provided through mobile network infrastructure (i.e. “fLTE”).34

(39) As for large business customers, the Commission indicated that they belong to a separate market for the retail supply of business connectivity services.35

(40) As regards fLTE services in particular, in its past practice (including recent precedents), the Commission did not identify these services as being part of a standalone market. It rather considered that mobile routers/fLTE services should be included in the overall market for retail mobile telecommunications services.36

4.3.1.2. The Notifying Party’s view

(41) The Notifying Party considers that the relevant product market to be taken into account is the market for the retail supply of fixed internet access services excluding mobile internet access services.

4.3.1.3. The results of the market investigation and the Commission’s assessment

(42) In line with the Notifying Party’s submission and the results of the market investigation37, the Commission considers that it would be appropriate to consider an overall retail market for the supply of fixed internet access services, including all product types, distribution modes and speeds/bandwidths, to residential and small business customers, but excluding the supply of fixed internet services provided through mobile network infrastructure.

(43) With regard to fixed internet access services provided through mobile network infrastructure, the respondents to the market investigation confirmed that fixed broadband Internet access services are not substitutable with mobile broadband access services, because “capacities available on fixed broadband, pricing models and customer usage patterns are different than in the case of mobile broadband”.38

(44) With respect to a possible distinction by customer type, the respondents to the market investigation confirmed that fixed internet access services provided to residential and small business customers on the one hand, and large business and government customers on the other hand belong to separate markets. In particular, the majority of competitors indicate that large business and government customers need a dedicated infrastructure and customised solutions vis-à-vis the more standardized and homogeneous requirements of residential and small business customers.39 The Commission further notes that, also from a supply side perspective, there is no perfect substitution between the services provided to the two categories. In fact, while, according to a majority of market participants, switching from the supply to residential and small business customers to large business and government customers would be possible within a short timeframe and at minimal costs,40 a majority of market participants indicated that the reverse (i.e. switching from the supply to large business and government customers to residential and small business customers) could involve significant investments into network infrastructure and technology to offer the necessary coverage.41

(45) The Commission, therefore, concludes that services provided to residential and small business customers, on the one hand, and to large business and government customers belong to separate product markets.

(46) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the retail supply of fixed internet access services, including all product types, distribution modes, and speeds/bandwidth, to residential and small business customers, excluding fixed internet access services provided through mobile network infrastructure.

4.3.2. Geographic market definition

(47) In previous decisions, the Commission has found the market for the retail supply of fixed internet access services to be national in scope,42 including for Romania.43

(48) The Notifying Party considers that the relevant geographic market for the retail supply of fixed internet access services corresponds to the territory of Romania.

(49) A majority of respondents to the market investigation indicated that the geographic scope of the market for the retail supply of fixed internet access services in the present case would be the territory of Romania.44

(50) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the retail supply of fixed internet access services is the territory of Romania.

4.4. Retail supply of audio-visual services

4.4.1. Product market definition

4.4.1.1. Commission precedents

(51) In previous cases, the Commission has identified a relevant product market for the retail supply of audio-visual (“AV”) services, which includes suppliers of linear and non-linear AV services and AV content to end customers. The Commission considered a number of possible segmentations (i) between Free-to-Air (“FTA) and Pay AV services; (ii) within Pay AV services, between linear and non-linear services (Pay-Per-View (“PPV”), Video-on-Demand (“VOD”)); (iii) between distribution technologies (cable, satellite, terrestrial television and Internet Protocol Television (“IPTV”)); and (iv) premium and basic pay AV services, but ultimately left the exact product market definition open.45 4.4.1.2. The Notifying Party’s view

(52) The Notifying Party considers that the relevant product market is the market for the retail supply of TV services. Furthermore, the Notifying Party notes that the possible segmentation between FTA TV and Pay TV can be left open as i) neither of the Parties is active in FTA TV in Romania and ii) due to a strong prevalence of Pay TV subscriptions while FTA TV is practically inexistent in Romania.

(53) The Notifying Party also considers that the market for Pay TV services should not be segmented based on the distribution technologies because (i) satellite is not relevant anymore in Romania; (ii) IPTV is marginal; and (iii) technology conversion46 is widely used and does not affect the substitutability of different distribution technologies.

4.4.1.3. The results of the market investigation and the Commission’s assessment

(54) A majority of respondents to the market investigation indicated that Pay AV services and FTA services would not fall into separate product markets. In particular, Pay AV channels and FTA channels appear to be included in the same monthly subscription. In a recent decision of the Romanian Competition Council (“RCC”), the RCC defined a single, albeit differentiated, market for the provision of audio-visual services (i.e. FTA AV, basic Pay AV, premium Pay AV) to end users was defined.47 Therefore, the Commission considers that the retail market for the provision of AV services in Romania does not need to be further segmented between FTA and Pay AV services, or between basic Pay AV and premium Pay AV services.

(55) With respect to the possible distinction between linear and non-linear services, a majority of respondents to the market investigation indicated that such services would fall into separate relevant product markets. In particular, one respondent noted that such services would usually be sold separately.48 Therefore, the Commission considers that there is an indication that linear and non-linear AV services might belong to separate markets in Romania.

