Commission, June 8, 2020, No M.9554

EUROPEAN COMMISSION

Decision

ELANCO ANIMAL HEALTH / BAYER ANIMAL HEALTH DIVISION

Subject: Case M.9554 – Elanco Animal Health/Bayer Animal Health Division Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

Dear Sir or Madam,

(1) On 14 April 2020, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (the “Merger Regulation”) by which Elanco Animal Health Inc. (“Elanco”, USA) acquires sole control of Bayer AG’s (“Bayer”, Germany) animal health business (“BAH”) (the “Transaction”).3 Elanco and BAH are designated hereinafter as the “Parties” and Elanco as the “Notifying Party” to the Transaction.

1. THE PARTIES AND THE OPERATION

(2) Elanco is a US-based animal health company that develops, manufactures and markets veterinary products for companion animals (“CA”) and production animals (“PA”) worldwide. Formerly part of the US pharmaceutical group Eli Lilly, Elanco became a fully independent company in March 2019.

(3) BAH comprises Bayer’s animal health business, which is active in the development, production and marketing of veterinary products for CA and PA worldwide. BAH represented approximately 3.5% of Bayer’s turnover in 2019.

(4) On 20 August 2019, the Parties entered into a share and asset purchase agreement pursuant to which Elanco will acquire sole control over BAH. The Transaction would therefore give rise to a concentration within the meaning of Article 3(1)(b) of the Merger Regulation.

2. UNION DIMENSION

(5) Based on 2019 data, the combined aggregate world-wide turnover of the Parties was more than EUR 2 500 million (Elanco: EUR 2 744 million; BAH: EUR 1 571 million). Each of the Parties had an EU-wide turnover of more than EUR 100 million (Elanco: […]; BAH: […]). In at least three Member States, the Parties had combined turnover of more than EUR 100 million and individual turnover of more than EUR 25 million ([…]). Neither of the Parties achieved more than two-thirds of its aggregate EU-wide turnover within one and the same Member State.

(6) The concentration therefore has a Union dimension pursuant to Article 1(3) of the Merger Regulation.

3. MARKET DEFINITION

3.1. Product market definition

3.1.1. Introduction

(7) The Transaction will combine the number four (Elanco) and five (BAH) players in the animal health industry, creating the number two supplier in the EEA and worldwide (in terms of sales) after Zoetis.

(8) As regards product market definition, in previous cases in this sector,4 the Commission has divided animal health products into three main categories: (i) biologicals (such as vaccines);5 (ii) pharmaceuticals; and (iii) feed supplements.6

(9) In the present case, the Parties’ activities mainly overlap in animal pharmaceuticals.7 Animal pharmaceuticals encompass a wide group of products that contain a variety of active substances to prevent or treat a large range of animal diseases and disorders. Within pharmaceuticals, the Commission’s past decisional practice8 distinguishes: (i) parasiticides,9 (ii) otitis products, (iii) antimicrobials, (iv) endocrine treatments, (v) anti-inflammatories, and (vi) analgesics.

(10) Furthermore, when defining relevant product markets in the area of animal pharmaceuticals, the Commission considered the following factors as important:10 (i) species (e.g. cats and dogs within CA; poultry, swine and cattle within PA), (ii) active ingredient/chemical class, (iii) targeted pathology/indication, (iv) mode of administration (“MoA”) (e.g. oral, topical, injection), (v) duration of efficacy for PA; and (vi) duration of the withdrawal period for PA.11 Not each factor was considered for each type of pharmaceuticals.

(11) In the present case, the Transaction gives rise to horizontally affected markets in the supply of pharmaceuticals for PA and CA. The Parties’ activities mainly overlap in relation to the following products: (i) CA parasiticides, antimicrobials, and otitis products and (ii) PA anticoccidials, parasiticides and antimicrobials.12

3.1.2. Companion animals

3.1.2.1. Parasiticides

(a) Commission’s precedents

(12) In its previous decisional practice, the Commission considered that feline and canine parasiticides belong to a single market for CA parasiticides.13

(13) Within parasiticides, the Commission found that products targeting multi-celled parasites (e.g. fleas and worms) and products targeting single-celled parasites (“anticoccidials”) constitute distinct product markets.14 As regards multi-celled parasiticides, the Commission distinguished three categories.15 (i) ectoparasiticides (or ecto products), used to control external parasites (e.g. fleas, ticks), (ii) endoparasiticides (or endo products), used to control internal parasites (e.g. flukes, tapeworms, roundworms), and (iii) endectocides (or endecto products), used to control both external and internal parasites. Given the existence of a certain degree of substitutability, the Commission also envisaged alternative market segments comprising (i) ecto/endecto products together and (ii) endo/endecto products together, but ultimately left the market definition open.16

(14) The Commission also envisaged additional sub-segmentations of the CA parasiticides markets including (i) a segmentation by mode of administration (e.g. oral, injectable, topical), which was ultimately left open;17 and (ii) a segmentation based on the indication/targeted parasites, considering that heartworm products constitute a separate market.18 In contrast, previous decisions did not envisage a segmentation of parasiticides by active ingredient/chemical class (such as isoxazolines (“isox”)) or by duration of efficacy.19

(b) The Parties’ views

(15) The Parties do not contest the fact that products targeting multi-celled parasites and anticoccidials are part of distinct product markets. They also agree with the distinction between (i) ectoparasiticides, (ii) endoparasiticides, and (iii) endectocides. However, they consider that market segments comprising (i) ecto/endecto products and (ii) endo/endecto products are not plausible. The Parties also submit that CA parasiticides are usually authorised for use specifically in either cats or dogs, and cannot be used interchangeably. Conversely, they do not consider meaningful to further segment the markets for parasiticides by mode of administration, indication or chemical class. In particular, they contest the existence of a distinct market segment for isox products on the ground that (i) the chemical class of parasiticides does not drive customer choices and that (ii) products may combine various compounds in order to extract the benefit of multiple different chemical classes. The Parties claim that the differences in terms of mode of administration, indication and chemical class are relevant when assessing closeness of competition rather than identifying separate product markets. The Parties also argue that, within these hypothetical sub-segments, the overlaps between their activities are limited.20

(c) The Commission's assessment

Segmentation between ecto, endo and endecto products

(16) Nothing in the market investigation suggested that the Commission should depart in the present case from its previous practice concerning the distinction between endo, ecto and endecto products.

(17) As regards the alternative market segments, which were envisaged in previous decisions, comprising (i) CA ecto/endecto products and (ii) CA endo/endecto products, the market investigation yielded mixed results.

(18) On the one hand, several market participants consider that endo and ecto products are not interchangeable with endecto products as they are generally used for different indications or situations. For instance, a competitor indicated that, in situations where veterinarians have to “address a specific issue related either to gastroinstestinal worms (EndoP) or fleas and flies (EctoP) […], EndectoP are not relevant from both a medical and customer point of view.” Another player stated that “endecto products are typically used for prevention (e.g., for prevention of heartworm, lungworm, or flea and tick)”, while “Endo products […] are typically used for the treatment of [gastrointestinal] parasites”. Similarly, a customer submitted that “for serious infections, exclusively endo should be used”.21

(19) On the other hand, a number of respondents confirmed the existence of a certain degree of substitutability indicating that endecto products may be used interchangeably with ecto or endo products in some situations. For example, a customer stressed that endo and endecto products are interchangeable “for minor infections” and a competitor submitted that “ENDECTOS products can replace ENDOS products as they cover the endoparasiticide spectrum”. Market participants also explained that “in practice, this depends very much on the customer and prescribing vet’s preferences, as well as the individual products at issue”. Some competitors also emphasised the fact that endecto sales have a “direct impact” on the revenues and trends of endo and ecto products.22

(20) In view of the above, for the purpose of this Decision, the Commission concludes that (i) endo, ecto and endecto products constitute distinct product markets and that (ii) the question of whether there exist alternative product markets comprising endo / endecto products and ecto / endecto products can be left open as it does not affect the Commission’s conclusions regarding the compatibility of the Transaction with the internal market.

Segmentation by species

(21) The results of the market investigation largely confirmed the Parties’ claim that CA parasiticides are usually authorised for use specifically in either cats or dogs, and cannot be used interchangeably. In particular, market participants stressed the facts that (i) CA parasiticides indicated for both cats and dogs are “very rare”, that (ii) drugs are “developed, tested and approved for [a particular pet] and should not be used on a different animal (and vets would not do so)” and that (iii) “giving a dog product to a cat is dangerous and can kill the cat”. Some competitors also explained that, albeit parasiticides for cats and dogs can be marketed under the same brand and based on the same active ingredient, the dosage and the mode of administration is likely to vary from one species to another. For instance, “dogs get a much higher dose of active depending on their weight” and oral parasiticides are more commonly used on dogs than on cats (as it is difficult to administer pills to cats).23

(22) In view of the above, for the purpose of this Decision, the Commission concludes that parasiticides for cats and dogs are likely to constitute distinct product markets. Segmentation by mode of administration

(23) The market investigation was inconclusive on the question of whether the CA parasiticides markets should be further segmented by mode of administration. Although a majority of market participants indicate that CA parasiticides with different modes of administration can be used interchangeably, a significant number of customers disagree.24 Moreover, both customers and competitors consider that the mode of administration is an important parameter of competition in the markets for CA parasiticides.25 This is notably illustrated by the fact that, in some CA parasiticides markets (in particular canine parasiticides), the demand tends to switch to oral products due to their ease of administration.

(24) In any event, for the purpose of this Decision, the segmentation of the markets for CA parasiticides by mode of administration can be left open as it does not affect the Commission’s conclusions regarding the compatibility of the Transaction with the internal market.

Segmentation by indication (heartworm)

(25) The results of the market investigation revealed that market participants have a clear preference for products with a broad spectrum of claims as it is more convenient (i.e. customers favour products that can be used to treat or prevent several parasites rather than using several different products).26 […].27 That being said, the market investigation also confirmed that products for the treatment and prevention of heartworms are likely to constitute a distinct product market. Heartworm is an endoparasitic worm residing in the heart of the host animal, which can be fatal and difficult to treat once contracted. In the EEA, heartworm is endemic only in southern Europe. Given these specific features, market participants consider that heartworm “is a very specific claim and also a unique product”.28 The results of the market investigation did not suggest the existence of distinct market segments for other indications.29

(26) In view of the above, and in line with its previous practice, the Commission concludes that, for the purpose of this Decision, products for the treatment and prevention of heartworm constitute a distinct product market. Segmentation by chemical class

(27) Subject to isox (see below), the results of the market investigation generally suggest that a segmentation of the markets for CA parasiticides by chemical class is not relevant. All competitors and half of the customers consider that parasiticides for CA with different chemical classes can be used interchangeably.

(28) More specifically, a large number of respondents indicated that products based on isox,30 i.e. the newest chemical class of ectoparasiticides (which is also used as endecto products in combination with endo chemical classes), are interchangeable with other parasiticides.31

(29) However, the Commission also found that isox products are subject to different competitive dynamics, with different pricing (isox products are significantly more expensive) and competitive landscape (only a limited number of players have isoxbased products). In recent years, isox products have rapidly increased sales at the expense of older ecto/endecto products and market participants expect the demand for isox products to increase further in the coming years. Some respondents consider that isox products are “changing the dynamic” in CA parasiticides.32 The success of isox products is linked to the facts that (i) they are effective against a wide range of ectoparasites (including fleas and ticks), (ii) they can be administered orally, (iii) they have a long duration of efficacy (between one and three months) and (iv) they act systematically, protecting all parts of the animals’ body. By comparison, older ecto chemical classes are either topical or injectable products, only effective against a sub-set of ectoparasites (or have encountered resistance issues with fleas or ticks) or do not produce systemic effects for one month or longer. For these reasons and also given that isox products are prescription-only (whereas older ecto chemical classes are often also available in the other-than-vet (“OTV”) distribution channel (including over-the-counter (“OTC”) and online distribution channels), isox products are increasingly endorsed by vets.33

(30) In any event, for the purpose of this Decision, the exact delineation of the product market can be left open since the Transaction gives rise to serious doubts as to its compatibility with the internal market regardless of whether isox-based parasiticides for CA constitute a distinct market segment or are part of broader markets for CA ecto and endecto.

