Commission, March 10, 2016, No M.7746

EUROPEAN COMMISSION

Decision

TEVA / ALLERGAN GENERICS

Dear Sirs,

To the notifying parties:

Subject: Case M.7746 – TEVA / ALLERGAN GENERICS

Commission decision pursuant to Article 6(1)(b) in conjunction with Article 6(2) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2

(1) On 21 January 2016, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which the undertaking Teva Pharmaceuticals Industries Limited ("Teva", Israel) intends to acquire within the meaning of Article 3(1)(b) of the Merger Regulation control of the global generic pharmaceuticals business ("Allergan Generics") of Allergan plc ("Allergan", Ireland), by way of purchase of shares and assets (the "Transaction").3 Teva and Allergan Generics are designated hereinafter as the "Parties".

I. THE PARTIES

(2) Teva is a global pharmaceutical company with its corporate headquarters in Israel, involved in the development, production and marketing of generic and proprietary pharmaceutical products, as well as biopharmaceuticals and active pharmaceutical ingredients.

(3) Allergan Generics includes the global generic pharmaceuticals business of Allergan (formerly known as Actavis), an international pharmaceutical company headquartered in Ireland, including the U.S. and international generic commercial units, third-party supplier Medis, global generic manufacturing operations, the global generic R&D unit, the international over-the-counter commercial unit (excluding eye care products) and some established international brands.

II. THE OPERATION

(4) On 26 July 2015, the Parties entered into a Master Purchase Agreement, pursuant to which Teva will acquire the shares and assets constituting Allergan Generics from Allergan.

(5) Teva will therefore acquire sole control over Allergan Generics within the meaning of Article 3(1)(b) of the Merger Regulation.

III. UNION DIMENSION

(6) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR 5 000 million.4 Each of them has an EU-wide turnover in excess of EUR 250 million, but each does not achieve more than two-thirds of its aggregate EU-wide turnover within one and the same Member State. The Transaction therefore has a Union dimension.

IV. ASSESSMENT

IV.1. Introduction

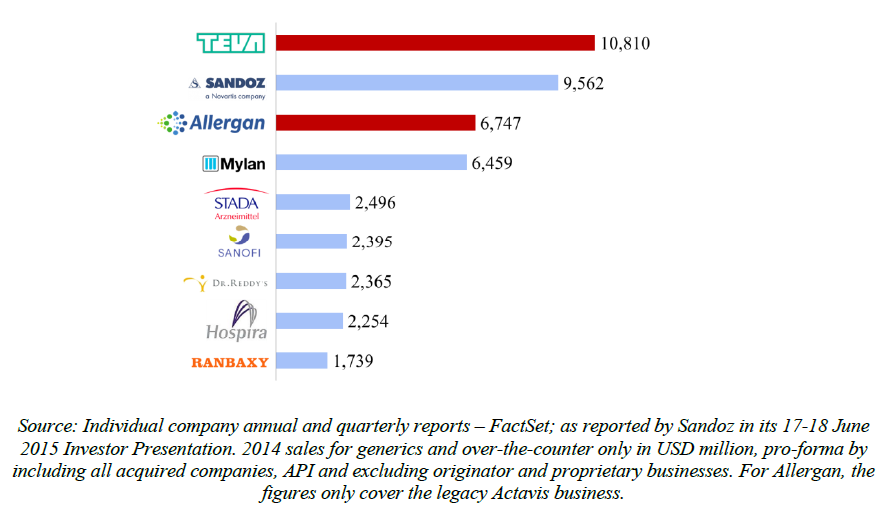

(7) Following a trend of consolidation amongst generic players, the Transaction would combine two of the four largest generic players globally (with Sandoz/Novartis and Mylan), which are followed by a long tail of smaller suppliers.