(56) With respect to distribution technologies, from a demand-side perspective, the results of the market investigation indicated that there is substitutability for endcustomers between all technical forms of AV distribution.49 The Commission also notes that this is also in line with the precedents of the RCC, which defined a market for retail TV services including both cable and satellite services (which are the main distribution technologies in Romania).50 The Commission therefore considers that the retail market for the provision of AV services includes all types of distribution technology.

(57) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant service market is the market for the retail supply of AV services encompassing all distribution technologies. The question whether the market should be segmented (i) between FTA and Pay AV services; (ii) basic and premium Pay AV services; and (iii) linear and non-linear services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible product market definition.

4.4.2. Geographic market definition

(58) In previous decisions, the Commission concluded that the market for the retail supply of audio-visual services is national in scope or at most corresponds to linguistically homogenous areas.51 In a case specifically involving Romania, the Commission concluded that such market is national in scope.52 The Commission has further considered the coverage of a service provider’s (cable) network as the geographical scope but ultimately left the exact geographic market definition open in such cases. 53

(59) The Notifying Party considers that the relevant geographic market for the retail supply of audio visual services corresponds to the territory of Romania.

(60) A majority of respondents to the market investigation indicated that the geographic scope of the market for the retail supply of audio-visual services in the present case is the territory of Romania.54

(61) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the retail supply of audio-visual services is the territory of Romania.

4.5. Retail supply of multiple play services

4.5.1. Product market definition

(62) The term "multiple play" relates to product offerings comprising two or more of the following services provided to retail consumers on the basis of a single or multiple contracts by the same provider: mobile telecommunications services, fixed telephony services, fixed internet access and audio-visual services. Multiple play offers comprising two, three or four of these services are referred to as dual play ("2P"), triple play ("3P") and quadruple play ("4P") respectively. 55

(63) Three of the four services, namely fixed telephony services, fixed internet access and AV services, are fixed services as they are provided over a fixed network such as cable, copper or fibre infrastructure. Multiple play offers comprising any combination of two or more of these fixed services without a mobile component are referred to as "fixed multiple play" products. Multiple play offers comprising one or more of these fixed services in combination with a mobile component are referred to as "fixed-mobile multiple play" or "fixed-mobile convergence" ("FMC") products. FMC products may involve a single mobile subscription or more than one mobile subscription combined with the fixed services.56

4.5.1.1. Commission precedents

(64) In previous decisions, the Commission considered but ultimately left open if there exist one or more multiple play markets which are distinct from each of the underlying individual telecommunications services.57 It also noted that, due to different services, delivered over different infrastructures (fixed for 2P and 3P or fixed and mobile for 4P), that are included in the different multiple play bundles, instead of one possible market for multiple play, there could be several candidate multiple play markets: a market for fixed bundles (dual play and triple play) and another separate market for FMC bundles. The possibility for several mobile subscriptions to be included in a quadruple play bundle further complicates the picture.58

4.5.1.2. The Notifying Party’s view

(65) The Notifying Party considers that there is no separate retail market for multipleplay services in Romania notably because these services are mostly sold as “softbundles” where only a discount is offered to consumers when they subscribe to multiple eligible services and therefore where customers are entirely free to discontinue part of the bundle but might lose the discount.

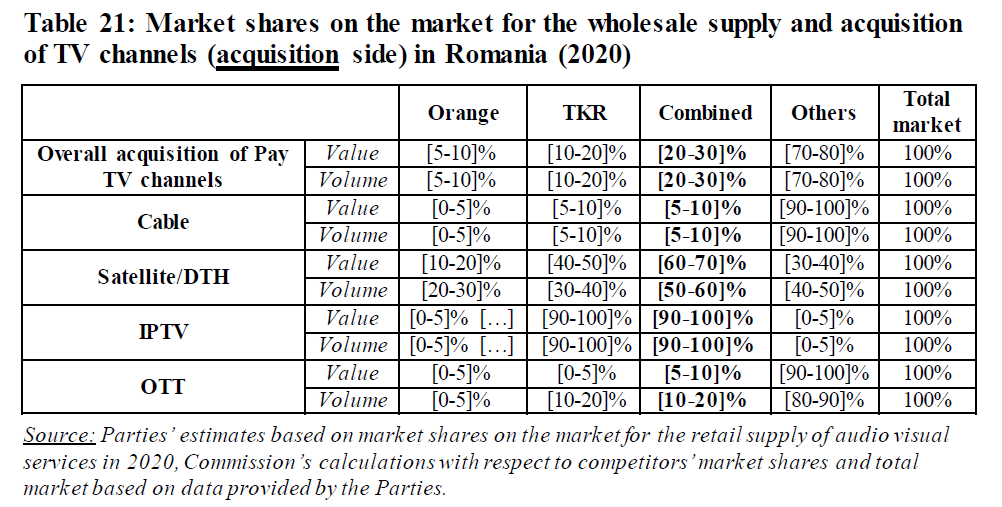

4.5.1.3. The results of the market investigation and the Commission’s assessment

(66) Overall, the results of the market investigation were mixed with respect to the existence of a distinct product market for the retail supply of multiple-play services.59