Segmentation by duration of efficacy

(31) As previously indicated, the past decisional practice did not consider a segmentation of the CA parasiticides markets by duration of efficacy. Nothing in the market investigation suggested that the Commission should depart in the present case from its previous practice.

(d) Conclusion

(32) Based on the results of the market investigation, for the purposes of this Decision, the Commission concludes that (i) endo, ecto and endecto products for CA; (ii) parasiticides for cats and for dogs; and (iii) products for the treatment and prevention of heartworm constitute distinct product markets/market segments.

(33) For the purposes of this Decision, the Commission also considers that it can be left open (i) whether there exist alternative product markets comprising endo / endecto products and ecto / endecto products for CA; (ii) whether the markets for CA parasiticides should be further segmented by mode of administration; and (iii) whether isox-based parasiticides for CA constitute a distinct market segment or are part of broader markets for CA ecto and endecto, as these alternative market delineations do not affect the Commission’s conclusions regarding the compatibility of the Transaction with the internal market.

3.1.2.2. Antimicrobials

(34) Antimicrobials (also known as antibiotics) are pharmaceutical products that destroy or prevent the growth of microbes such as bacteria, mycoplasma or fungi and treat diseases associated with them. Antimicrobials can be administered in various ways, notably by injection and orally (including as a tablet; a soluble powder, concentrate or solution that is added to drinking water; and as a pre-mix). Antimicrobial products can be used to treat multiple species. There are a number of chemical classes used in antimicrobials.

(a) Commission’s precedents

(35) In previous decisions, the Commission considered possible segmentations based on the following factors: (i) the species, (ii) the active ingredient/chemical class (including sulphonamides, penicillins, cephalosporins, phenicols, fluoroquinolones and tetracyclines), and (iii) the mode of administration (oral vs. injectable).34 The exact delineation of the market was ultimately left open.35

(b) The Parties’ views

(36) The Parties agree with the Commission’s previous position that there is a limited demand-side substitutability between antimicrobials based on different chemical classes. For instance, different chemical classes have received different categorisations from the European Medicines Agency (“EMA”) regarding their impact on disease resistance in humans,36 and those defined as higher risk are not recommended for use except as a last resort. Lower risk classes include macrolides (which form the base of the majority of Elanco’s antimicrobials), alongside pleuromutilins, various types of penicillins, cephalosporins, aminoglycosides, lincosamides and tetracyclines. Higher risk classes include, in particular, fluoroquinolones (which is the basis of BAH’s core Baytril product, which makes up the […] majority of BAH’s sales in Group 1 affected markets37). Moreover, different chemical classes have different properties, meaning that they may typically be used at different stages of a given treatment.

(37) As regards methods of administration, the Parties agree with the Commission’s past assessment that there is limited demand-side substitutability between different methods of administration.

(38) As regards a potential segmentation by species, the Parties argue that many antimicrobials can be administered to a range of species and that distinguishing between different species for the purposes of market definition is not appropriate from both a supply- and demand-side perspective.

(c) The Commission’s assessment

(39) As regards a segmentation by mode of administration (i.e. oral and injectable), the results of the market investigation were mixed. From the demand side, a large majority of customers do not consider antimicrobials with different modes of administration to be interchangeable and some respondents specified that the choice may depend on the circumstances of the individual animal.38 On the other side, the majority of suppliers consider them to be interchangeable, specifying that often a vet will administer the same antimicrobial by injection and the pet owner will follow the treatment at home with an oral version.39

(40) As regards a segmentation by species (i.e. cats and dogs), the results of the market investigation were mixed. From the demand side, the large majority of customers do not consider antimicrobials for different species to be interchangeable, but some respondents specified that most products are indicated for use in both cats and dogs.40 Most suppliers consider that customers use antimicrobials for different species interchangeably to treat the same disease, confirming that many antimicrobials are authorised for use in both cats and dogs.41

(41) Also as regards segmentation by chemical class (the relevant classes for the Parties’ CA antimicrobials being fluoroquinolones, penicillin and sulphonamides), the results of the market investigation were mixed. From the demand side, a large majority of customers do not consider antimicrobials with different chemical classes to be interchangeable, and some respondents further specified that it is linked to the target bacteria.42 However, most suppliers consider that antimicrobials with different chemical classes are interchangeable, while vets tend to have first and second line preferences to treat certain infections.43 One supplier mentioned that “The choice of active ingredient will usually vary depending on the pathogen/bacteria causing the disease. A disease can be caused by a pathogen and several antibiotics can be acceptable for use.”

(d) Conclusion

(42) In the present case, the question of the segmentation of the market by mode of administration, species or chemical class can be left open as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

3.1.2.3. Otitis products

(a) Commission’s precedents

(43) Otitis externa is an inflammation of the external ear canal. Sometimes, otitis may progress further into the ear (otitis media). Otitis is not a disease in itself but rather a symptom of other diseases, such as an infection. It is common in dogs but less frequent in cats.

(44) According to the Commission’s past decisional practice, otitis pharmaceuticals are considered as a separate market. Previously, the Commission has left open the exact delineation of the relevant market for otitis products as to whether further segmentation based on the mode of administration was warranted, indicating however that the otitis externa market is mainly a topical market and that oral and injectable products are rarely used.44

(b) The Parties’ views

(45) The Parties agree with the Commission’s precedents in that otitis products constitute a separate market and submits that there exist significant differences between (i) a new generation of long-acting otitis products that are applied only once or twice by the veterinarians (“long-acting otitis products”) and (ii) older daily-use otitis products that need to be applied daily for one to three weeks by pet owners (“dailyuse otitis products”). The Parties point to the important difference in price between both products. RBB Economics’ analysis of third party data sources indicates that, for example, in the UK, Osurnia (long-acting product) was approximately […] more expensive than Canaural (daily-use product) in 2019.

(c) The Commission’s assessment

(46) The market investigation confirmed that in line with precedents and the Parties’ views, otitis products constitute a separate product market.45 The market investigation also confirmed the views of the Parties that very significant differences exist based on the duration of efficacy of the products, between long-acting and daily-use otitis products.

(47) Long-acting otitis products currently include in the EEA only the Parties’ products: Elanco’s Osurnia and BAH’s recently launched Neptra. These products are administered by a veterinarian and only require a single (in the case of Neptra) or a dual (in the case of Osurnia) application. Both products are effective against Grampositive bacteria and fungal infections. Long-acting products are significantly more expensive than daily dose products.

(48) Daily-use otitis products cover most of the topical otitis products in the market, including Elanco’s Surolan, Dechra’s Canaural, Vetoquinol’s Aurizon and Oridermyl, Ecuphar’s Conofite Forte, Virbac’s Easotic and Merck’s Posatex. These products normally require daily ear drop administration by pet owners for one to three weeks. Most of these products are effective against both Gram-positive and Gram-negative bacteria, as well as fungal infections.

(49) As long-acting products, Osurnia and Neptra only need to be applied once or twice and are administered by a vet. They eliminate or greatly reduce the risk of noncompliance (i.e. non-adherence to the treatment regimen due to difficulties to apply the products to the animal by pet owners without any training). A significant share of customers are ready to pay a significant premium for a convenient solution which eliminates the need for them to apply the product and the risk of ineffective treatment. In contrast, daily dose products are seen as a cheap option, and will be used in cases where compliance is not a primary concern or for pet owners which prefer a more economical alternative.

(50) In this respect, half of the suppliers consider that long-acting and daily-use otitis product are not interchangeable, while the other half indicate they are interchangeable for customers.46 However, it seems that suppliers that answered that long-acting and daily-use product are interchangeable refer only to substitutability from a medical point of view. For example, one of the suppliers who deemed these products substitutable explains that “from a medical point of view they are interchangeable. The main benefit of long duration products is perceived by pet owners who no longer apply any product at home as it has been administered at the veterinary clinic”.47 Other suppliers considering the products interchangeable, explain that ease of administration and price are key factors for customers and vets to decide on a specific product, as well as the ability of the owner to administer the product.48 Some suppliers consider that even if they believe long-acting and daily-use products are interchangeable, “long acting treatments are more and more used as first line otitis treatment in dogs.”49

(51) Another supplier explains that “compliance with the treatment regime is critical to success. In cases where the vet is concerned about an owners ability to administer the treatment on a daily basis they will opt for a long term treatment option […] The choice would therefore be predominantly based upon […] the ability of the owner to apply the ear suspension for several consecutive days. Both Neptra (Bayer) and Osurnia (Elanco) are applied by the veterinary surgeon in the clinic rather than by the pet owner at home which is ensuring full compliance of treatment and therefore peace of mind for the vets as when a treatment does not work we can never be sure if the diagnostic was not good, if the treatment protocol was not respected by the petowner at home (not easy to put a liquid in the ear of a dog) or if the product failed. For this reason, vets tend to prescribe these long acting products at the place of the short acting ones”.50

(52) Moreover, the vast majority of customers considers that long-acting and daily-use otitis products cannot be used interchangeably.51 For example, one customer explains that “the advantage of long duration products is highly appreciated by customers and veterinarians”.52

(53) In fact, competitors indicated clearly that the most important parameters to choose an otitis product are duration of efficacy and frequency of administration while price, chemical class or reputation of suppliers would be less relevant.53 Customers also identify duration of efficacy and frequency of administration as the most important parameters to select an otitis product, followed by price, while chemical class or reputation of the supplier would be less relevant.54 Long-acting and daily-use products’ main differences are precisely duration of effect and frequency of administration.

(54) Based on the significant differences in terms of price, duration of effect, frequency of administration and customers’ preferences and taking into consideration the results of the market investigation, the Commission considers that long-acting and daily-use products belong to separate product markets.

(55) With regards to mode of administration, the Commission notes that most otitis products are topical and the market investigation did not provide any element suggesting that a segmentation by mode of administration would be meaningful. Moreover, this differentiation would be only relevant for daily-use products. Should the market be segmented by mode of administration, there would be no overlap between the daily-use products of the Parties. Therefore, this distinction will not be further considered in this Decision.

(56) With regards to a distinction by species, it would not be relevant for long-acting products, as long-acting products are only indicated for dogs. With regards to daily-use otitis products, the question as to whether a segmentation by species is needed can be left open as the Transaction does not raise concerns with regards to daily-use otitis products irrespective of the exact product market definition retained.

(d) Conclusion

(57) The Commission concludes, in light of the above, that, for the purposes of this case, long-acting and daily-use otitis products constitute distinct product markets. The precise market definition can be left open as to whether daily-use products for different species (cats and dogs) or via different modes of administration constitute a separate market or form part of a wider daily-use otitis products market, as the Transaction does not raise serious doubts as to its compatibility with the internal market for daily-use otitis products irrespective of whether the relevant product market is defined as comprising all species and all modes of administration or not.

3.1.3. Production animals

3.1.3.1. Parasiticides

(a) Commission’s precedents

(58) The Commission’s decisional practice referred to in Section 3.1.2.1(a) above concerning parasiticides for CA is to a large extent also relevant for PA. In particular, in Eli Lilly/Novartis Animal Health, the Commission adopted for PA the same approach as for CA, (i) distinguishing ecto, endo and endecto products and (ii) envisaging alternative market segments comprising ecto/endecto products and endo/endecto products. In that decision, the Commission also envisaged to subsegment the PA parasiticides markets (i) by species, (ii) by mode of administration, and (iii) by indication, but ultimately left open the exact delineation of the market.55 In contrast, previous decisions did not envisage a segmentation of PA parasiticides by chemical class, period of efficacy or period of withdrawal.

(b) The Parties’ views

(59) The Parties did not provide any specific views regarding the product market definition for PA parasiticides and referred to the approach taken for CA.56

(c) The Commission’s assessment

Segmentation between ecto, endo and endecto products

(60) Nothing in the market investigation suggested that the Commission should depart in the present case from its previous practice concerning the split between endo, ecto and endecto products. As regards the alternative market segments comprising (i) PA ecto/endecto products and (ii) PA endo/endecto products, the market investigation was inconclusive, with respondents providing mixed responses. For instance, a competitor submitted that these products cannot be used interchangeably as “it depends on the type of prevention program and breeding conditions of the target animal group”, while another player indicated that “most customers use endecto for comfort and consider specific products when necessary”, suggesting the existence of a certain degree of demand-side substitutability.57 In any event, for the purpose of this Decision, the Commission considers that the exact scope of the product market can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition.