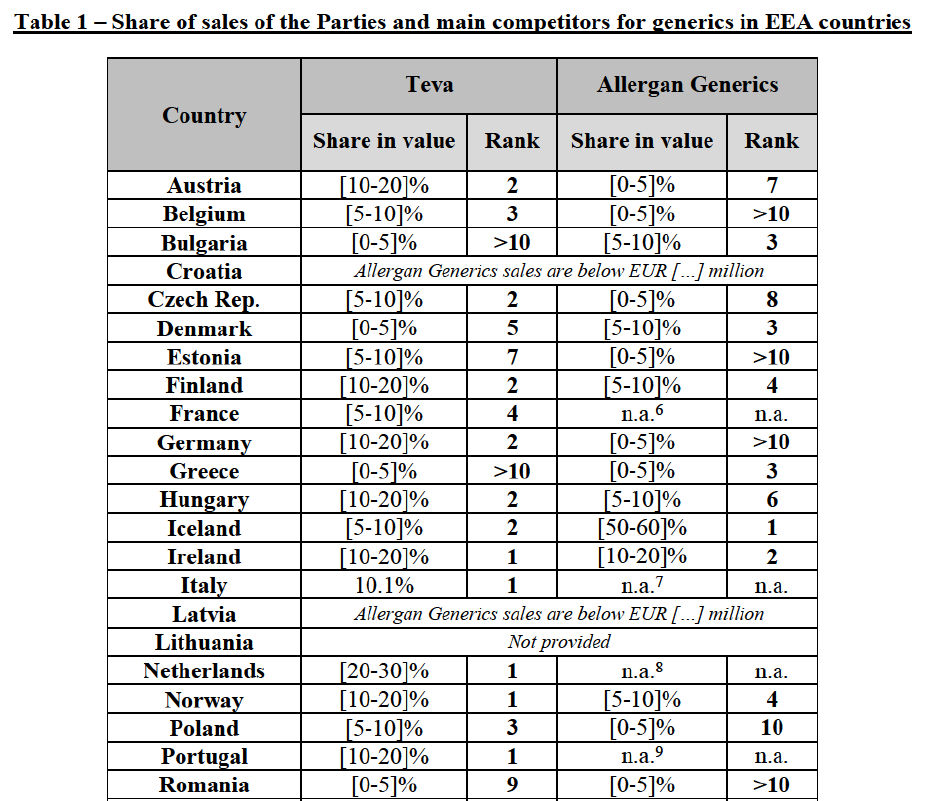

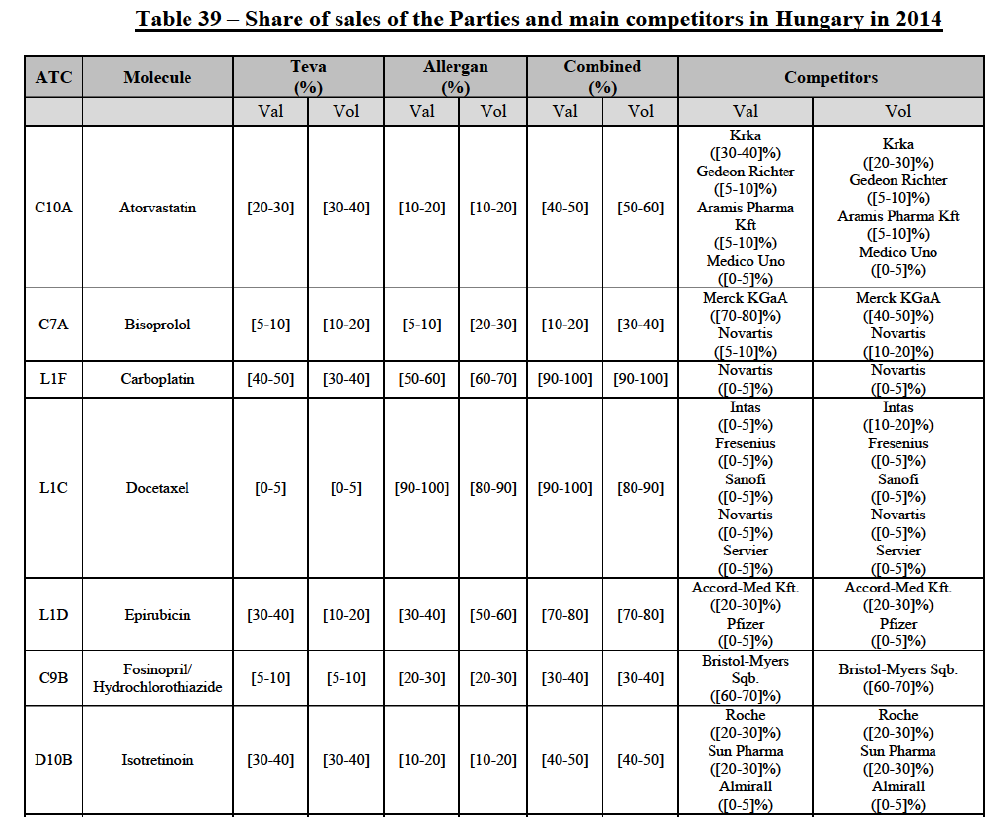

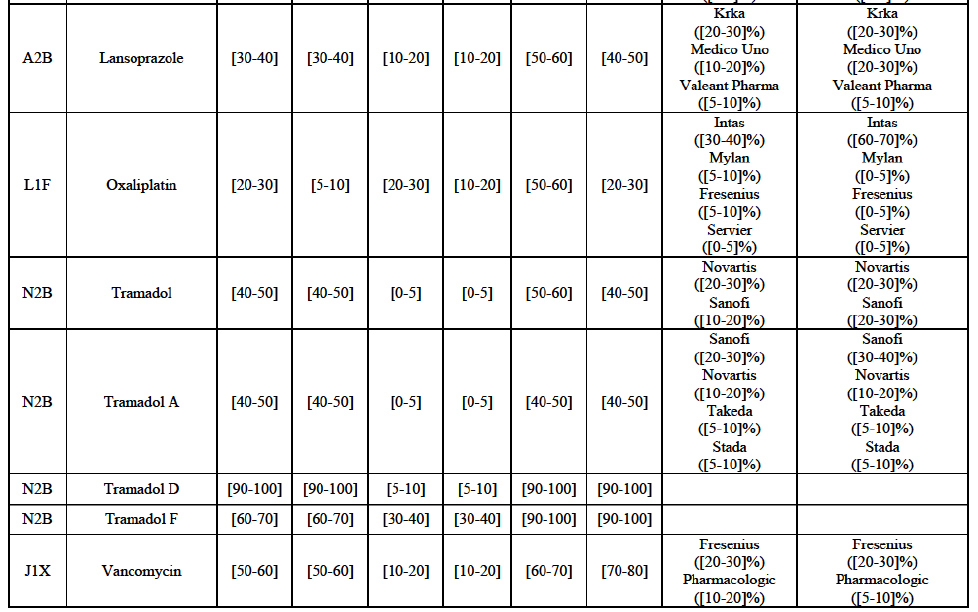

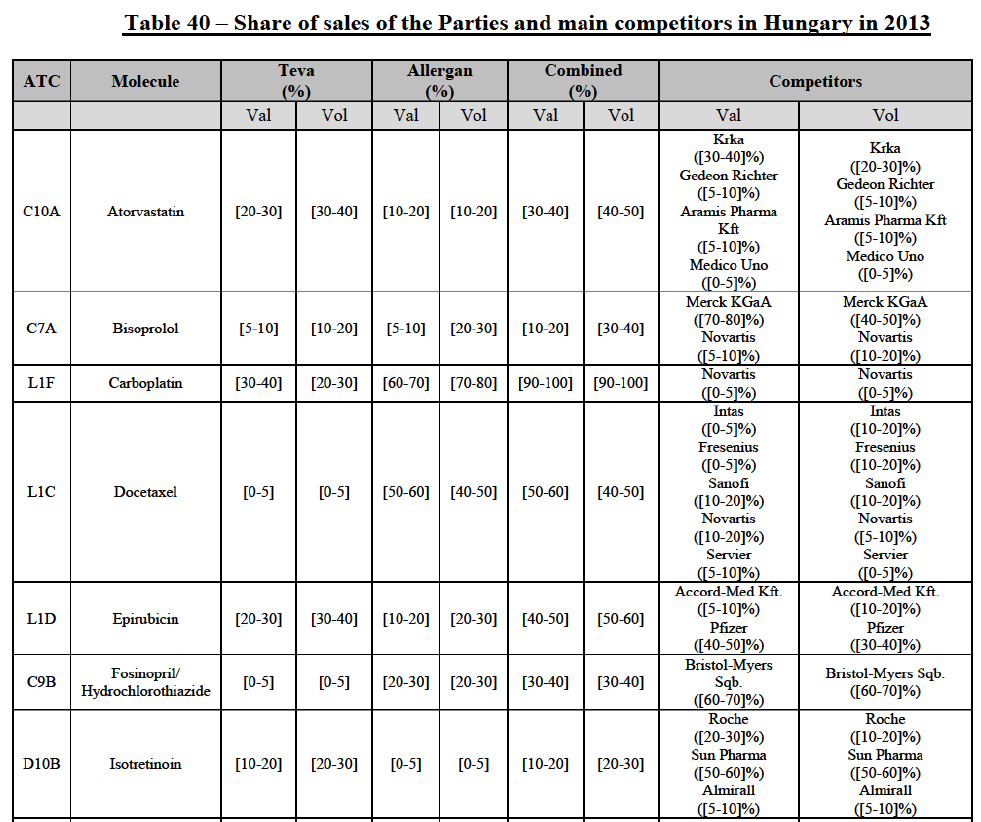

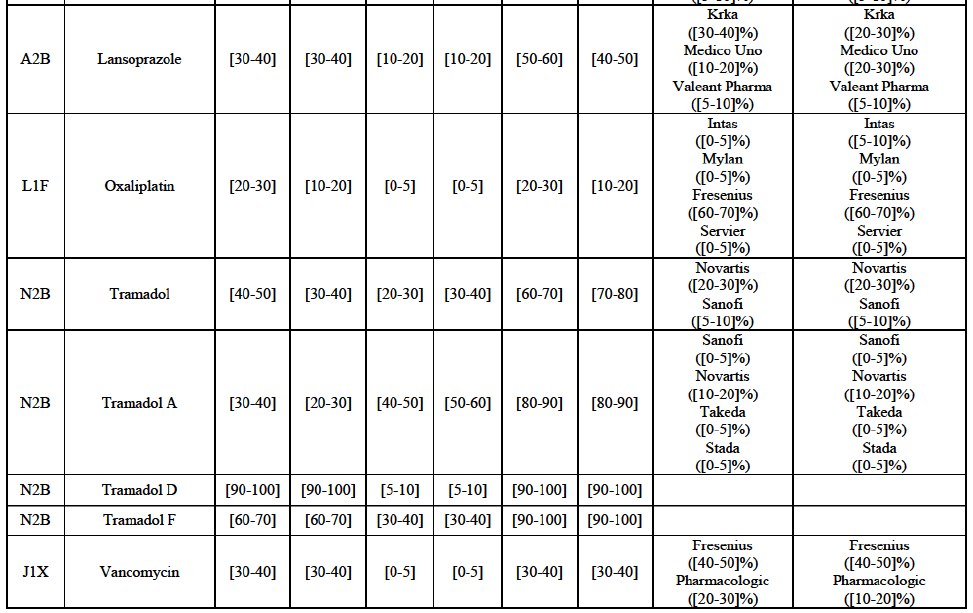

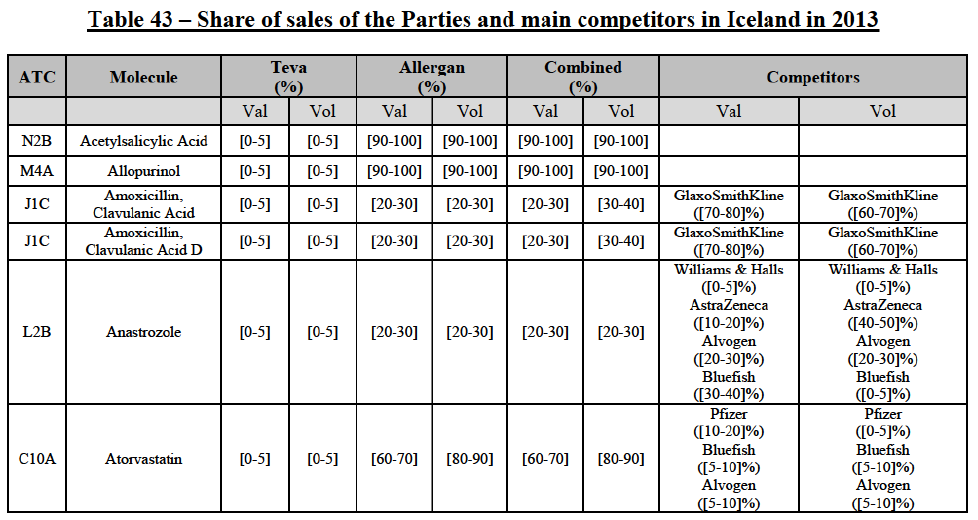

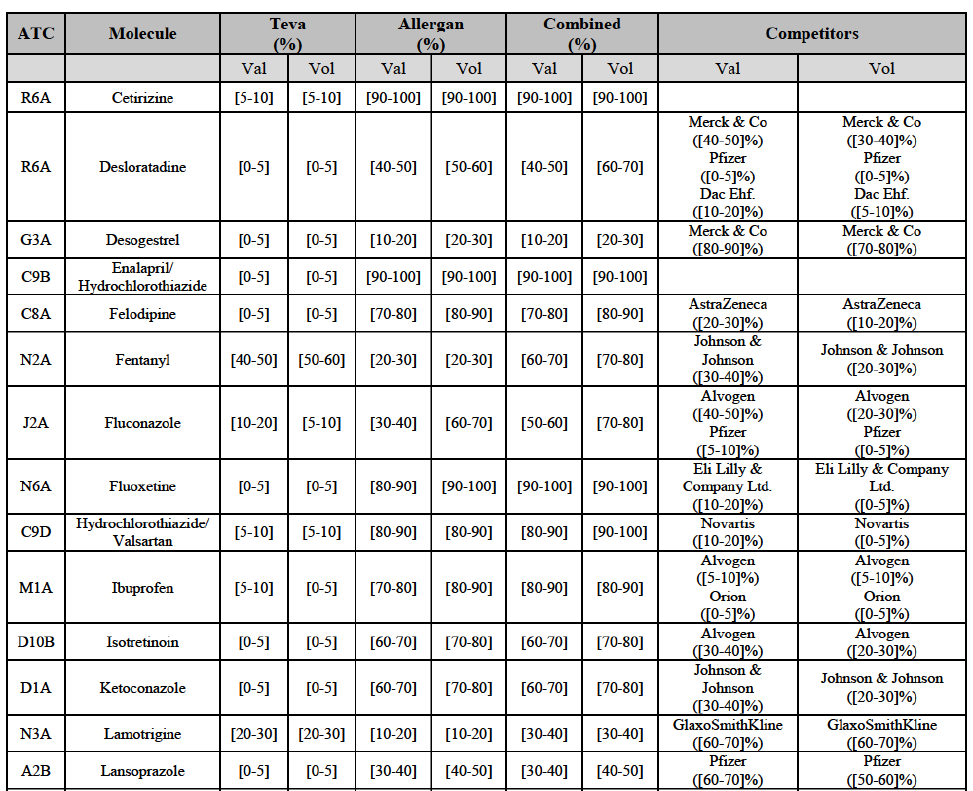

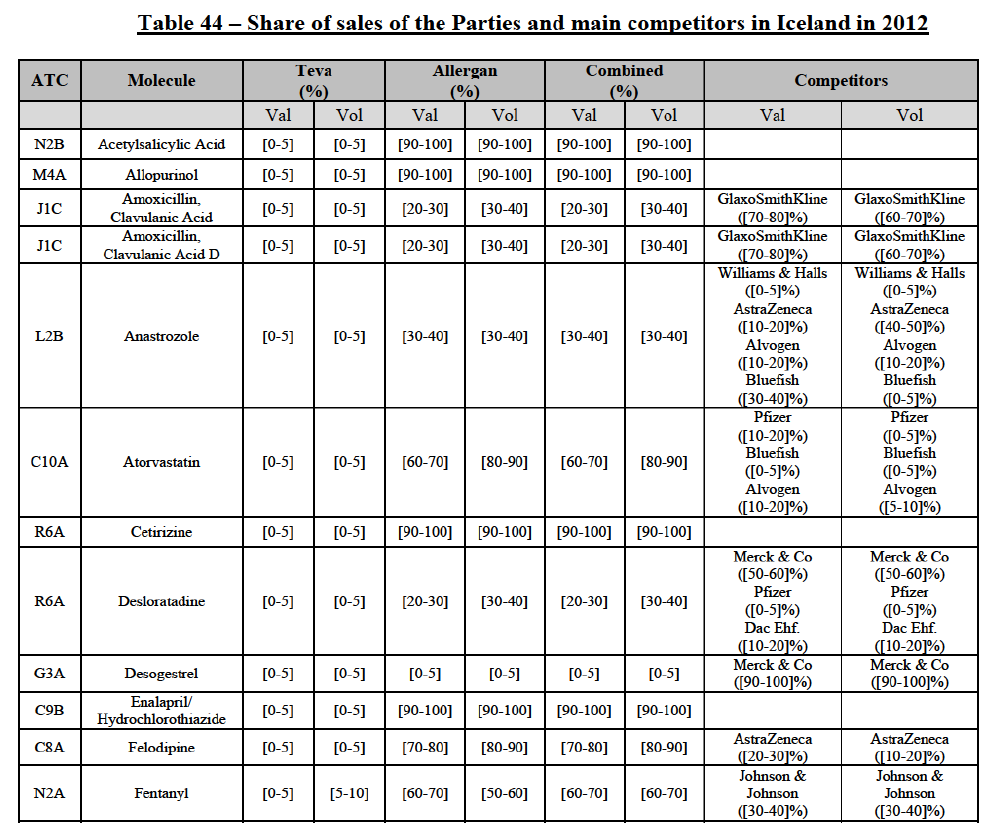

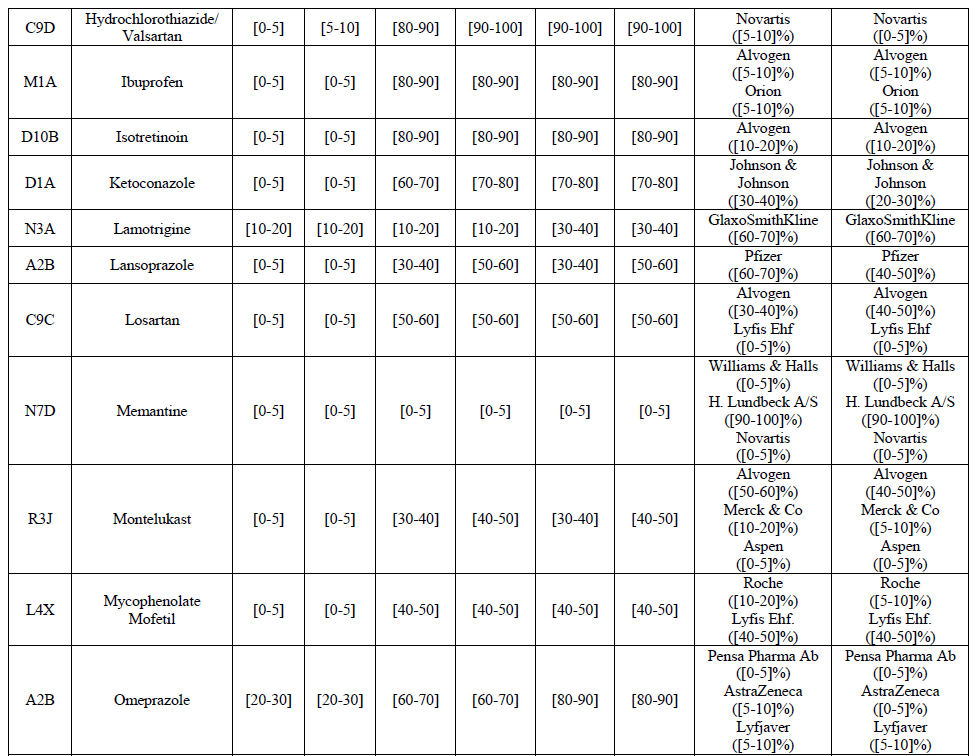

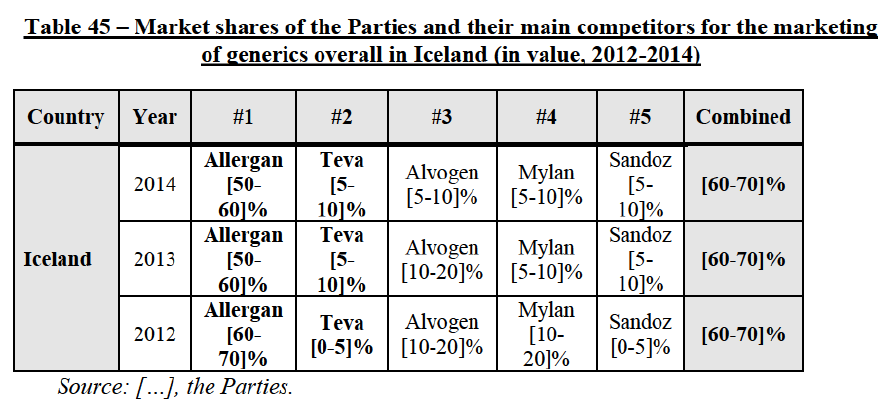

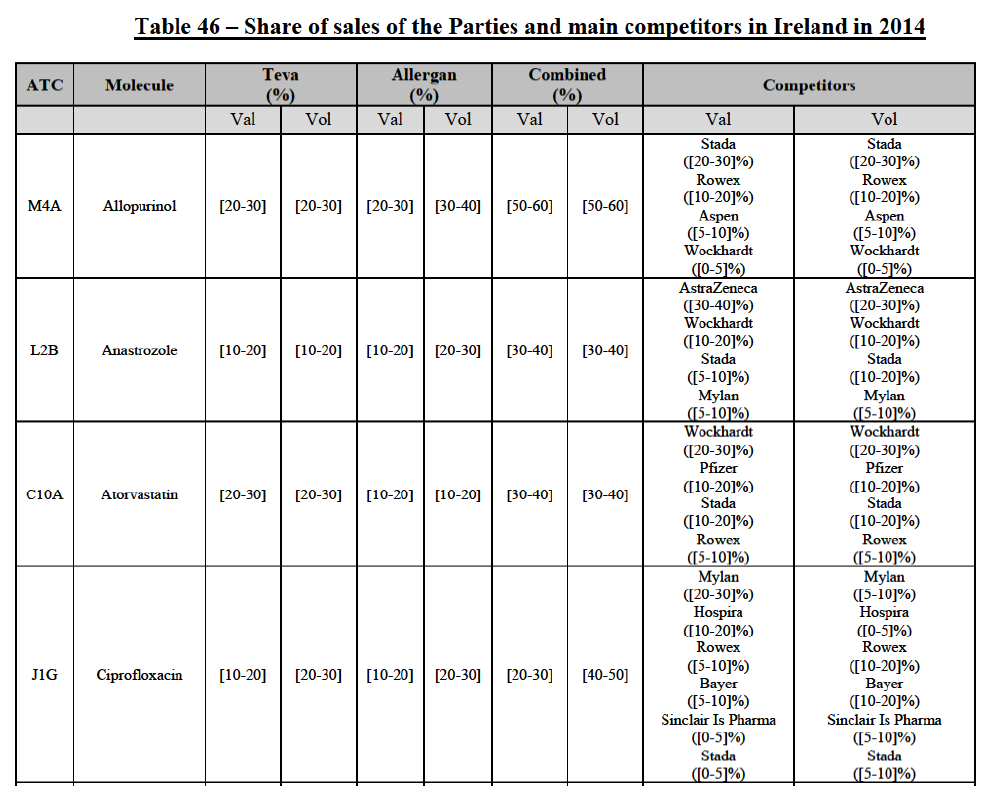

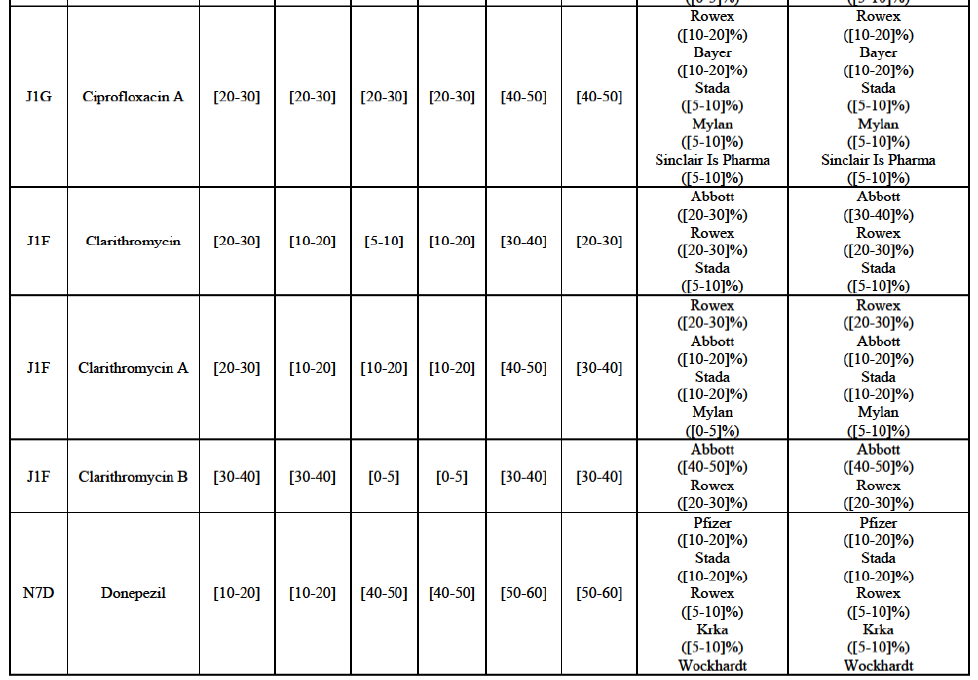

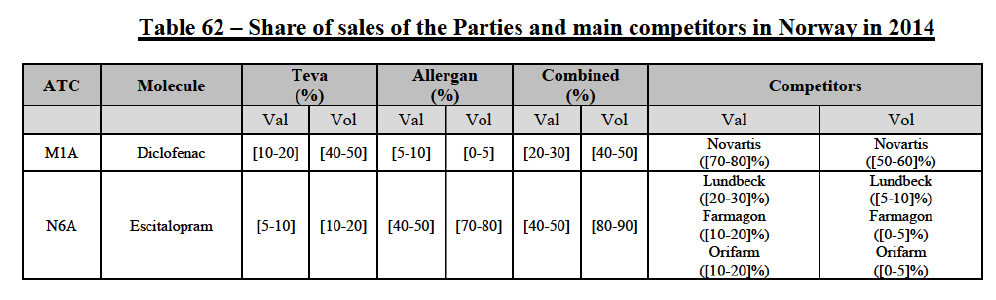

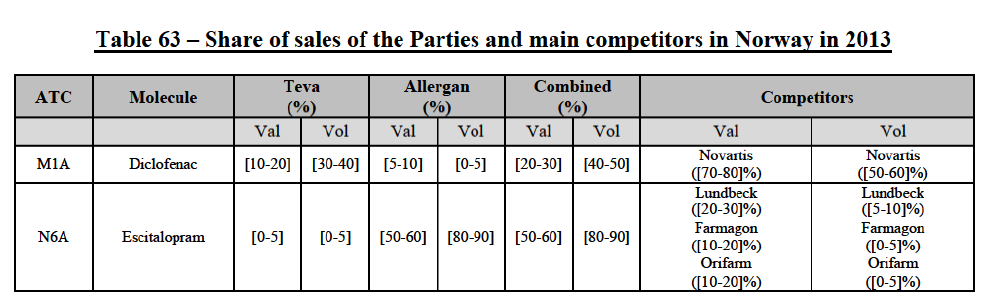

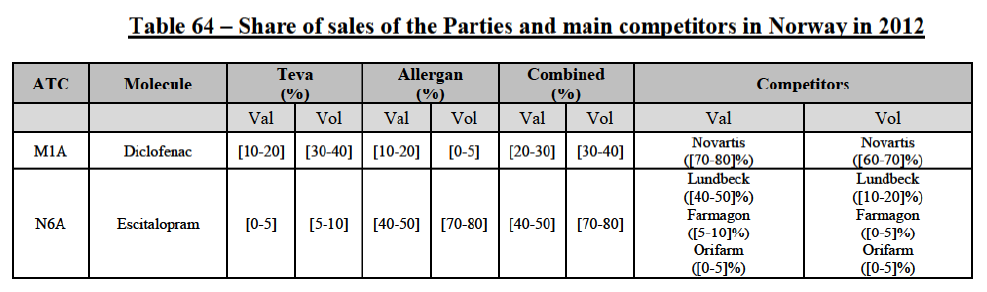

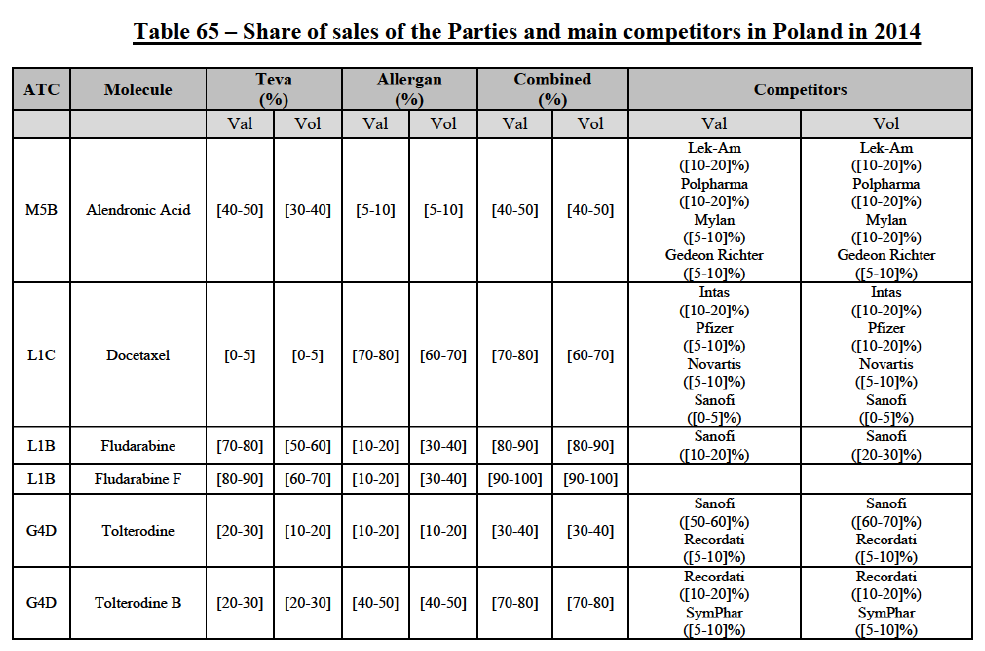