(67) With respect to demand side substitutability, respondents underlined the existence of one-stop-shop advantages due to the bundling of services.60 Regarding contractual conditions, a majority of market participants indicated that multiple-play services in Romania are more often sold as a combination of standalone fixed and mobile offers from the same provider with various types of benefits attached (“soft bundles”), rather than as multiple play offers containing pre-defined fixed and mobile benefits (“hard bundles”).61 Accordingly, barriers to switching from a multiple-play services package to standalone services appear, on balance, not to be significant, but rather limited to losing certain discounts or the advantage of interacting with one provider instead of multiple ones. 62

(68) With respect to supply side substitutability, the majority of respondents to the market investigation indicated that there would or could be cost savings associated with supplying multiple-play services relative to standalone services, e.g. due to infrastructure advantages, as well as cost savings linked to marketing, service, billing and payment collection activities. Furthermore, respondents to the market investigation indicated the ability to make more competitive offers in the first place as advantages, which would or could reduce churn rates of multiple-play services packages.63

(69) Based on the results of the market investigation, the Commission considers that, due to the fact that different combinations of fixed and mobile telecommunications services are mainly sold as soft bundles in Romania, allowing customers to choose different suppliers for certain parts of the bundle, it appears that suppliers of standalone services are still exerting significant competitive pressure on suppliers of bundles. Moreover, given that there are no standard offers containing pre-defined fixed and mobile benefits, it is difficult to identify which bundles would belong to a separate market or segment.

(70) Therefore, the Commission will assess the effects of the Transaction as regards any possible multiple play bundles, as well as each of the standalone markets.

(71) In light of the above, the Commission considers that the question whether there a separate product market(s) for the retail supply of multiple-play-services exists and whether there are separate markets for fixed bundles and FMC bundles can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.5.2. Geographic market definition

(72) In previous decisions, the Commission considered that the geographic scope of any possible retail market for multiple-play services would be (either regional or) at most national in scope.64 With respect to Romania, the Commission concluded specifically that this market is national in scope.65

(73) The Notifying Party considers that the relevant geographic segment for the retail supply of multiple-play services corresponds to the territory of Romania.

(74) A majority of the respondents to the market investigation indicated that the geographic scope of the market for the retail supply of multiple-play services in the present case is the territory of Romania.66

(75) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the retail supply of multiple play services is the territory of Romania.

4.6. Retail supply of business connectivity services

4.6.1. Product market definition

4.6.1.1. Commission precedents

(76) The retail market for the supply of business connectivity services includes fixed telecommunications services purchased by large businesses, enterprises and public sector customers in order to provide data connectivity between multiple sites.

(77) In previous decisions, the Commission considered potential subdivisions into (i) broadband access for large business customers67; (ii) leased lines68; and (iii) virtual private networks (“VPN”) services69, but ultimately left the question open.70 The Commission also distinguished between two separate markets for connectivity services. Firstly, connectivity services offered to residential and small business customers, which are part of the retail market for fixed internet access services; and secondly, connectivity services to large business customers, which are part of the retail market for business connectivity services. This is because of the peculiar requirements and purchase processes of larger business customers.71

4.6.1.2. The Notifying Party’s view

(78) The Notifying Party considers that the relevant product market is the market for the supply of retail business connectivity services. The Notifying Party emphasises that business connectivity clients often purchase custom-made solutions that include several elements, and that leased lines tend to be replaced by VPN and broadband access services.

4.6.1.3. The results of the market investigation and the Commission’s assessment

(79) The results of the market investigation confirm that there is no need to distinguish between residential and small business customers, and that these customers should not be included in the market for business connectivity services along with connectivity services to larger business customers, notably due to different customer requirements.72

(80) With respect to a potential segmentation into broadband access; leased lines; and VPN services, a majority of respondents to the market investigation confirmed that such segmentation would be appropriate. While a number of respondents noted that such services should be treated individually due to different technical characteristics73, others nevertheless indicated that business customers could and would easily switch between such services and that it is common for business customers to purchase a mix of (some of those) services.74

(81) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the retail supply of business connectivity services to large businesses and public sector customers, excluding the supply of such services to residential and small business customers. The question whether such product market should be further segmented into (i) broadband access for large business customers, (ii) leased lines, and (iii) VPN services can be left open, as the Transaction does not raise competition concerns under any possible product market definition.

4.6.2. Geographic market definition

(82) In previous decisions, the Commission found the market for the retail supply of business connectivity services to be national in scope,75 including for Romania.76

(83) The Notifying Party agrees with the Commission and considers that the relevant geographic market for the retail supply of business connectivity services corresponds to the territory of Romania.

(84) A majority of respondents to the market investigation indicated that the geographic scope of the market for the retail supply of business connectivity services in the present case is the territory of Romania.77

(85) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the retail supply of business connectivity services is the territory of Romania.