Segmentation by species

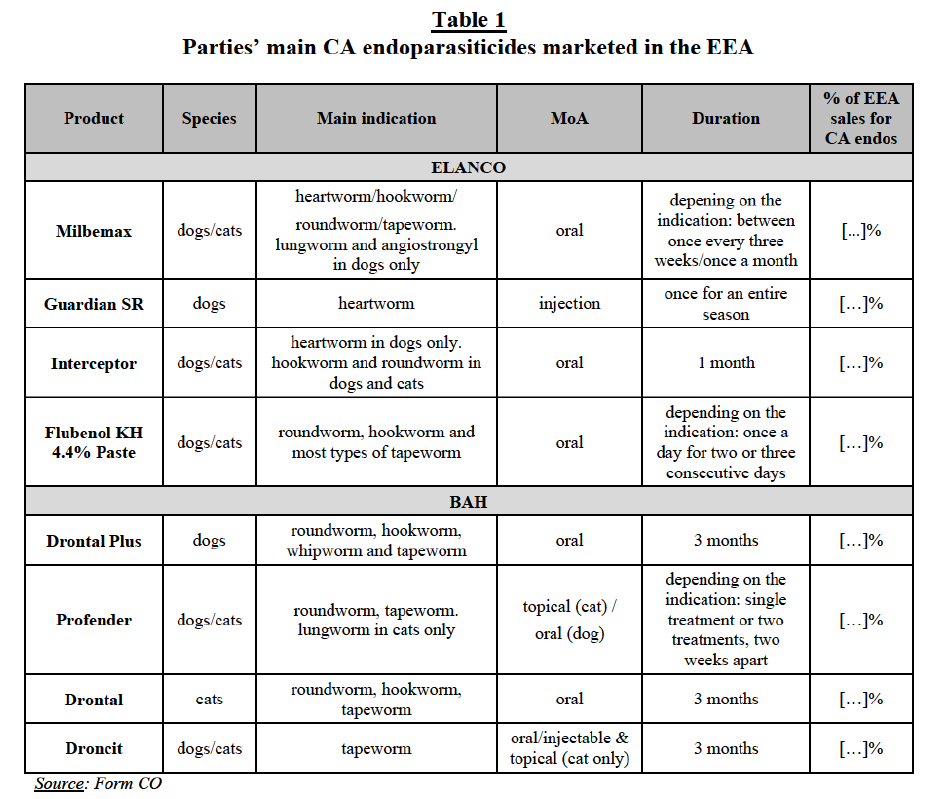

(61) The results of the market investigation largely confirmed that PA parasiticides for different species (e.g. swine, cattle, etc.) cannot be used interchangeably. For example, a competitor explained that “many products are only indicated for a particular species or group of species. This limitation of use is largely driven by: (i) the size of the animal which may justify a different strength/dosage; and (ii) the animal’s intended use (e.g. human consumption).”58 In view of the above, and similarly to CA, the Commission consider that, for the purpose of this Decision, the markets for PA parasiticides should be segmented by species.

Segmentation by mode of administration

(62) The results of the market investigation suggest some demand-side substitutability between PA parasiticides with different modes of administration. However, some customers also stressed the fact that depending on the situations products with different modes of administration may not be used interchangeably (e.g. “it depends whether I have to do mass treatments, if I have to treat only a few animals, it depends on age and how the animals are housed”).59 In any event, for the purpose of this Decision, the segmentation of the markets for PA parasiticides by mode of administration can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition.

Segmentation by indication

(63) The results of the market investigation were inconclusive as to whether the markets for PA parasiticides should be further segmented by indication. In any event, for the purpose of this Decision, the exact relevant product market definition can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition.

Segmentation by chemical class

(64) The market investigation revealed that PA parasiticides with different chemical classes can be used interchangeably and that the chemical class is not a key parameter of competition. For instance, a competitor stated: “efficacy and price are the main drivers, the chemical class is not that relevant”.60 In any event, for the purpose of this Decision, the exact relevant product market definition can be left open since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition.

Segmentation by duration of efficacy or withdrawal period

(65) The past decisional practice did not consider a segmentation of the PA parasiticides markets by period of efficacy or by period of withdrawal. Nothing in the market investigation suggested that the Commission should depart in the present case from its previous practice.

(d) Conclusion

(66) Based on the results of the market investigation, for the purposes of this Decision, the Commission concludes that endo, ecto and endecto products for PA constitute distinct product markets/market segments and that the markets for PA parasiticides should be segmented by species.

(67) For the purposes of this Decision, the Commission also considers that it can be left open (i) whether there exist alternative product markets comprising PA endo / endecto products and PA ecto / endecto products; (ii) whether the markets for PA parasiticides should be further segmented by mode of administration, indication or chemical class, since the Transaction does not give rise to serious doubts as to its compatibility with the internal market under any plausible product market definition.

3.1.3.2. Antimicrobials

(a) Commission’s precedents

(68) The Commission’s decisional practice and the approach outlined in Section 3.1.2.2 (a) above concerning antimicrobials for CA are also applicable to PA. As regards the mode of administration for PA antimicrobials, the Commission previously also considered a possible further sub-segmentation of oral PA antimicrobials into premixes and solubles, but ultimately left the question open.61 In previous cases, the Commission has also considered that mastitis treatments for cattle can be distinguished from other forms of antimicrobial treatment on the basis of their singular mode of administration, namely intra-mammary injections.62 As the Parties’ activities do not overlap in mastitis treatments, this segment will not be considered in the rest of this Decision.

(b) The Parties’ views

(69) The Parties submit the same views for PA antimicrobials as for CA antimicrobials described in Section 3.1.2.2(b). In respect of defining markets for antimicrobials by reference to chemical class or mode of administration, the Parties agree with the Commission’s previous paractice that there can be limited demand-side substitutability between antimicrobials that make use of different chemical classes or modes of administration. Moreover, within oral antimicrobials, the Parties consider that there is a meaningful difference from a customer perspective between pre-mixes and other products like water solubles. As regards a potential segmentation by reference to species, the Parties do not consider this appropriate from both supplyand demand-side substitutability.

(c) The Commission’s assessment

(70) As regards a segmentation by mode of administration (i.e. oral vs. injectable), the results of the market investigation were not conclusive. From the demand side, most customers do not consider antimicrobials with different modes of administration to be interchangeable, with some respondents specifying “except in certain cases.”63 The majority of suppliers do consider them to be interchangeable, however specifying that it depends on the target indication.64

(71) As regards a segmentation by species, the results of the market investigation confirmed that this is not appropriate. The large majority of customers65 and suppliers responded that most antimicrobials are indicated for multiple species.66

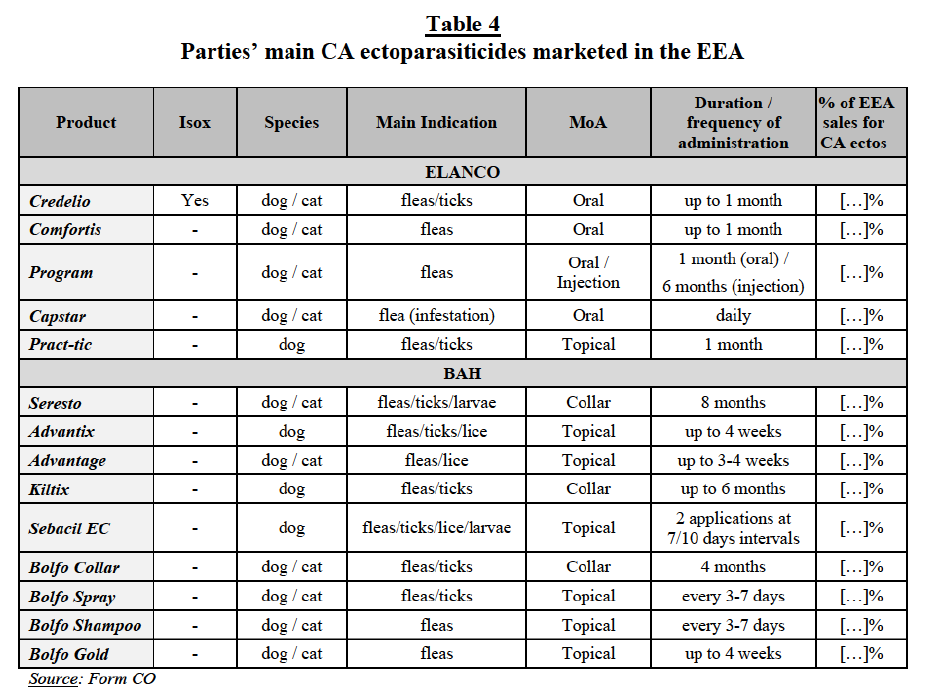

(72) As regards a segmentation by chemical class, the results of the market investigation were mixed. From the demand side, the majority of customers do not consider antimicrobials with different chemical classes to be interchangeable,67 while the large majority of suppliers responded that antimicrobials with different chemical classes are considered interchangeable, specifying that it depends on the target bacteria.68

(d) Conclusion

(73) Based on the results of the market investigation, for the purposes of this Decision the Commission does not consider further segmentation of the PA antimicrobials market by species. The question of segmentation of the market by mode of administration or chemical class can be left open in the present case as the Transaction does not raise serious doubts as to its compatibility with the internal market under any plausible market definition.