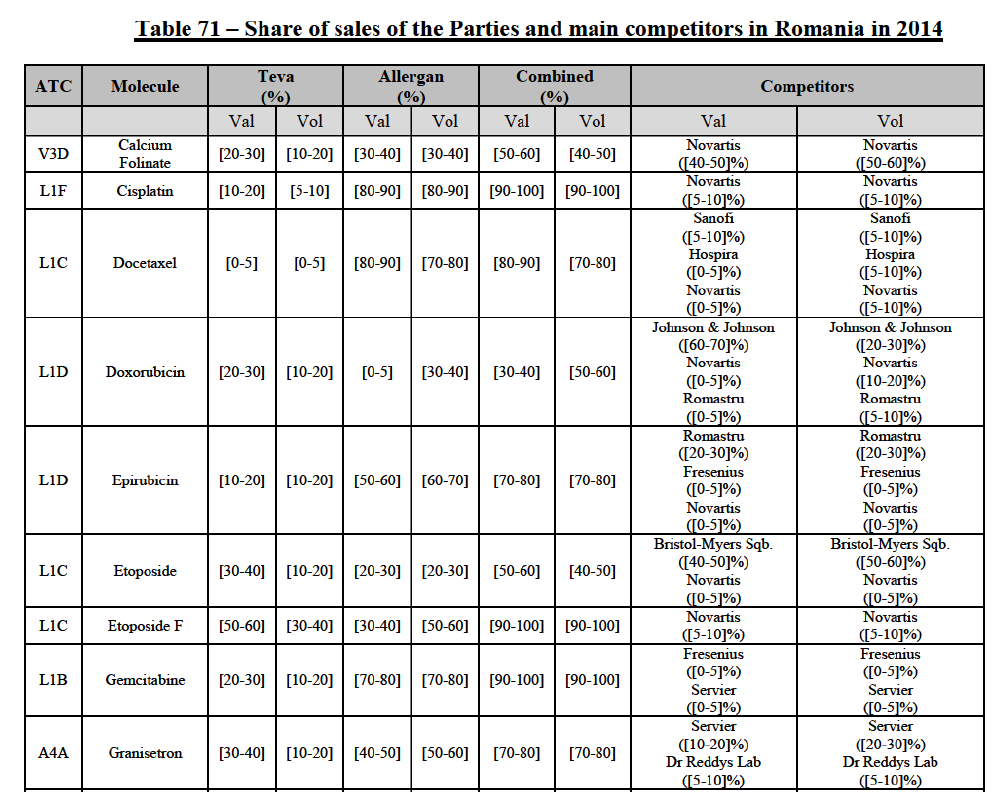

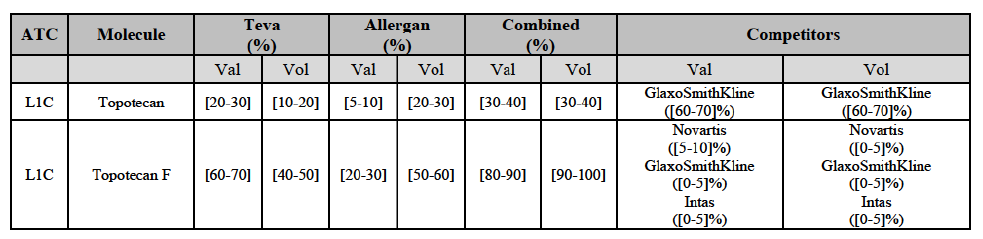

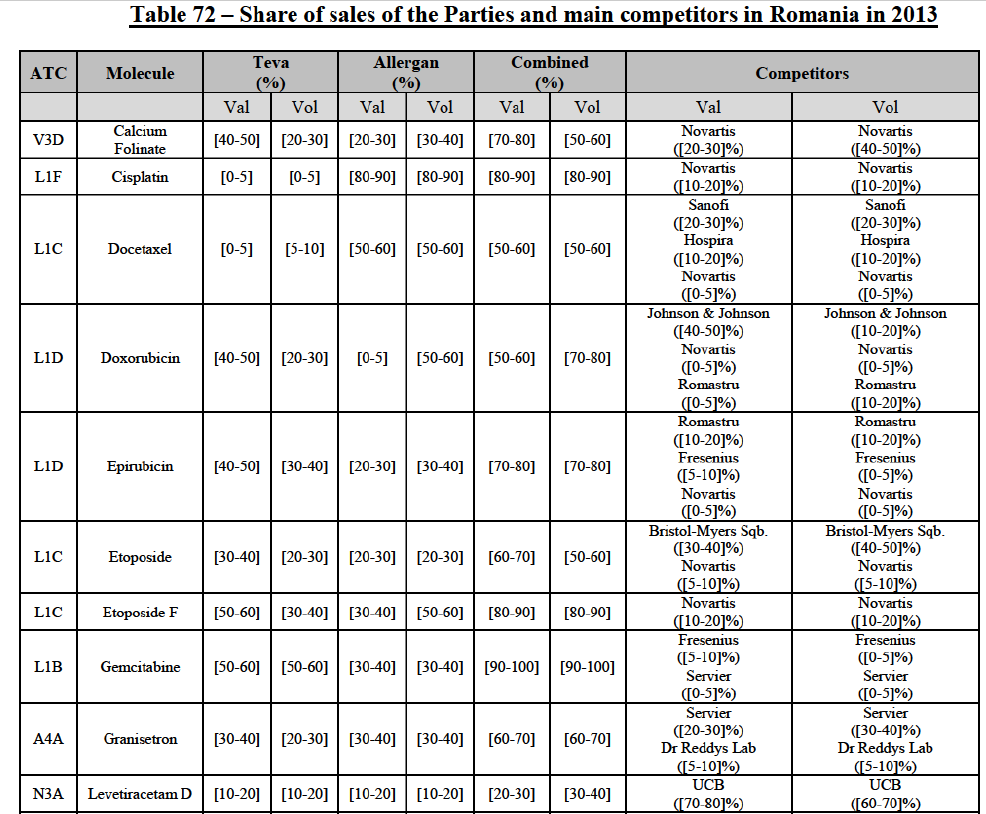

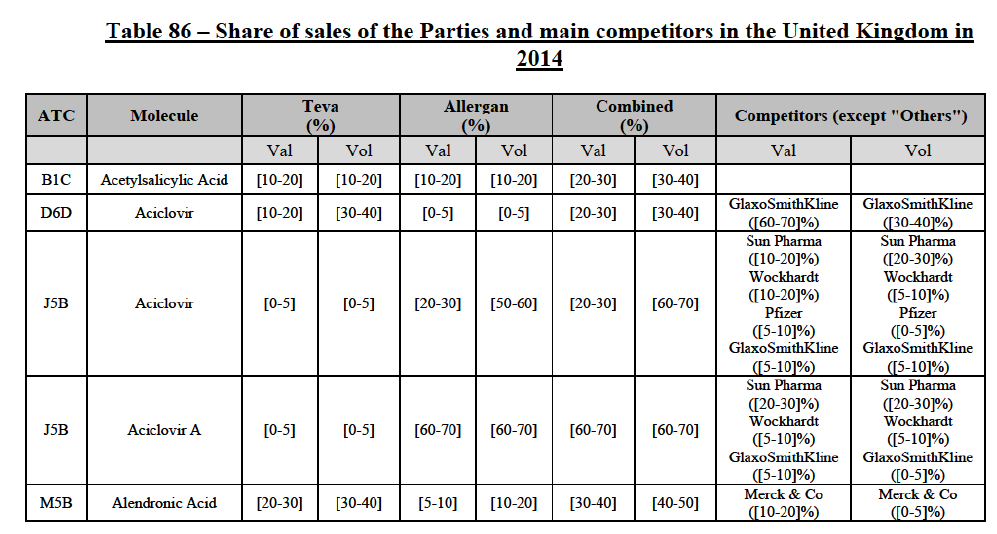

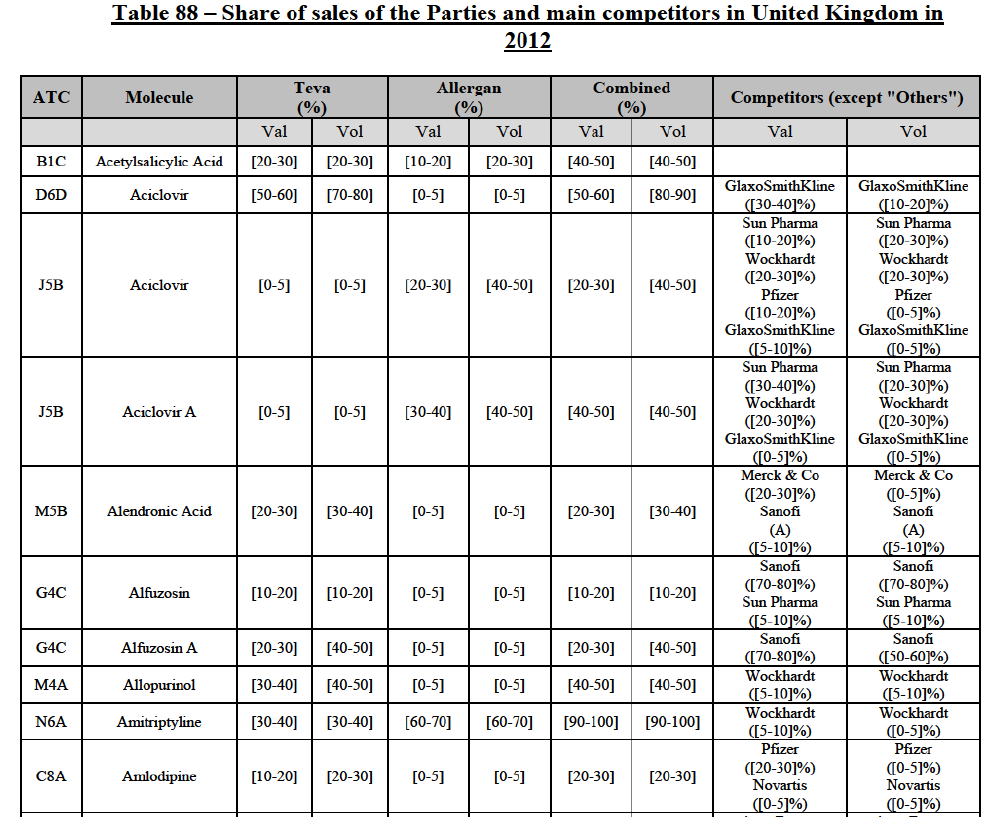

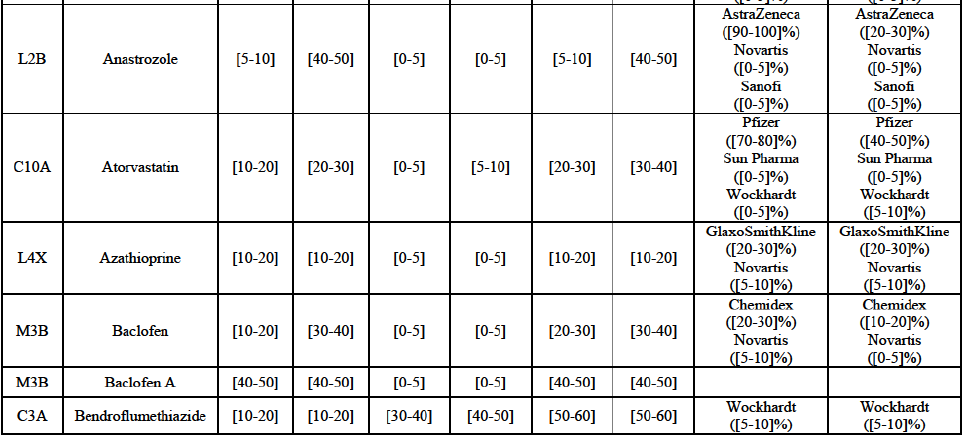

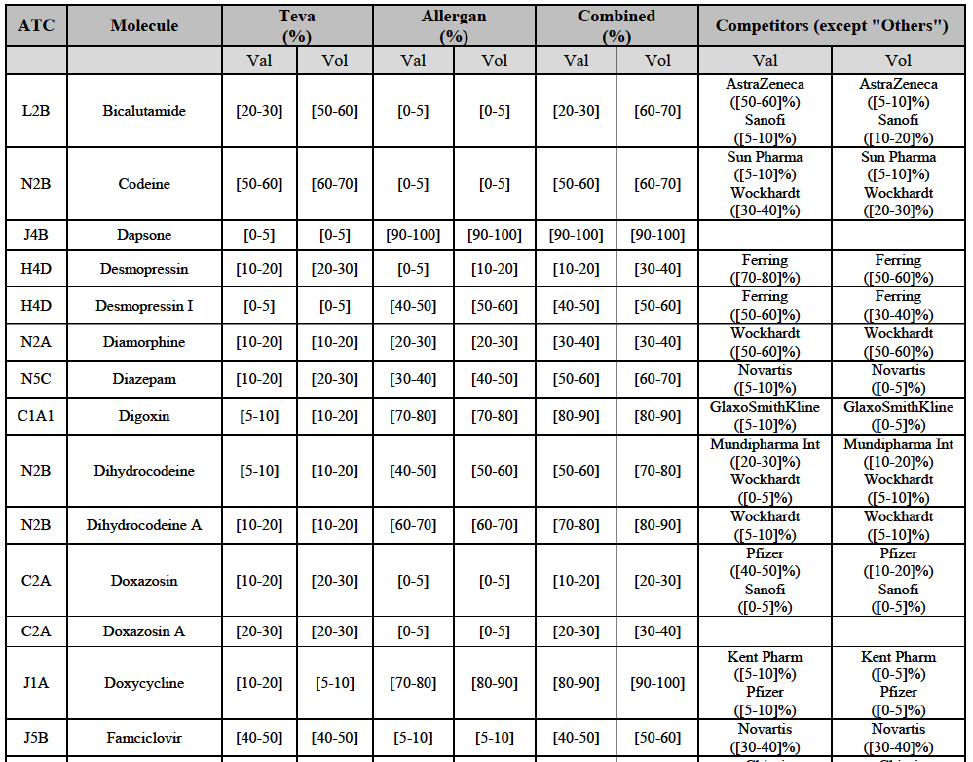

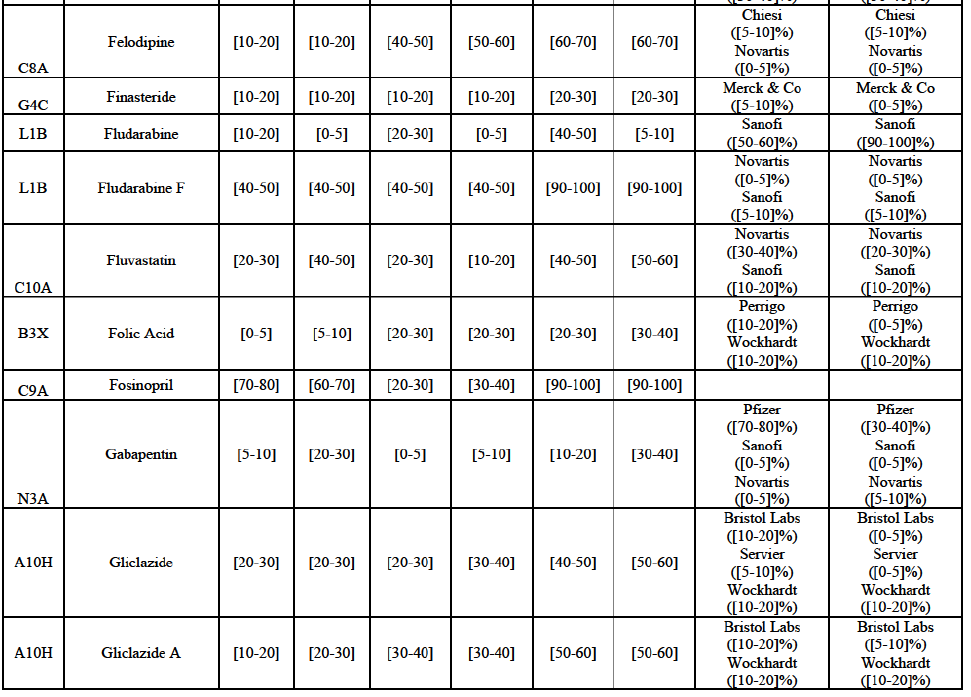

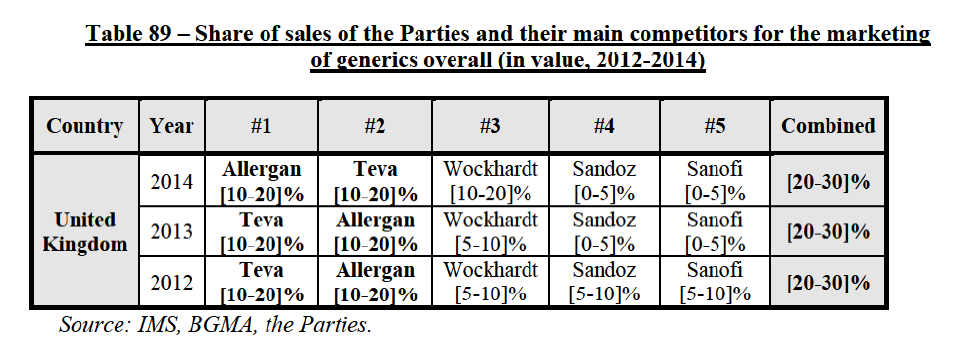

(8) The market share in value and rank of the Parties regarding the sales of generics is presented below for each EEA country in 2014.5

(9) The Parties activities overlap in relation to a vast number of affected markets in relation