4.7. Wholesale supply of leased lines

4.7.1. Product market definition

(86) Wholesale leased lines are part-circuits that allow telecommunications providers to connect their own networks to end user sites for the supply of business connectivity services. In addition, wholesale leased lines are an input for the provision of fixed and mobile telecommunications services.78

(87) In particular, backhaul services are the connections between the antennae in a mast and the switches in the core network and are used to ensure the proper functioning of a mobile network. Backhaul networks can be comprised of wireless backhaul (i.e. microwaves) or fixed backhaul. MNOs have typically operated their own microwave backhaul while fixed backhaul has been provided by fixed network operators. Fixed backhaul services are provided on either (i) fibre optic cables or (ii) copper cables. However, wireless backhaul can be used in areas where fixed backhaul is not available. 79

4.7.1.1. Commission precedents

(88) In previous decisions, the Commission considered possible segmentations of the market for the wholesale supply of leased lines according to (i) network layer (trunk vs. terminating (i.e., backhaul) segments of leased lines); (ii) speed (terminating leased lines with bandwidth below 2 Mbps vs. above 2 Mbps); (iii) passive or active nature of the line (the distinction corresponding to dark fibre on the one hand and managed leased lines and Ethernet services with guaranteed bandwidth on the other); (iv) leased lines with traditional interfaces vs. Ethernet services with guaranteed bandwidth; and (v) transmission means (wireless, fiber, copper lines), but ultimately left open the exact product market definition.80 The Commission has further considered a potential segment for fixed backhaul services.81

4.7.1.2. The Notifying Party’s view

(89) The Notifying Party considers that the exact product market definition for the wholesale supply of leased lines can be left open. With respect to wholesale fixed backhaul services, the Notifying Party argues that such service do not fall into a separate product market.

4.7.1.3. The results of the market investigation and the Commission’s assessment

(90) With respect to a segmentation by transmission means (i.e. wireless, fibre and copper lines), the results of the market investigation were mixed. Several respondents submitted that while there are certain differences between technologies for layer 1, specifically in relation to bandwidth/speed, all technologies ultimately serve the same purpose of providing wholesale leased lines as a means to connect different parts of the network of a telecommunications operator. For layer 2, there is basically no differentiation between technologies as services are provided packet-based, i.e. a certain bandwidth/speed is agreed. 82

(91) With respect to a segmentation by network layer (trunk segments and terminating segments), a majority of market participants that responded to the market investigation indicated that such segmentation would not be relevant. In particular, one respondent noted that, once leased lines are installed, there is no differentiation between the capacity used for trunk segments and that allocated to terminating segments.83

(92) With respect to a segmentation based on bandwidth/speed, above and below 2Mbps, a majority of market participants that responded to the market investigation indicated that such segmentation would not be meaningful. In particular, respondents noted that a speed of 2 Mbps would be too slow for today’s requirements.84

(93) With respect to a segmentation between active and passive infrastructure, a majority of market participants that responded to the market investigation indicated that such segmentation would not be meaningful.85

(94) Based on the above, the Commission considers that the product market wholesale leased lines in Romania does not need to be segmented based on transmission means, bandwidth/speed or between active and passive infrastructure.

(95) With respect to a separate segment for fixed backhaul services (i.e., within a larger overall market of wholesale leased lines), the results of the market investigation were mixed. While certain respondents noted that fixed backhaul services and leased lines would represent different services, others indicated that fixed backhaul would be only one way to use wholesale leased lines among others with similar requirements for speed and bandwidth.86 The Commission therefore considers that the market investigation provided no clear indication that fixed backhaul services should belong to a product market separate from the product market for wholesale leased lines.

(96) In light of the above, the Commission considers that, for the purpose of this Decision, the exact product market definition of the wholesale market for the supply of leased lines and the question whether it includes wholesale fixed backhaul services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.7.2. Geographic market definition

(97) In previous decisions, the Commission found that the relevant geographic market for the wholesale supply of leased lines (and possible sub-segments) is national in scope,87 including for Romania.88

(98) The Notifying Party considers that the relevant geographic market for the wholesale supply of leased lines corresponds to the territory of Romania.

(99) A majority of respondents to the market investigation indicated that – in line with the Commission’s findings in the case Vodafone/Certain Liberty Global Assets89 – the market for the wholesale supply of leased lines in the present case is the territory of Romania.90

(100) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the wholesale supply of leased lines is the territory of Romania.

4.8. Wholesale supply and acquisition of TV channels

4.8.1. Product market definition

(101) In the wholesale market for TV channels, TV broadcasters supply linear channels that retail TV providers either purchase or carry in order to provide audio-visual services to end-users. In particular, TV broadcasters package the TV content that they have acquired or produced in-house in order to create linear TV channels. Subsequently, retailers of TV services incorporate those TV channels in their TV offerings to final viewers.91

4.8.1.1. Commission precedents

(102) In previous decisions, the Commission identified a market for the wholesale supply and acquisition of TV channels.92 Within that market, the Commission has identified separate product markets for: (i) FTA TV channels; and (ii) Pay TV channels93 and more recently left the exact product market definition open.94

(103) In addition, the Commission found that within the Pay TV channels market, there are different segments95 or, more recently, product markets96 for (i) premium Pay TV channels and (ii) basic Pay TV channels. In certain cases, the Commission has considered FTA channels to be part of the market for basic Pay TV channels.97

(104) Further, the Commission also examined a number of other potential segmentations, including: (i) by genre or thematic content (such as films, sports, news, youth, and others);98 (ii) between linear and non-linear;99 and (iii) between the different means of infrastructure used to deliver channels to the viewer (cable, satellite, terrestrial or IPTV)100 but ultimately left the exact market definition open. 4.8.1.2. The Notifying Party’s view