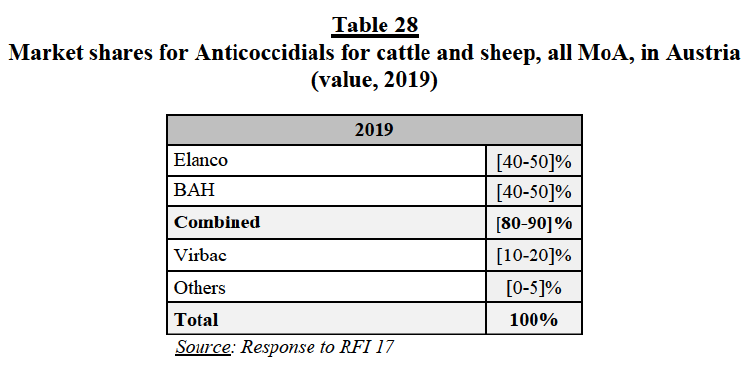

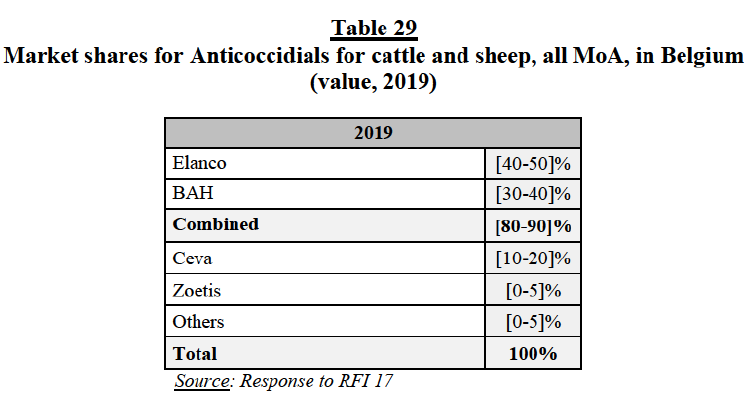

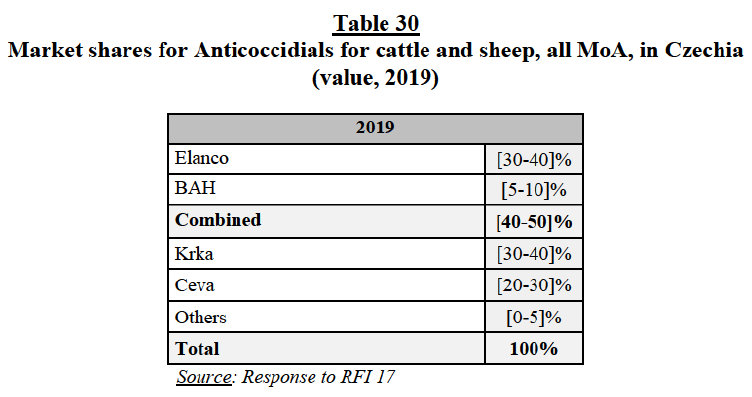

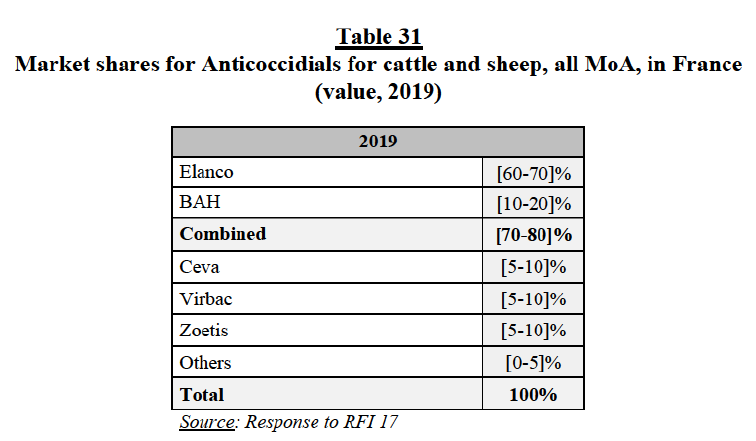

3.1.3.3. Anticoccidials

(a) Commission’s precedents

(74) Anticoccidials act against single-celled parasites known as coccidia. Various types of drug are used for coccidiosis prevention and control: (i) prophylactic anticoccidials approved on an EEA-wide scale as preventative feed-in anticoccidials to be administered routinely, in particular for poultry (including turkey); (ii) pharmaceutical coccidiostats authorised as veterinary medicinal products available throughout the EEA for prevention, treatment or aid in the control of coccidiosis (dependent on the pharmacokinetic characteristics of their active substances); and (iii) coccidiosis vaccines: used as a preventative preparation, to induce active immunity against coccidiosis, in particular for poultry.

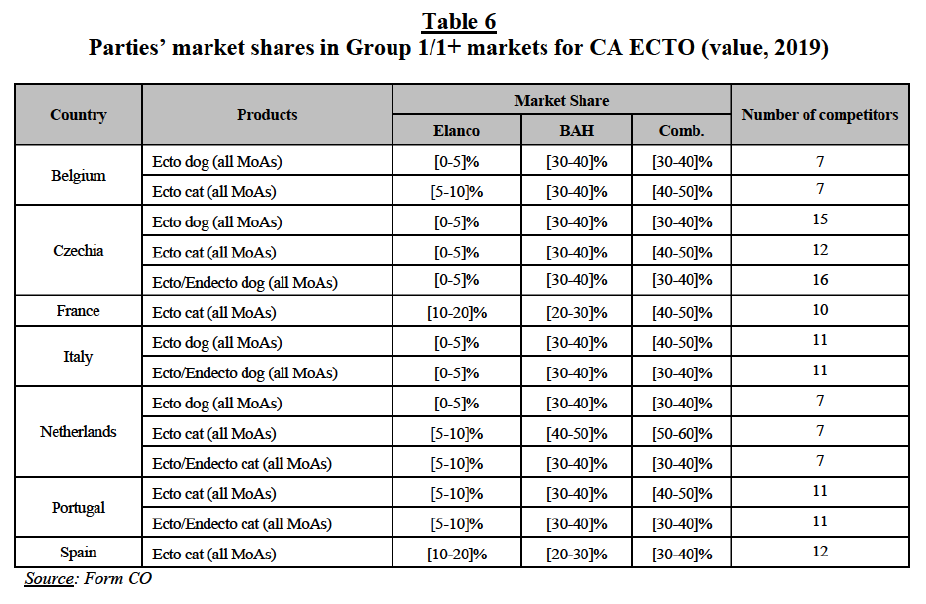

(75) The Commission has considered PA anticoccidials in previous cases.69 In these cases, the Commission has defined a separate market for poultry anticoccidials compared to anticoccidials for other species. Within poultry anticoccidials, the Commission further defined the following categories: (i) prophylactic anticoccidials, (combining categories (i) and (iii) above in paragraph 74) with a possible market segmentation between vaccines and feed additives, and (ii) pharmaceutical coccidiostats, corresponding to category (ii) above in paragraph 74.70 The subsegmentation of prophylactic anticoccidials between vaccines and feed additives was ultimately left open.

(76) As regards other species (cattle, sheep and swine), the Commission has not previously assessed these products and therefore has not considered any potential segmentation.

(b) The Parties’ views

(77) As regards poultry, the Parties support the above segmentation distinguishing between pharmaceutical coccidiostats and prophylactic anticoccidials, potentially with separate sub-markets within the latter for vaccines and feed additives.

(78) As regards other species, the Parties submit that only pharmaceutical coccidiostats are available on the market and, that for each of cattle, sheep and swine, there is a single market for species-specific pharmaceutical coccidiostats.

(79) The Parties submit that there is no basis for further segmentation by mode of administration or indication, as the relevant anticoccidials are all administered orally, and all products indicated for each of cattle, sheep and swine target all of the coccidiosis-causing species relevant for the respective species.

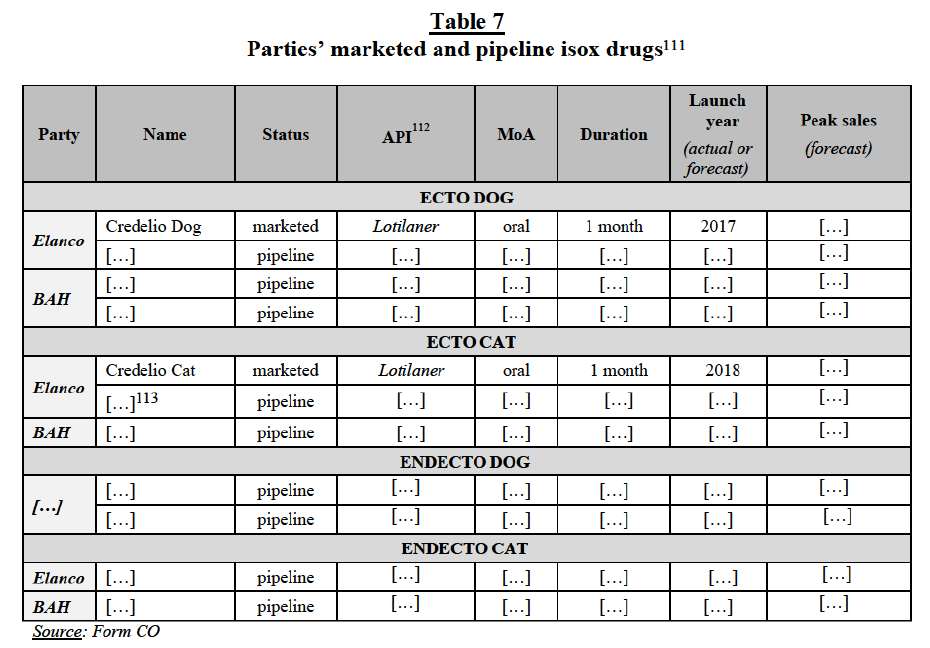

(c) The Commission’s assessment

(80) As regards the separation of anticoccidials for poultry from other species, and the segmentation of poultry anticoccidials into prophylactic anticoccidials and pharmaceutical coccidiostats, the market investigation did not provide any element to depart from the previous decisional practice and the Parties’ views.71 On this basis, no overlap among the Parties’ activities would arise and therefore poultry products will not be considered further in this Decision.

(81) As regards segmentation by single species for non-poultry species, the market investigation did not confirm the Parties’ views that this is appropriate. The majority of responding competitors and customers confirm that PA pharmaceutical coccidiostats are indicated for multiple species and not single species. Respondents highlighted that there are products indicated for ruminants (i.e. both cattle and sheep) suggesting this possible grouping of species within the non-poultry species72.

(82) As only pharmaceutical coccidiostats are available for non-poultry species, further segmentation between prophylactic anticoccidials and pharmaceutical coccidiostats for these species was not considered meaningful and as such was not investigated further.

(83) The Commission does not consider any further segmentation by mode of administration or indication to be meaningful as the relevant anticoccidials are all administered orally, and all products indicated for each of cattle, sheep and swine target all of the coccidiosis-causing species relevant for the respective species. Furthermore, the market investigation results did not indicate that any segmentations by chemical class, period of efficacy or period of withdrawal are relevant and they are not considered for the purpose of this case.

(d) Conclusion

(84) In the present case, the question of segmentation of the non-poultry PA anticoccidial market by (groups of) species (i.e. considering ruminants and swine separately or together) can be left open as the Transaction raises serious doubts as to its compatibility with the internal market under any plausible market definition.

3.2. Geographic market definition

(a) Commission’s precedents and the Parties’ view

(85) The Commission has consistently defined the geographic markets for marketed animal pharmaceuticals as being national in scope.73 With respect to pipeline pharmaceuticals, the Commission has consistently held that the geographic scope of the market is either global or EEA-wide.74

(86) The Parties agree with the above approach but submits, with respect to marketed products, that there is a growing trend towards competition across borders in the EEA (due to the increasing harmonisation of the regulation at European level and the fact that many animal health players are active in multiple EEA countries), which should be taken into account in the competitive assessment.75

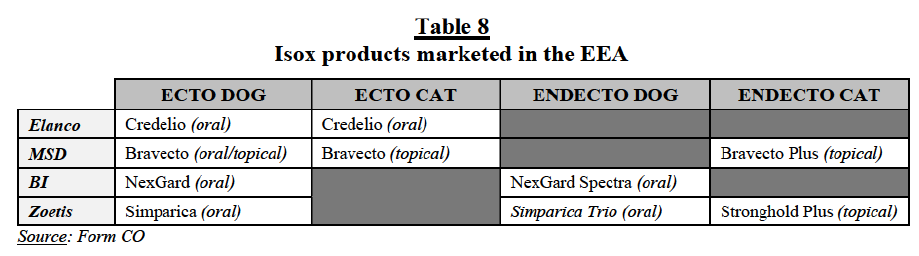

(b) Commission’s assessment and conclusion

(87) As regards marketed products, the results of the market investigation confirmed that the geographic market for animal pharmaceuticals should be defined at national level. However, the market investigation also supports, at least to some extent, the growing supranational dimension of competition put forward by the Parties. For example, although most competitors fix prices and organise their sales and marketing teams at national level, this is also done by some players at regional or EEA level.76 Similarly, although customers typically source animal pharmaceuticals at national level, some of them organise their procurement at regional or EEA level.77 Therefore, for the purpose of this Decision, the Commission considers that the geographic market for marketed animal pharmaceuticals is national in scope, and it will consider the growing supranational dimension of competition in its competitive assessment.

(88) As regards pipeline products, nothing in the market investigation suggests that the Commission should depart in the present case from its previous decisional practice concerning the geographic market definition. In fact, companies which invest significant resources in R&D to develop new products expect to sell those products in as many countries as possible. It is not possible to allocate pipeline products to specific countries. Therefore, pipeline products should be considered at EEA or global level.

4. COMPETITIVE ASSESSMENT

4.1. Methodology for the identification and the assessment of affected markets

(89) In line with Commission precedents in pharmaceutical mergers with a large number of affected markets (involving numerous product and geographic markets), the Commission has applied a system of filters aimed at determining the group of markets where concerns are most likely and on which it focuses its analysis. In line with Commission precedents in the pharmaceutical sector,78 affected markets can be classified in four categories: Group 1, where the Parties' combined market share exceeds 35% and the increment exceeds 1%; Group 1+, where either (i) the combined market share is below 35% (but above 20%), and only one other competitor remains on the market, or where (ii) the combined market share exceeds 35% and the increment is below 1%, but the party with the small increment is a recent entrant;79 Group 2, where the Parties' combined market share exceeds 35% but the increment is below 1%; and Group 3, where the Parties' combined market share is between 20% and 35%, and Group 1+ conditions are not met.

(90) The Commission has analysed all markets affected by the Transaction under all plausible market definitions.