to marketed and pipeline finished dose pharmaceuticals (hereafter "FDPs" or "pharmaceuticals"), see section IV.2. A vast number of vertical relationships also arise in relation to the out-licensing and contract manufacturing of FDPs to third parties, see section IV.3, as well as to the supply of active pharmaceutical ingredients ("API")11 used to manufacture FDPs, see section IV.4.

IV.2. Finished dose pharmaceuticals

IV.2.1. Market definition

IV.2.1.1. Marketing of pharmaceuticals

IV.2.1.1.a. Marketed generic pharmaceuticals

Product market definition

(10) Through the assessment of the relevant market definition in past decisions dealing with the marketing of generic pharmaceuticals,12 the Commission has established a number of principles. In those decisions it noted that medicines may be subdivided into therapeutic classes by reference to the Anatomical Therapeutic Classification ("ATC"), devised by the European Pharmaceutical Marketing Research Association ("EphMRA")13 and maintained by EphMRA and Intercontinental Medical Statistics ("IMS").

(11) In the EphMRA ATC system, medicines are classified into groups at four different levels. In the first and broadest level (ATC1), medicinal products are divided into the 16 main anatomical groups. The second level (ATC2) represents either a pharmacological or therapeutic group. The third level (ATC3) further groups medicinal products by their specific therapeutic indications, i.e. their intended use. The ATC4 level is the most detailed one (not available for all ATC3) and refers for instance to the mode of action (e.g. distinction of some ATC3 classes into topical and systemic depending on their way of action) or any other subdivision of the group. Finally, the level of the chemical substance is the so-called molecule level.

(12) In its past merger decisions, the Commission has referred to the ATC3 level as the starting point for defining the relevant product market. However, in a number of cases, the Commission found that the ATC3 level classification did not