(105) The Notifying Party considers that the relevant product market to be taken into account is the market for wholesale supply and acquisition of TV channels irrespective of the different types of infrastructures, notably because satellite is not relevant anymore in Romania, IPTV is marginal, and technology conversion (e.g. the conversion of fibre into cable or IPTV signal to facilitate the connection to customers’ devices) is widely used as it is required in all homes where TV services are based on fibre, cable or xDSL infrastructures. The Notifying Party explains that this conversion does not affect the substitutability of different distribution technologies as it does not materially differ across input infrastructure (e.g. between fibre, cable or xDSL). For instance, Digi converts fibre to cable TV and TKR converts fibre to cable TV or to IPTV (depending on the customer requirements).101

4.8.1.3. The results of the market investigation and the Commission’s assessment

(106) Based on the replies to the market investigation,102 the Commission considers that the segmentation of the value chain for audio visual content in Romania into i) the (upstream) market for the licensing of audio visual content; ii) the (intermediate) market for the wholesale supply of TV channels; and iii) the (downstream) market for the retail supply of TV services is accurate.

(107) With regard to the distinction between FTA TV channels and Pay TV channels, the majority of distributors and of suppliers of TV channels indicated that the distinction is relevant in Romania.103 In particular, a number of responses by suppliers of TV channels pointed to financial differences between FTA TV and Pay TV channels (i.e., in terms of investments needed, pricing models for end consumers).104

(108) However, a number of responses by TV channel suppliers indicated that the development of new platforms and technologies might justify disregarding a distinction between FTA TV channels and Pay TV channels.105 Furthermore, a supplier of TV channels indicated that there is no significant difference, from a demand-side perspective, between FTA TV channels and Pay TV channels in Romania. This is because FTA and Pay TV channels are packaged the same way and offer similar programming suited for similar target audiences.106

(109) With respect to a further segmentation between basic Pay TV channels and premium Pay TV channels, the results of the market investigation are inconclusive. While a majority of respondents supported such further segmentation, several well substantiated responses submitted that the distinction is not relevant in Romania.107

(110) On the one hand, a number of market participants indicated that basic and premium Pay TV channels had different wholesale prices and that certain premium Pay TV channels would be made available to end consumers for an additional fee. One response in particular suggested different target audiences and different levels of local content between basic and premium TV channels.

(111) On the other hand, a supplier of TV channels indicated that more generalist channels attract the highest audience shares and that high quality local content attracts audience shares at least on par with major US films. In addition, local “basic” channels have a significantly high content-refresh rate. Moreover, according to this submission, the hypothetical distinction between basic and premium would not be clear-cut, that both types of channels compete for the same audience and that “premium” content is also available via non-linear services. Finally, from a wholesale perspective, the total fees paid by retail TV distributors for “premium” channels would be comparable or even lower than the total fee for basic packages.108

(112) Based on the above, the Commission considers that the wholesale market for the acquisition and supply of TV channels in Romania should be segmented between FTA channels and Pay TV channels, as well as between premium Pay TV and basic Pay TV channels.

(113) With respect to a distinction of separate markets based on genre or thematic content, the results of the market investigation were mixed. On the one hand, the market investigation indicated that certain types of content might be distinctive due to their particularly high cost and that the Romanian regulator would require operators to group TV channels by type of content offered. On the other hand, while there are many specialised channels, “generalist” channels which cross-cut the discussed distinction also exist. In addition, there might be partial, temporary competition, e.g., between a news channel and an entertainment channel, if the news channel offers a sports competition. Finally, the switching behaviour of viewers who are unhappy with the program they watch, would indicate high demand side substitutability for several switching scenarios.109 The Commission therefore considers that the distinction of separate markets based on genre or thematic content remains relevant.

(114) Generally, with respect to a distinction of separate markets based on the infrastructure/platform used for the delivery to the viewer (cable, satellite, digital video broadcasting, IPTV), the results of the market investigation were inconclusive.110

(115) On the one hand, the market investigation indicated differences in terms of image quality and number of channels as well as the fact that the must-carry status of a channel does not apply to delivery via satellite infrastructure. Moreover, satellite is the prevalent infrastructure in rural areas, representing 27% of total Romanian households, while cable is prevalent in urban areas. Even in areas where both satellite and analogue cable infrastructure are available, the signal quality and number of channels via satellite infrastructure would be better than via cable networks. The following switching barriers were indicated i) technical barriers due to satellite signal reception, ii) administrative barriers due to the need for permission by owners’ associations and/or local authorities, iii) aesthetic barriers due to the visibility of satellite reception equipment, and iv) legal barriers due to cancellation fees payable by customers who would cancel their subscription before the minimum term of usually two years. Also, it was submitted that satellite TV offers are usually sold on a standalone basis, rather than part of a multiple-play bundles (unlike other infrastructures).111

(116) On the other hand, a number of respondents to the market investigation indicated that major distributors provide TV signal through at least two types of infrastructures/platforms and that the variation in terms of quality is insignificant. Moreover, it was also suggested that customers, especially in urban areas, have multiple types of infrastructures/platforms to choose from. In that context, even though customer choice could be limited in areas where only one type of technology would be available, the breadth of types of infrastructures/platforms available to customers increases steadily at national level. Further, in terms of pricing, different types of infrastructures/platforms do not differ to a degree that would suggest the existence of separate markets.112

(117) Based on the above, the Commission considers that the wholesale market for the supply of TV channels should not be further segmented by type of infrastructure used for the delivery of the signal to the end-customer. This is because several types of infrastructure are available to almost all end-customers and the barriers to switching mentioned under paragraph (116) do not appear to be significant.