(91) In line with precedents,80 Group 3 markets are not discussed individually in this Decision.81 The Commission assessed the competitive situation in these markets by considering the combined market shares of the Parties and their competitors over the last three years, other factors including the presence of competitors with a significant presence, the date of patent expiry and competition from generics, the Parties’ pipeline products, as well as the results of the market investigation. The Commission reached the conclusion that the Transaction does not raise serious doubts as to its compatibility with the internal market in relation to the possible Group 3 markets arising from the Transaction, due to the limited market shares of the Parties and the presence of significant competitors remaining on the market post-Transaction that will likely sufficiently constrain the merged entity.

(92) Similarly, in line with precedents,82 Group 2 markets are not discussed individually in this Decision. Generally, the Parties have combined market shares below 50%83 with a de minimis increment below 1%. In some markets, combined market shares are above 50%,84 with a de minimis increment below 1%. Post-Transaction, the Parties will face at least three competitors with market shares equal or above the increment (including meaningful players with market share above 5%) in all these markets. Moreover, the market investigation did not reveal any concerns in these markets. In light of the above, the Commission considers that the Transaction is unlikely to remove any significant competitive constraint on the Group 2 markets and, thus, will not lead to any competition concerns on these markets.

(93) In the following, the Commission individually assesses all Group 1 and 1+ markets.

4.2. Companion animals

4.2.1. Parasiticides

4.2.1.1. Endoparasiticides85

(a) Overview of the market and the Parties’ products

(94) As explained in Section 3 above, endoparasiticides are used to control internal parasites, such as flukes, tapeworms and roundworms. Each type of endo-product has a different mode of administration and works on endoparasiticides more or less effectively. The Parties estimate that, in 2018, the total size of the endoparasiticides segment in the EEA was […].86 The Parties explained that the demand for CA endoparasiticides is growing and expected to further grow in the next years due to increasing pet adoption and expenditure on veterinary healthcare.

(95) Endoparasiticides for CA can be administered (i) topically, with a typical frequency of application/duration of a month or once every three months; (ii) by injection, with a typical frequency of application/duration of one time per year; (iii) orally (including both preventive and treatment endoparasiticides; in the former case, they can be administered monthly or quarterly, while in the latter case, they should be administered daily, for a certain number of days).

(96) There are a number of chemical classes used in endo products. The core chemical classes used in currently marketed endo products are: avermectins, benzimidazoles and isoquinoles. Avermectins are a class of endos used also as endectos. This class is effective against intestinal worms, heartworms and lungworms, as well as ectoparasites. Benzimidazoles are a class of endos with a broad spectrum of action and a high safety profile; they are effective against roundworms (such as hookworms and whipworms) and some tapeworms. Isoquinolines include praziquantel and

players (i.e. BI, Merck and Zoetis), which have a significant presence in most EEA national markets, and (ii) several smaller competitors (such as Ceva and Virbac), with market shares comparable to Elanco’s in certain national markets. Second, the Parties claim that their products face fierce competition from generics (several of the Parties’ products being off-patent, including Elanco’s Milbemax, as well as most of BAH’s Drontal family of products). Third, the Parties argue that their products do not closely compete with each other as they are differentiated (i) in terms of spectrum of indications. Elanco’s Milbemax can be used against a wider range of worms, while BAH’s Drontal, Drontal Plus and Profender are not effective against either heartworm or lungworm. In addition, Droncit can only be used in cases of tapeworm and is not effective against other gastro-intestinal worms; and (ii) in terms of distribution channels, Elanco focusing on veterinaries, whereas BAH increasingly distributes its products through the OTV channel. Finally, the Parties argue that barriers to entry from neighbouring geographic markets in which certain CA endoparasiticides are already sold are relatively low.

(102) In any event, the Parties have agreed to divest BAH’s Drontal and Profender families of products in the EEA in order to remove the full overlap between their activities in the market for CA endoparasiticides. More details on this remedy are provided in Section 5 below.

(d) The Commission’s assessment

(103) As a preliminary remark, it should be noted that, unless otherwise specified, the findings set out in this Section 4.2.1.1, and in particular the results of the market investigation, do not materially differ depending on the species and MoAs.89 As regards possible differences depending on the analysed EEA country, although national specificities exist (with e.g. market share variations at national level), the main characteristics of supply and demand in the markets for feline and canine endoparasiticides (and sub-segments) do not appear to vary significantly across countries. Therefore, unless otherwise specified, the findings of Section 4.2.1.1 (regarding e.g. closeness of competition, generic competition and the feedback received from market participants) do not materially differ depending on the geographic market at stake.

(104) For the reasons set out below, the Commission considers that the Transaction raises serious doubts as to the compatibility of the Transaction with the internal market and the functioning of the EEA Agreement in some markets for CA endoparasiticides (and potential sub-segments).

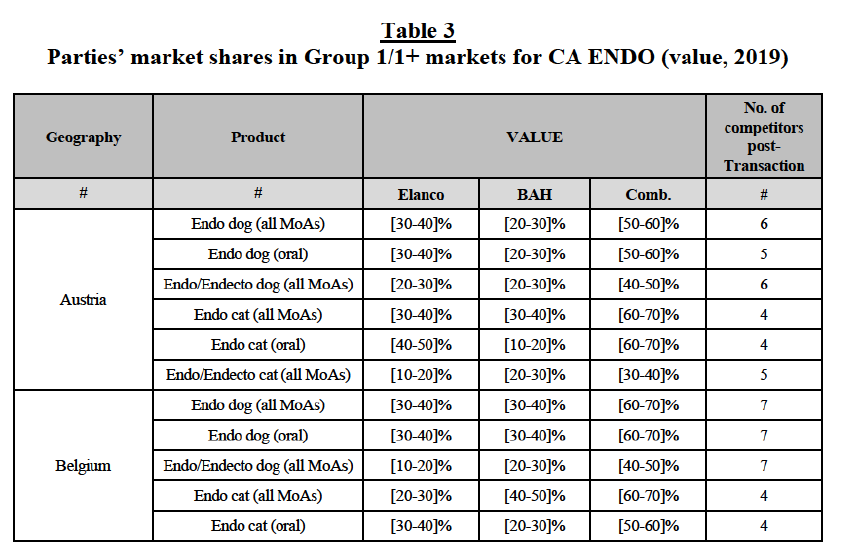

(105) First, the Commission notes that the Transaction leads to large or very large combined market shares in a number of affected markets (see Table 3 above).90 As set out in the Horizontal Merger Guidelines, market shares provide a useful first indication of the market structure and of the competitive importance of both the Parties and their competitor.91 In the present case, the Commission considers that the high market shares would lead to a significant increase of market power and/or the strengthening or creation of a dominant position of the merged entity post- Transaction. More specifically:

(a) In Austria: the Parties have high combined market shares with a significant increment in (i) the canine endo market, both encompassing all modes of administration and including oral products only ([50-60]% combined market share, with a [20-30]% increment brought by BAH); in (ii) the feline endo market ([60-70]% combined market share, with a [30-40]% increment brought by Elanco); and in (iii) the feline endo market including only products administered orally ([60-70]% combined market share, with a [10- 20]% increment brought by BAH). Post-Transaction, (a) in the canine endo market, both encompassing all modes of administration and including oral products only, the new entity would face five competitors, with Ceva and Virbac being the largest ([10-20]-[10-20]%), followed by Zoetis, Merck and Vetoquinol (with market shares between [5-10]% and below [0-5]%); and (b) in the feline endo market, both encompassing all modes of administration and considering oral products only, the new entity would face four competitors, the largest being Ceva and Virbac, with market shares between [10-20]-[10- 20]%, followed by Merck, Zoetis, Vetoquinol and BI, with market shares below [5-10]%.

(b) In Belgium: the Parties have high combined market shares in (i) the canine endo market, both encompassing all modes of administration and including oral products only ([60-70]% combined market share, with a [30-40]% increment brought by Elanco), in (ii) the feline endo market ([60-70]% combined market share, with a [20-30]% increment brought by Elanco), similarly in the (iii) the feline endo market including only products administered orally ([50-60]% combined market share, with a [20-30]% increment brought by BAH). Post-Transaction, (a) in the canine endo market, both encompassing all modes of administration and considering the products administered orally only, the new entity would face seven competitors, with Ceva and Virbac being the largest (with market shares of [5-10]% and [10- 20]%, respectively); and (b) in the feline endo market, both encompassing all modes of administration and considering oral products only, the new entity would face four competitors, the largest being Virbac and Zoetis, with market shares between [10-20]-[10-20]%, followed by Ceva and Krka, with market shares between [0-5]-[5-10]%.

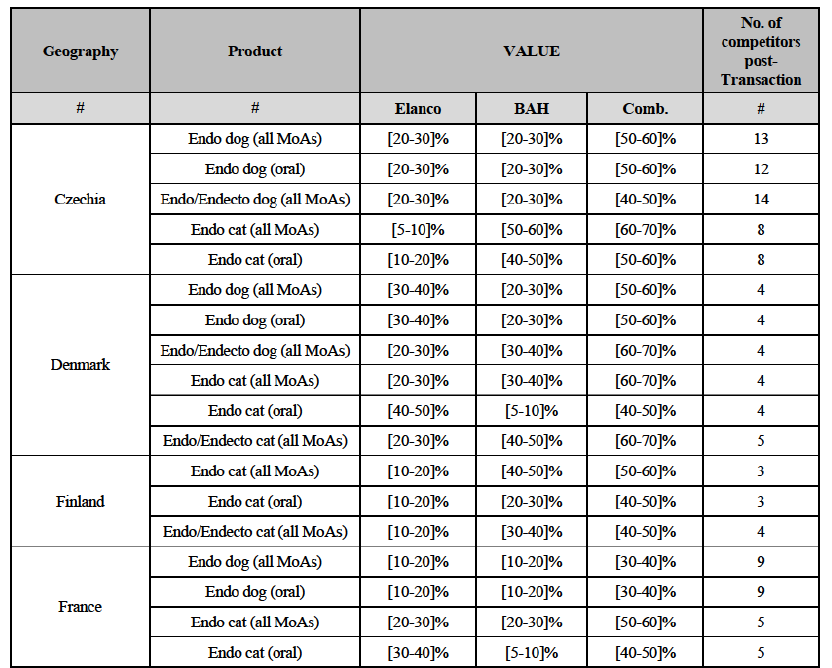

(c) In Czechia: the Parties have high combined market shares in (i) the canine endo market, both encompassing all modes of administration and including oral products only ([50-60]% combined market share, with a [20-30]% increment brought by BAH); and in (ii) the feline endo market, both encompassing all modes of administration and considering oral products only ([60-70]-[50-60]% combined market share, with a [5-10]-[5-10]% increment brought by Elanco). Post-Transaction, (a) in the canine endo market, both encompassing all modes of administration and considering only the products administered orally, the new entity would face 13-12 competitors, all with a very limited market presence (between [5-10]% and below [0-5]% market share), and only with Krka having a larger market share of [10-20]%; and (b) in the feline endo market, both encompassing all modes of administration and considering oral products only, the new entity would face eight competitors, all with a limited market presence (between [5-10]% and below [0-5]% market share) and only with Krka having a larger market share between [10- 20]-[20-30]%.

(d) In Denmark: the Parties have high combined market shares in (i) the canine endo market, both encompassing all modes of administration and considering only oral products ([50-60]% combined market share, with a [20-30]% increment brought by BAH), in (ii) the feline endo market ([60-70]% combined market share, with a [20-30]% increment brought by Elanco). Similarily, the Parties have high combined market shares in (iii) the canine endo/endecto market ([60-70]% combined market share, with a [20-30]% increment brought by Elanco) and (iv) the feline endo/endecto market ([60- 70]% combined market share, with a [20-30]% increment brought by Elanco). Post-Transaction, (a) in the canine endo market, both encompassing all modes of administration and considering only the products administered orally, the new entity would face four competitors, two of which (Merck and Virbac) with a larger market presence between [20-30]-[10-20]% market share and the other two (Ceva and Zoetis) with a negligible market share between [0-5]% and below [0-5]%; similarily, (b) in the feline endo market, the new entity would face four competitors, all with a limited market presence (between [5-10]% and below [0-5]% market share), with the only exception represented by Virbac holding a larger market share of [20-30]%; (c) in the canine endo/endecto market, the new entity would face four competitors, the largest ones being Merck ([10-20]%) and Virbac ([10-20]%) and the other two with a market share between [5-10]% and [0-5]%; and (d) in the feline endo/endecto market, the new entity would face five competitors, the largest one being Virbac ([20-30]%) and the others with a negligible market share between [0-5]% and [0-5]%.