(118) With regard to the distinction between the wholesale supply and acquisition of TV channels for linear and non-linear distribution, the market investigation did not provide any elements indicating that the Commission should depart from its precedents.

(119) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market for the wholesale supply and acquisition of TV channels encompasses all infrastructures/distribution technologies. The question whether the product market should be further segmented i) between FTA TV channels and Pay TV channels; ii) between basic Pay TV channels and premium Pay TV channels; iii) by genre/thematic content; and (iv) between linear and non-linear can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.8.2. Geographic market definition

(120) In previous decisions, the Commission considered that the wholesale supply and acquisition of TV channels is either national in scope or comprises a broader (or narrower) linguistically homogeneous area,113 including for Romania.114

(121) The Notifying Party considers that the relevant geographic market for the wholesale supply and acquisition of TV channels corresponds to the territory of Romania.

(122) A majority of responses by suppliers of TV channels indicated that they would license (most of) their TV channels on a national basis. In particular, a number of respondents noted that content produced in-house could be distributed worldwide, while acquired content could only be distributed on a geographic/territorial basis, in compliance with the rights granted by the licensors. At the same time, another respondent noted that certain distributors with operations in several countries prefer EEA-wide or regional licenses.115

(123) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the wholesale supply and acquisition of TV channels is the territory of Romania.

4.9. Wholesale supply of broadband access

4.9.1. Product market definition

(124) Wholesale broadband access includes different types of access to fixed connections that allow internet service providers to provide services to end consumers. It comprises physical access at a fixed location, such as LLU; non-physical or virtual network access, such as bitstream access, at a fixed location; and resale of a fixed provider’s internet access services.

(125) In previous decisions, the Commission defined a separate market for wholesale broadband access. The Commission considered to further segment such market by i) type of access (LLU, bitstream, resale of the incumbent’s offering); and ii) infrastructure (standalone access to DSL, standalone access to cable, access to cable for TV and internet together) but ultimately left the exact product market open.116

(126) The Notifying Party considers that the relevant product market to be taken into account is the market for wholesale broadband access.

(127) The results of the market investigation did not provide reasons to depart from the Commission’s previous approach.

(128) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the wholesale supply of broadband access. The question whether such market should be segmented by i) type of access or ii) infrastructure can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.9.2. Geographic market definition

(129) In previous decisions, the Commission found indications that the market for the wholesale supply of broadband access is national in scope, but ultimately left open the exact geographic market definition.117

(130) The Notifying Party considers that this definition can be left open given that the Transaction will not give rise to any competition concern.

(131) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(132) In light of the above, the Commission considers that, for the purpose of this Decision, the exact geographic scope of the market for the wholesale supply of broadband access can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.10. Wholesale supply of call termination services on fixed networks

4.10.1. Product market definition

(133) Call termination is the service provided by a network operator on the supply side to other network operators on the demand side, whereby a call originating in a demand side operator’s network is delivered to a user in the supply side operator’s network. This service is required by every originating operator, as it is necessary for its customers to be able to communicate with the customers located on other networks. Call termination is therefore a wholesale service that is resold or used as an input for the provision of downstream retail telephony and mobile services. 118

4.10.1.1. Commission precedents

(134) In the past, the Commission has concluded that each individual network (both in mobile and in fixed networks) constitutes a separate market for termination, as there is no substitute for call termination in each individual network as the intended recipient can only be reached by the operator transmitting the outbound call through the operator of the network to which the recipient is connected.119 Each individual network constitutes a separate product market.

(135) Further, in previous decisions, the Commission considered wholesale call termination services on fixed network to be a distinct market from the market for the wholesale supply of international voice carrier services.120

4.10.1.2. The Notifying Party’s view

(136) The Notifying Party considers that termination in each individual fixed network constitutes a separate product market.

4.10.1.3. The results of the market investigation and the Commission’s assessment

(137) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(138) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for wholesale supply of call termination services on fixed networks that is a distinct market from the market for the wholesale supply of call termination services on mobile networks.

4.10.2. Geographic market definition

(139) In previous decisions, the Commission considered the geographic market for the wholesale supply call termination services in fixed networks to be national in scope,121 including for Romania.122

(140) The Notifying Party considers that the relevant geographic market for the wholesale supply of call termination services on fixed network corresponds to the territory of Romania.

(141) The results of the market investigation did not provide reasons to depart from the Commission’s previous approach.

(142) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the supply of wholesale call termination services on fixed networks is the territory of Romania.

4.11. Wholesale supply of termination and hosting of calls to non-geographic numbers

4.11.1. Product market definition

(143) Voice calls are not only made to geographic numbers but also to non-geographic numbers. A non-geographic number is a number associated with a country, but not to any single geographic location within that country. Non-geographic number services are less frequently used than standard services and are typically used for free and paid information services, for example, for helpdesks, subscription services, TV voting lines etc.