(e) In Finland: the Parties have high combined market shares in the feline endo market ([50-60]% combined market share, with a [10-20]% increment brought by Elanco). Post-Transaction, in the feline endo market, encompassing all modes of administration, the new entity would face only three competitors, the largest one being Merck with a [30-40]% market share and the two remaining ones (Virbac and Zoetis), with market shares between [10-20]% and below [0-5]%.

(f) In France: the Parties have high combined market shares in the feline endo market ([50-60]% combined market share, with a [20-30]% increment brought by BAH). Post-Transaction, in the feline endo market, encompassing all modes of administration the new entity would face five competitors, with the larger ones being Ceva ([10-20]%) and Virbac ([10-20]%), followed by Clément Thekan ([10-20]%), and Merck and Zoetis with a market share between [0-5]% and below [0-5]%.

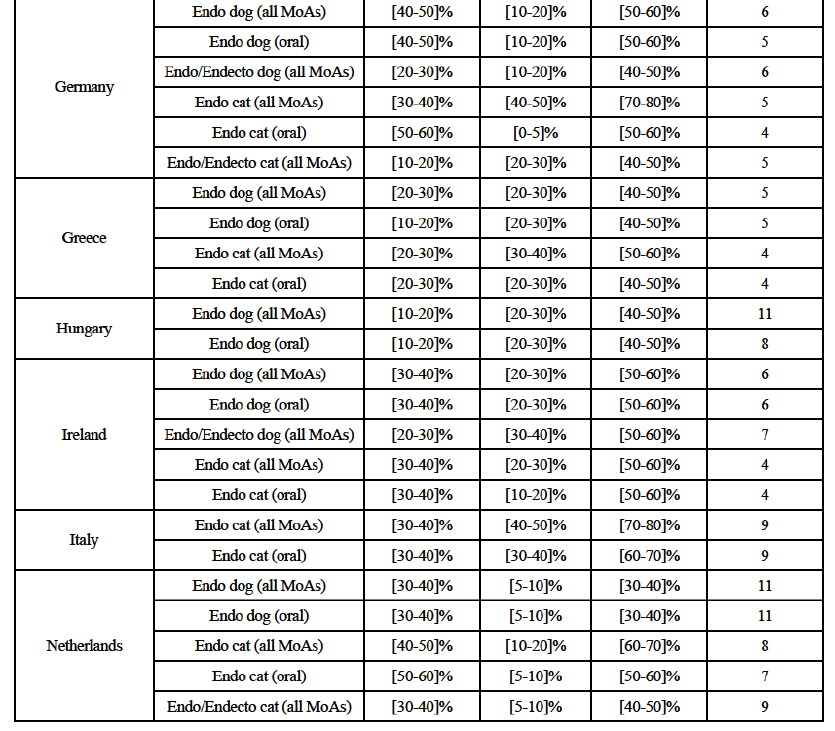

(g) In Germany: the Parties have high combined market shares in (i) the canine endo market, both encompassing all modes of administration and consideringonly oral products ([50-60]% combined market share, with a [10- 20]% increment brought by BAH), in (ii) the feline endo market ([70-80]% combined market share, with a [30-40]% increment brought by Elanco). When considering (iii) the feline endo market, including oral products only, the increment brought by BAH is less significant but still contributes to high combined market shares for the Parties ([50-60]% combined market share, with a [0-5]% increment brought by BAH). Post-Transaction, (a) in the canine endo market, both encompassing all modes of administration and considering only the products administered orally, the new entity will face 6- 5 competitors, the largest being Virbac, Merck and Ceva ([20-30]-[10-20]%) and the others with a more negligible market presence; and (b) in the feline endo market, both encompassing all modes of administration and considering oral products only, the new entity would face 5-4 competitors, the largest being Virbac ([10-20]-[20-30]%) and the others holding a more negligible market share.

(h) In Greece: the Parties have high combined market shares in the feline endo market, encompassing all modes of administration ([50-60]% combined market share, with a [20-30]% increment brought by Elanco). Post- Transaction, in the feline endo market, encompassing all modes of administration, the new entity would face four competitors, with Virbac and Zoetis being the largest ([10-20]-[20-30]%) and the others with a more limited market presence ([10-20]-[0-5]%).

(i) In Ireland: the Parties have high combined market shares in (i) the canine endo market, both encompassing all modes of administration and considering oral products only ([50-60]% combined market share, with a [20-30]% increment brought by BAH); (ii) the feline endo market, both encompassing all modes of administration and considering oral products only ([50-60]-[50- 60]% combined market share, with a [20-30]-[10-20]% increment brought by BAH) and (iii) the canine endo/endecto market ([50-60]% combined market share, with a [20-30]% increment brought by Elanco). Post-Transaction, (a) in the canine endo market, both encompassing all modes of administration and considering only the products administered orally, the new entity would face six competitors, the largest being Virbac ([30-40]%) and the others having a more negligible presence (between [5-10]% and below [0-5]%); (b) in the feline endo market, both encompassing all modes of administration and considering only the products administered orally, the new entity would face four competitors, the largest one being Virbac ([30-40]-[30-40]%) and the others having a more negligible market presence (between [5-10]% and below [0-5]%); and (c) in the canine endo/endecto market, the new entity would face seven competitors, the largest one being Virbac ([30-40]%) and the others having a more negligible market presence (all well below [5- 10]%).

(j) In Italy: the Parties have high combined market shares in the feline endo market, both encompassing all modes of administration and considering only oral products ([70-80]-[60-70]% combined market share, with a [30-40]-[30- 40]% increment brought by Elanco). Post-Transaction, in the feline endo market, both encompassing all modes of administration and considering only oral products, the new entity would face nine competitors, the largest one being Merck ([10-20]-[10-20]%) and all the others with a very negligible market presence equal to or well below [5-10]%.

(k) In the Netherlands: the Parties have high combined market shares in (i) the feline endo market, both encompassing all modes of administration and considering oral products only ([60-70]-[50-60]% combined market share, with a [10-20]-[5-10]% increment brought by BAH). Post-Transaction, in the feline endo market, both encompassing all modes of administration and considering only the products administered orally, the new entity would face 8-7 competitors, with Virbac and Beaphar being the largest ([10-20]-[10- 20]%) and the others with a more limited market presence (between [5-10]% and below [0-5]%).

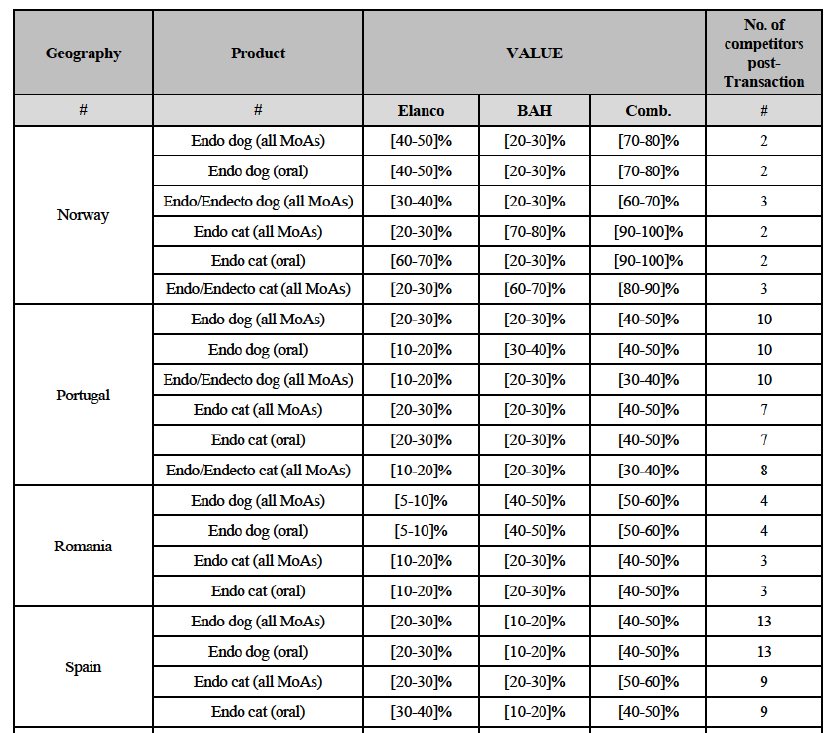

(l) In Norway: the Parties have high combined market shares (i) in the canine endo market, both encompassing all modes of administration and considering oral products only ([70-80]% combined market share, with a [20-30]% increment brought by BAH); (ii) in the feline endo market, the increment brought by Elanco being equally significant, leading to a situation of quasimonopoly ([90-100]% combined market share, with a [20-30]% increment brought by Elanco) and (iii) in the feline endo market, including oral products only ([90-100]% combined market share, with a [20-30]% increment brought by BAH). Still very high is the increment brought by BAH and Elanco, respectively, (iv) in the canine endo/endecto market ([60- 70]% combined market share, with a [20-30]% increment brought by BAH) and (v) in the feline endo/endecto market ([80-90]% combined market share, with a [20-30]% increment brought by Elanco). Post-Transaction, across the various segments, the new entity would face only 2-3 competitors, the largest being Merck and Zoetis.

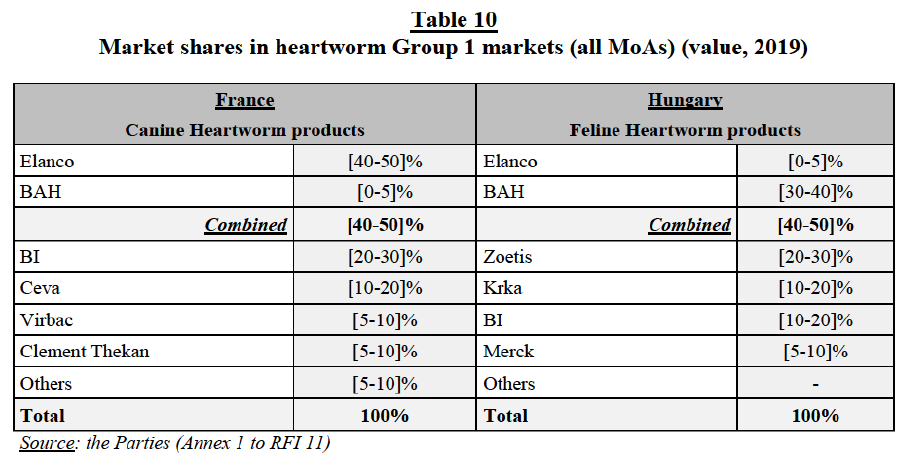

(m) In Romania: the Parties have high combined market shares in the canine endo market, both encompassing all modes of administration and considering only oral products ([50-60]-[50-60]% combined market share, with a [5-10]- [5-10]% increment brought by Elanco). Post-Transaction, in the canine endo market, both encompassing all modes of administration and considering only oral products, the new entity would face only four competitors, the largest ones being Ceva ([30-40]%) and Krka ([10-20]%), the two others with a negligible market presence equal to or well below [0-5]%.

(n) In Spain: the Parties have high combined market shares in the feline endo market, encompassing all modes of administration ([50-60]% combined market share, with a [20-30]% increment brought by BAH). Post- Transaction, in this segment, the new entity would face 9 competitors, the largest being Virbac ([10-20]%) and the others with a moderate to negligible market presence (between [10-20]% and below [0-5]%).