(144) When a caller initiates a call to a non-geographic number, the call is automatically transferred from the originating operator to the terminating operator hosting the service provider that operates the service related to the non-geographic number, irrespective of the location.

(145) Unlike ordinary call termination services, call origination and call termination regulation does not apply to these numbers. Therefore, different revenue sharing agreements exist between the originating operator, the terminating operator, and the service provider.123

4.11.1.1. Commission precedents

(146) In previous decisions, the Commission considered that there is a product market for the wholesale supply of termination and hosting of calls to non-geographic numbers without it being necessary to consider further possible segmentations.124

4.11.1.2. The Notifying Party’s view

(147) The Notifying Party considers that the relevant product market to be taken into account is the market for the wholesale supply of termination and hosting of calls to non-geographic numbers.

4.11.1.3. The results of the market investigation and the Commission’s assessment

(148) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(149) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the wholesale supply of termination and hosting of calls to non-geographic numbers that is distinct from other wholesale termination services.

4.11.2. Geographic market definition

(150) In previous decisions, the Commission considered that the geographic scope of the wholesale market for the supply of termination and hosting of calls to nongeographic numbers is national.125

(151) The Notifying Party considers that the relevant geographic market for the wholesale supply of termination and hosting of calls to non-geographic numbers corresponds to the territory of Romania.

(152) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(153) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the wholesale supply of termination and hosting of calls to non-geographic numbers is the territory of Romania.

4.12. Wholesale supply of domestic call transit services on fixed networks

(154) Domestic call transit on a fixed network is a wholesale service provided by a third party where there is no direct connection between originating communication providers and terminating communication providers.

(155) In previous decisions, the Commission found that the market for the wholesale supply domestic transit services in fixed networks to be a separate product market, notably from the market for global telecommunications services.126

(156) The Notifying Party considers that the relevant product market to be taken into account is the market for the wholesale supply of domestic call transit services on fixed networks. The Notifying Party notes that the market for the call transit services on fixed networks is shrinking and likely to disappear in the future.

(157) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(158) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the wholesale supply of domestic call transit services on fixed networks.

4.12.1. Geographic market definition

(159) The Commission found that the market for the wholesale supply of domestic transit services in fixed networks is national in scope.127

(160) The Notifying Party considers that the relevant geographic market for the wholesale supply of domestic call transit services on fixed networks corresponds to the territory of Romania.

(161) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(162) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the wholesale supply of domestic call transit services on fixed networks is the territory of Romania.

4.13. Supply of global telecommunications services

4.13.1. Product market definition

(163) Global telecommunications services (GTS) are telecommunications services linking a number of different customer locations, generally in at least two different continents and across a larger number of different countries. They are generally purchased by multinational companies with presence in many countries and a number of continents. The services provided are enhanced services to provide customers with package solutions including virtual private networks (“VPN”) for both voice and data services and advances functionalities. 128

(164) Global telecommunications services are supplied at retail level and wholesale level. In the latter case, they can also be referred to as “international carrier services”. Wholesale global telecommunications services comprise (i) the lease of transmission capacity and (ii) the provision of related services to third party telecommunications traffic carriers and service providers and are an input for retail global telecommunications services. 129

(165) While leaving the exact product market definition open, the Commission considered a possible distinction between the retail supply global telecommunications services and the wholesale supply of global telecommunications services130 as well as between the lease of transmission capacity and the provision of related services to third-party carriers.131

(166) The Notifying Party considers that the relevant market to be taken into account is the overall market for the supply of global telecommunications services comprising both retail and wholesale services as well as that the exact definition may be left open in the present case.

(167) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(168) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the supply of global telecommunications services. The question whether to segment such market between i) retail and wholesale services; and ii) the lease of transmission capacity and the provision of related services to third parties can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.13.2. Geographic market definition

(169) In previous decisions, the Commission considered that the geographic market for the supply of global telecommunications services, both at retail and wholesale levels, is likely worldwide while leaving its exact geographic scope open.132

(170) The Notifying Party considers that the market for the supply of global telecommunication services is worldwide in scope.

(171) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(172) In light of the above, the Commission considers that, for the purpose of this Decision, the exact geographic scope of the market for the supply of global telecommunications services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.14. Wholesale supply of internet connectivity services

(173) Internet connectivity services allow corporate customers to be present on the internet by providing access to the entire routing table of the global internet or to a subset of the same, in which case the customer will need to cover the totality of its needs by means of a multi-homing strategy. Connectivity to the internet can be achieved (i) by the purchasing of transit services, (ii) by means of peering with selected networks, or (iii) by means of a combination of the two. Entities which do not connect directly to the internet may also call upon hosting providers, who aggregate hosting needs and procure in turn internet connectivity for their customers.133 Whilst global coverage is a primary requirement, more specific performance criteria also enter into a customer's internet connectivity strategy such as latency, reliability, speed and minimization of traffic-related costs.

(174) Transit is a service whereby a customer pays for access to all or a large part of the internet, with performance characteristics which may vary according to the destination of the traffic. Peering, on the other hand, whether settlement-free or paid, provides access to individual networks but no further onward connectivity. Providers of transit services will in turn use a combination of peering relationships and paid commercial relationships with other transit providers in order to provide global internet coverage. A transit provider which does not purchase transit services from other providers because it is able to reach the entire internet merely by means of peering relationships is referred to as a "Tier 1" transit provider.