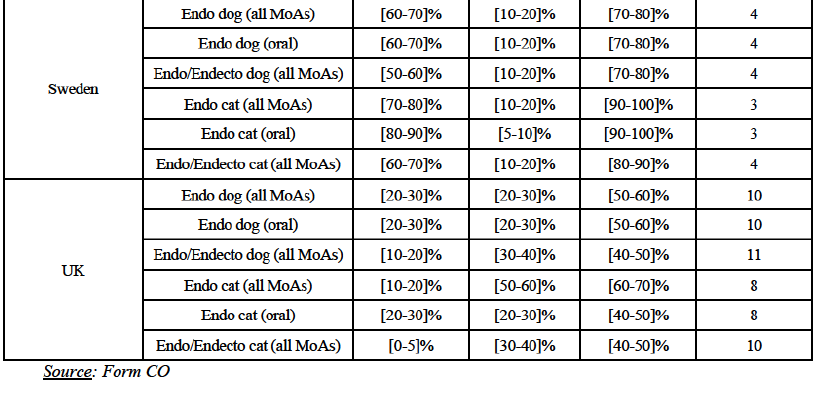

(o) In Sweden: the Parties have high combined market shares (i) in the canine endo market, both encompassing all modes of administration and considering oral products only ([70-80]% combined market share, with a [10-20]% increment brought by BAH); (ii) in the feline endo market, both encompassing all modes of administration and considering oral products only ([90-100]% combined market share, with a [10-20]-[5-10]% increment brought by BAH), leading to a situation of quasi-monopoly, and (iii) in the canine and feline endo/endecto markets ([70-80]-[80-90]% combined market share, with a [10-20]% increment brought by BAH). Post-Transaction, in all segments, the new entity would face only 3-4 competitors, the largest being Merck ([0-5]-[10-20]%) and the others (Zoetis, Virbac and BI) with a much more limited market presence (equal to or well below [5-10]%, with the exception of Zoetis which holds a [10-20]% in the canine endo/endecto market).

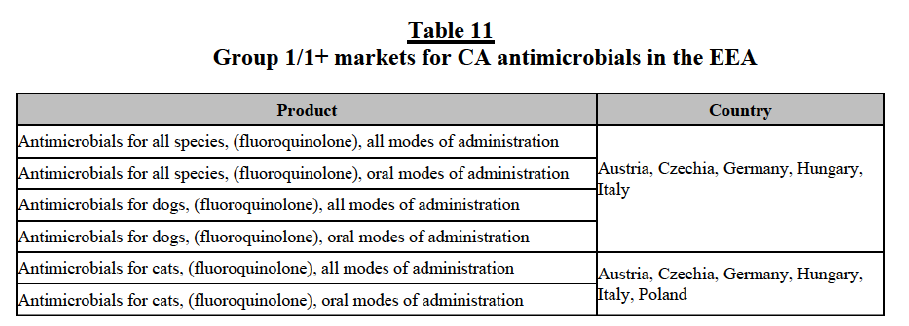

(p) In the UK: the Parties have high combined market shares with a significant increment brought by Elanco in (i) the canine endo market, both encompassing all modes of administration and including oral products only, ([50-60]-[50-60]% combined market share, with a [20-30]% increment brought by Elanco); and (ii) the feline endo market, encompassing all modes of administration ([60-70]% combined market share, with a [10-20]% increment brought by Elanco). Post-Transaction, across the various segments, the new entity would face between 10 and 8 competitors, the largest being BI, Merck, Virbac and Zoetis (with market shares varying between [20-30]% and [0-5]% across the different segments) and the others with a more limited market presence (between [5-10]% and, more frequently, below [0-5]%).

(106) Second, the results of the market investigation confirm that Elanco and BAH are perceived as close competitors and as the two largest players in the EEA markets for CA endoparasiticides, followed by BI, Ceva and Virbac. Zoetis and Merck are also mentioned among the top five competitors, although to a lesser extent.92 Competitors also stressed that (i) Elanco is an innovative player and is particularly strong thanks to its well known brands and large portfolio of products and (ii) BAH also benefits from a large portfolio of strong brands and, although less innovative than Elanco, it has a significant presence in the OTV distribution channel, which represents one of its major strengths, against other competitors.93

(107) Third, a large majority of competitors indicated that the Parties are the only alternatives available or among the very few suppliers in the EEA with respect to certain CA endoparasiticides. One competitor indicated that the merged entity would be “Dominant on the tapewormer market with Milbemax, Drontal and Profender”.94 95

(108) Fourth, the market investigation results were mixed with regards to the competitive pressure exercised by generic products over branded products in the market for CA endoparasiticides.

(109) Fifth, respondents to the market investigation indicated that there has been no material originator entry in the EEA in the past three years nor is such entry expected to occur in the next three years in the market for CA endoparasiticides and that, generally, entry in this market is perceived as difficult.96

(110) Finally, both competitors and customers, who responded to the market investigation, confirmed the existence of serious competition concerns in relation to the combination of the Parties’ marketed feline and canine endoparasiticides.

(e) Conclusion

(111) In view of the above considerations, taking into account the market investigation and all the evidence available, the Commission concludes that the Transaction raises serious doubts as to its compatibility with the internal market and functioning of the EEA Agreement with respect to overlaps between the Parties’ marketed endoparasiticides for CA in the markets/market segments listed and assessed in paragraph 105. The Commission notes that, in relation to the markets mentioned in Table 3 but not listed and assessed in paragraph 105 (see foonote 90 above), the Parties’ combined market shares and the presence of a sufficient number of competitors post-Transaction do not raise serious doubts. In any event, the Final Commitments aimed at remedying the horizontal non-coordinated effects of the Transaction in other CA endoparasiticides markets also exclude the possibility that the Transaction would lead to horizontal non-coordinated effects in those markets. Indeed, the Final Commitments will fully remove the overlap between the Parties’ activities in CA endoparasiticides at EEA level.

4.2.1.2. Ectoparasiticides97

(a) Overview of the market and the Parties’ products

(112) As explained in Section 3 above, ectoparasiticides are used to control external parasites, such as fleas and ticks.

(113) The Parties estimate that the total size of the CA ectoparasiticide sector was […] in the EEA in 201898 and explain that demand is growing due to increasing pet adoption and expenditure on veterinary healthcare.

(114) A number of chemical classes are used in ecto products. Most of them were originally developed for crop protection applications and subsequently applied to animal health. The main ecto chemical classes currently available on the market (which can be used alone or in combination) are: pyrazoles, neonicotinoids, pyrethroids, insect growth regulators, spinosyns and isox products (the newest class

new entity would face significant competition across the EEA from a range of competitors, including (i) three significant players (i.e. BI, Merck and Zoetis), with at least two of them equalling or surpassing BAH in size, and (ii) several smaller rivals (such as Ceva and Virbac), with market shares comparable to Elanco’s. Third, the Parties claim that their products face strong competitive constraints from generics (several of their products being off-patent, including Elanco’s Comfortis and Capstar, as well as most of BAH’s Advantage family of products). Fourth, it is argued that competitors supplying CA ectoparasiticides in other EEA countries can easily and quickly expand to countries giving rise to Group 1 markets. Finally, Elanco and BAH argue that their products do not closely compete as they are differentiated (i) in terms of MoAs, Elanco’s key brands (i.e. Comfortis, Credelio, Capstar) being all administered orally, whereas BAH’s key brands (i.e. Advantix, Advantage and Seresto) are administered topically or by collar; (ii) in terms of spectrum of indications, BAH’s key brands being indicated for use against a broader range of ectoparasites compared to Elanco’s portfolio (Comfortis and Capstar, being only active against fleas) and (iii) in terms of distribution channels, Elanco focusing on veterinarians, whereas BAH increasingly distributes its products through the OTV channel.

(d) The Commission’s assessment

(122) As a preliminary remark, it should be noted that, unless otherwise specified, the findings set out in this Section 4.2.1.2, and in particular the results of the market investigation, do not materially differ depending on the species or the mode of administration.102 As regards possible differences depending on the analysed EEA country, although national specificities exist (with e.g. market share variations at national level), the main characteristics of supply and demand in the markets for feline and canine ectoparasiticides do not appear to vary significantly across countries. Therefore, unless otherwise specified, the findings of Section 4.2.1.2 (regarding e.g. closeness of competition, generic competition and the feedback received from market participants) do not materially differ depending on the geographic market at stake.

(123) The evidence in the Commission’s file generally confirms the Parties’ claims. It allows the Commission to exclude serious doubts as to the compatibility of the Transaction with the internal market and the functioning of the EEA Agreement resulting from the overlap of the Parties’ activities in feline and canine ectoparasiticites regardless of possible further segmentations.

(124) First, it appears from Table 6 above that the Transaction gives rise to Group 1 markets for CA ecto in only seven countries, with combined shares not exceeding 50% and a moderate increment brought by Elanco comprised between 1% and 10% (except in two cases where the increment is above 10%). More specifically:

(a) In Belgium: the Parties have medium combined market shares with a limited or moderate increment brought by Elanco in (i) the canine ecto market ([30- 40]%, with a [0-5]% increment), and (ii) the feline ecto market ([40-50]%, with a [5-10]% increment). Post-Transaction, in both markets, the new entity would face significant competitors, with market shares above [20-30]%, namely Merck and BI, as well as several other players (including Zoetis, Ceva and Virbac);

(b) In Czechia: the Parties have medium combined market shares with a modest increment brought by Elanco in (i) the canine ecto market ([30-40]%, with a [0-5]% increment), (ii) the feline ecto market ([40-50]%, with a [0-5]% increment), and (iii) the canine ecto/endecto market ([30-40]%, with a [0-5]% increment). Post-Transaction, in the above markets, the new entity would face at least three competitors with market shares well above the increment (between [5-10]% and [40-50]%), namely Merck, BI and Zoetis, as well as several other players, such as Ceva, Virbac, Vetoquinol and Krka (whose market shares are comparable to Elanco’s);

(c) In France: the Parties have a combined market share of [40-50]% in the feline ecto market ([10-20]% for Elanco and [20-30]% for BAH). Post- Transaction, the new entity would face (i) two significant competitors, with market shares above [10-20]%, namely BI ([20-30]%) and Merck ([10- 20]%), (ii) several other meaningful players, including Clement Thekan ([5- 10]%) and Virbac ([5-10]%), as well as (iii) generic players (such as Biocanina, Krka and Vetoquinol);

(d) In Italy: the Parties have medium combined market shares with a modest increment brought by Elanco in (i) the canine ecto market ([40-50]%, with a [0-5]% increment), and (ii) the canine ecto/endecto market ([30-40]%, with a [0-5]% increment). Post-Transaction, in both markets, the new entity would face two significant competitors, with market shares comprised between [10- 20]% and [30-40]%, namely BI and Merck, and several other players, including three rivals with market share above the increment (i.e. Zoetis, Ceva and Virbac);

(e) In the Netherlands: the Parties’ combined market shares do not exceed [50- 60]%, with a limited or moderate increment brought by Elanco in (i) the canine ecto market ([30-40]%, with a [0-5]% increment), (ii) the feline ecto market ([50-60]%, with a [5-10]% increment), and (iii) the feline ecto/endecto market ([30-40]%, with a [5-10]% increment). Post-Transaction, in the above markets, the new entity would face many competitors, including significant players with market shares well above [10-20]% (such as Merck and BI, as well as Zoetis in the feline ecto/endecto market) and several other players (such as Ceva, Virbac, and Fengo);

(f) In Portugal: the Parties have medium combined market shares with a moderate increment brought by Elanco in (i) the feline ecto market ([40- 50]%, with a [5-10]% increment), and (ii) the feline ecto/endecto market ([30-40]%, with a [5-10]% increment). Post-Transaction, in both markets, the new entity would face two significant competitors, with market shares comprised between [10-20]% and [20-30]%, namely BI and Merck, as well as several other players (such as Calier, Ceva, Virbac, Zoetis, and Vetoquinol); and