(175) Operators of retail internet access networks, sometimes referred to as "eyeball networks", procure internet connectivity in the same way as any other corporate customer, and may themselves also provide wholesale internet connectivity services. Certain internet access providers ("IAPs") offer transit services, whereas many offer direct connectivity to their own network and subscribers. To the extent that the IAP purchases transit services, these may also be used to reach its users. The end users of a given IAP can also be reached by means of relationships with those networks which peer with the IAP in question.134

4.14.1. Product market definition

(176) In previous decisions, the Commission considered the existence of an overall market for the wholesale supply of internet connectivity services, including both transit and peering services and potentially further segmented between transit and peering services but ultimately left the exact product market definition open.135 Further, the Commission considered, but ultimately left open a possible segmentation of the product market for wholesale internet connectivity services between Tier-1 transit providers and Tier-2 transit providers.136

(177) The Notifying Party considers that the relevant product market to be taken into account is the market for the wholesale supply of internet connectivity services.

(178) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(179) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the wholesale supply of internet connectivity services. The question whether such market a) includes both transit and peering services; b) should be further segmented between transit and peering services; and c) can be further segmented between Tier-1 transit providers and Tier-2 transit providers can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.14.2. Geographic market definition

(180) The Commission previously found the market for the wholesale supply of internet connectivity services to be either global or regional in scope.137

(181) The Notifying Party considers the relevant market to be at least regional if not global in scope but submits that the market definition may be left open given the absence of overlap.

(182) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(183) In light of the above, the Commission considers that, for the purpose of this Decision, the exact geographic scope of the market for the wholesale supply of internet connectivity services can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any possible product market definition.

4.15. Wholesale supply of access and call termination services on mobile networks

(184) Call termination is the service provided by a network operator on the supply side to other network operators on the demand side, whereby a call originating in a demand side operator’s network is delivered to a user in the supply side operator’s network. This service is required by every originating operator, as it is necessary for its customers to be able to communicate with the customers of other networks. Call termination is therefore a wholesale service that is resold or used as an input for the provision of downstream retail telephony and mobile telecommunications services.138

4.15.1. Product market definition

(185) In previous decisions, the Commission has identified relevant markets for the wholesale supply of access and call termination services on mobile and fixed networks. Further, the Commission found that there is no substitute for call termination on each individual network, as the operator transmitting the call can reach the intended recipient only through the operator of the network to which the recipient is connected and thus concluded that each individual network, either fixed or mobile, constitutes a separate market. 139

(186) The Notifying Party considers that the relevant product market to be taken into account is the market for wholesale supply of access and call termination services on mobile networks.

(187) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(188) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the wholesale supply of access and call termination services on mobile networks.

4.15.2. Geographic market definition

(189) In previous decisions, the Commission considered the geographic market for the wholesale supply of access and call termination services on mobile networks to be national in scope,140 including for Romania.141

(190) The Notifying Party agrees with the Commission and considers that the relevant geographic market for the wholesale supply of access and call termination services on mobile networks corresponds to the territory of Romania.

(191) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(192) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the wholesale supply of access and call termination services on mobile networks is the territory of Romania.

4.16. Wholesale supply of access and call origination services on mobile networks

4.16.1. Product market definition

(193) MNOs provide wholesale access and call origination services which enable operators without their own network, namely MVNOs and Service Providers, to have access to one or more of the MNOs’ networks in order to provide mobile telecommunications services to end customers. “Full” or “thick” MVNOs maintain their own core infrastructure and use MNOs only for access to a radio network. By contrast, “light” or “thin” MVNOs do not have their own infrastructure and rely entirely on the infrastructure of an MNO. 142

(194) In previous decisions, the Commission considered network access and call origination to be part of the same product market as both services are considered as key elements required for non-MNOs to be able to provide retail mobile telecommunications services and are generally supplied together.143

(195) The Notifying Party considers that the relevant product market to be taken into account is the market for the wholesale supply of access and call origination services on mobile networks.

(196) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(197) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the wholesale supply of access and call origination services on mobile networks.

4.16.2. Geographic market definition

(198) In previous decisions, the Commission held that the geographic scope of the market for the wholesale supply of access and call origination services on mobile networks national due to regulatory barriers,144 including for Romania.145

(199) The Notifying Party considers that the relevant geographic market for the wholesale supply of access and call origination services on mobile networks corresponds to the territory of Romania.

(200) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(201) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant geographic market for the wholesale supply of access and call origination services on mobile networks is the territory of Romania.

4.17. Wholesale supply of international roaming services

(1) In previous decisions, the Commission found that international roaming services constitute a distinct product market.146

(2) The Notifying Party considers that the relevant product market to be taken into account is the market for wholesale supply of international roaming services.

4.17.1.1. The results of the market investigation and the Commission’s assessment

(202) The results of the market investigation did not provide reasons to depart from the Commission’s decisional practice.

(203) In light of the above, the Commission considers that, for the purpose of this Decision, the relevant product market is the market for the wholesale supply of international roaming services.

4.17.2. Geographic market definition

(204) In previous decisions, the Commission held that the relevant geographic market for the wholesale supply of international roaming is national in scope due to regulatory barriers,147 including for Romania.148