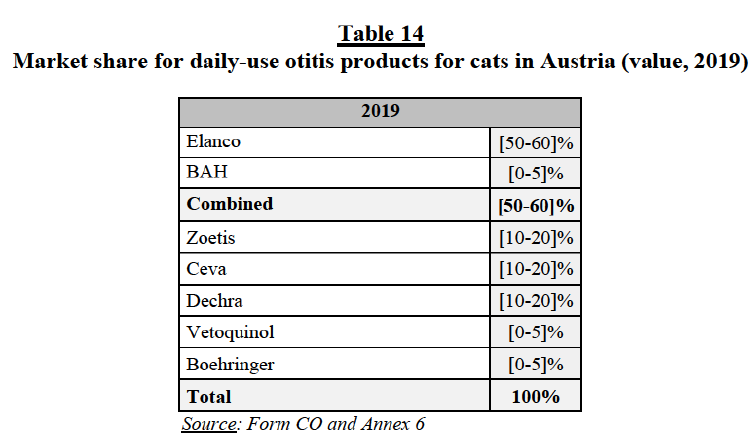

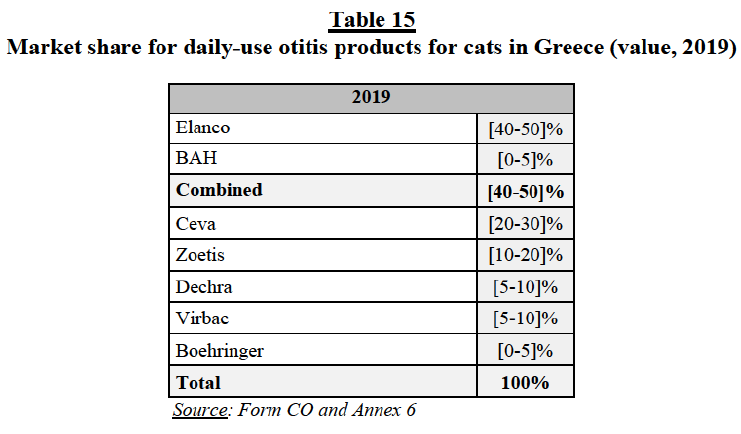

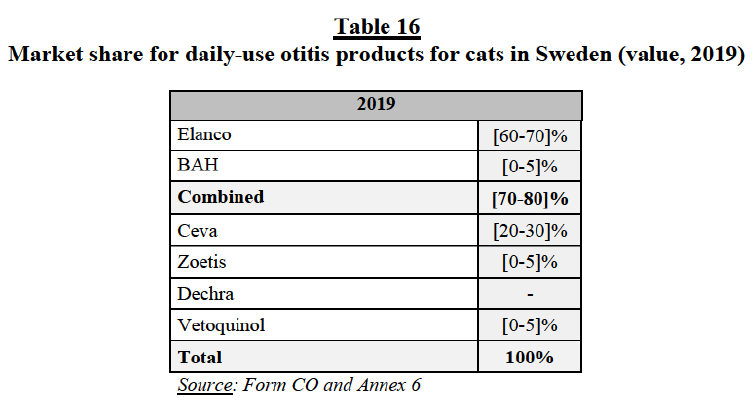

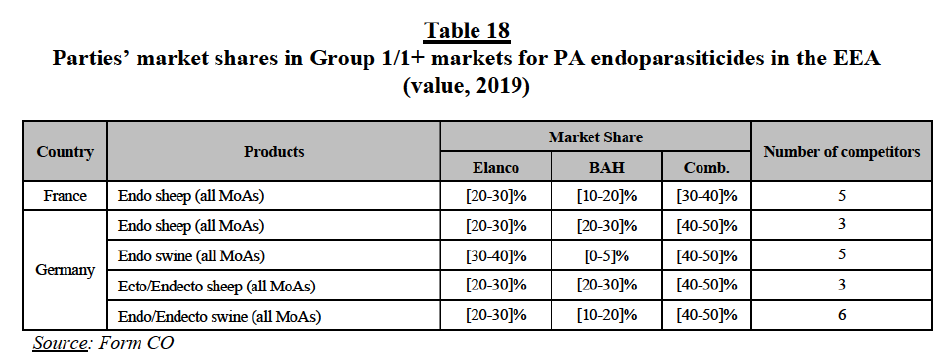

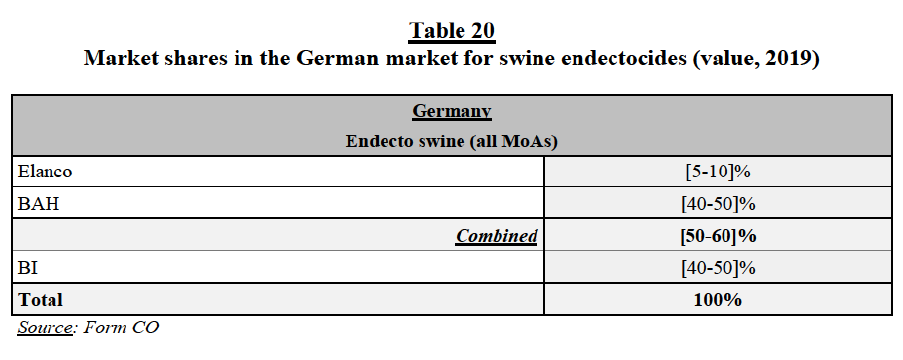

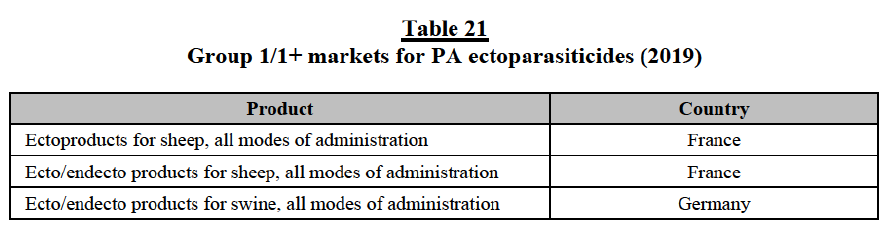

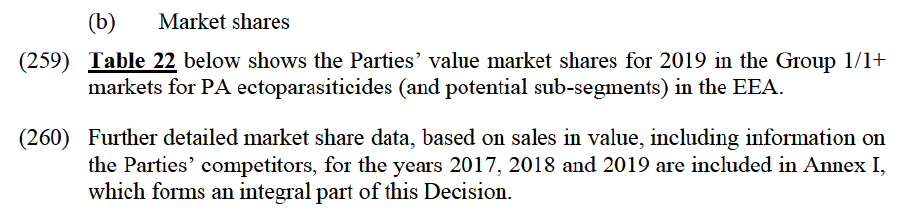

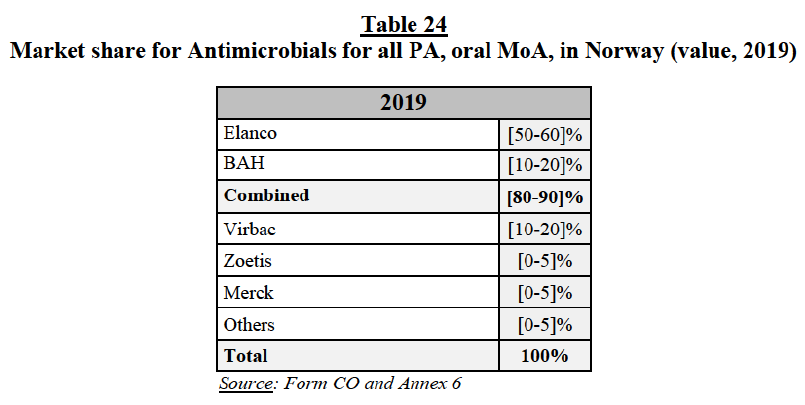

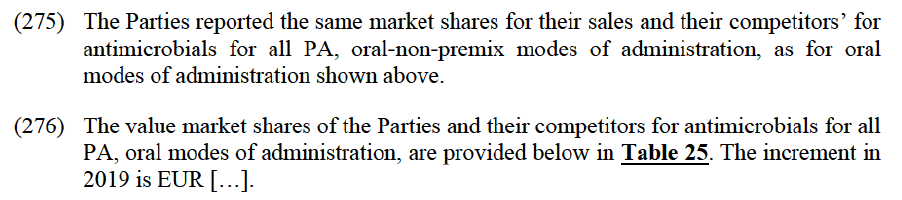

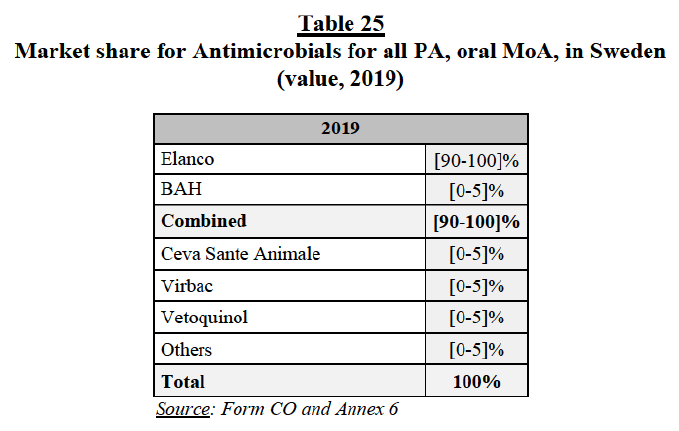

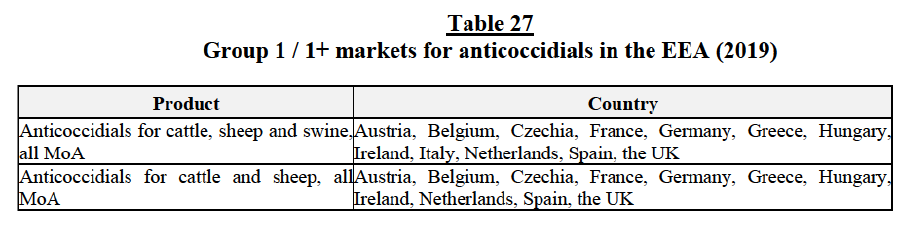

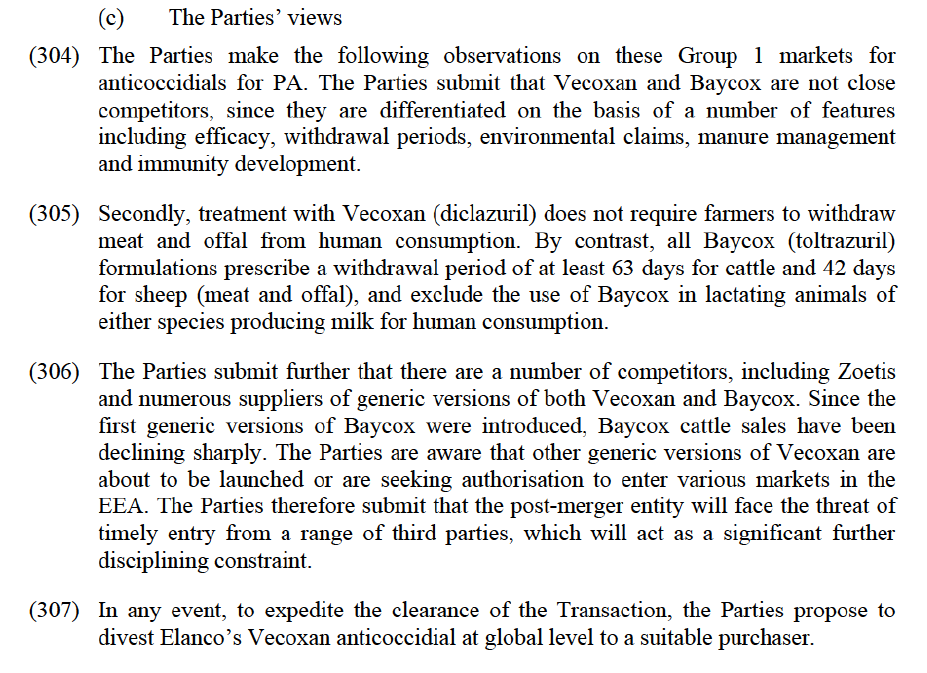

(g) In Spain: the Parties have a medium combined market share of [30-40]% in the feline ecto market ([10-20]% for Elanco and [20-30]% for BAH). Post- Transaction, the new entity would face many competitors, including (i) one rival with a comparable market share, namely BI ([30-40]%), (ii) two other meaningful players, i.e. Merck ([5-10]%) and Virbac ([5-10]%), and (iii) several other competitors (e.g. Ceva, Ecuphar, Beaphar, Karizoo, Vetoquinol).