yield the appropriate market definition within the meaning of the Commission Notice on the Definition of the Relevant Market.14 Indeed, the overlap in therapeutic uses does not necessarily imply any particular economic substitution patterns between products. As a result, where appropriate and based on the factual evidence collected during the market investigation, the Commission defined the relevant product market at the level of the molecule.15

(13) In the present case, given the characteristics of the products involved (typically mature genericised medicines), the Commission takes the molecule level as the most plausible starting point for the product market definition, considering that a generic molecule is the closest substitute to the generic medicinal product based on the same molecule or API.16 Neither the Notifying Party nor the market investigation provided any indications that the Commission should depart from this approach.

(14) Furthermore, as the Commission has previously acknowledged, medicines are differentiated not only by their API(s), but also, in particular, as recognized by the European regulatory framework for medicines for human use,17 by their dosage, pharmaceutical form and route of administration, which may limit their substitutability.

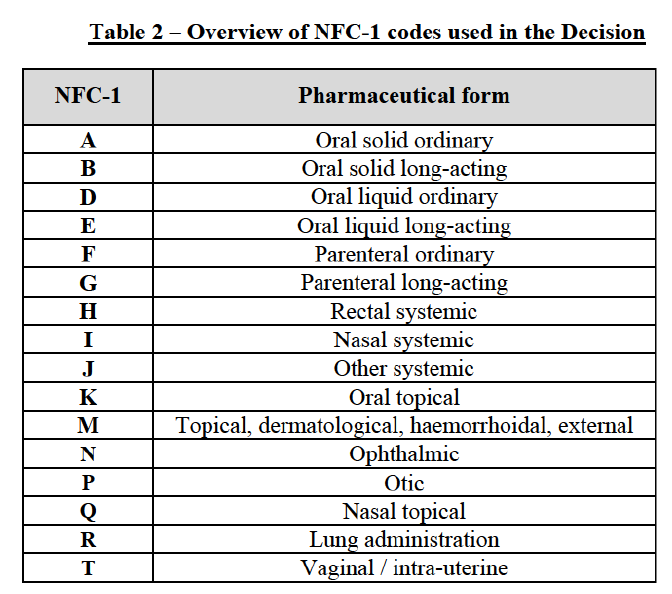

(15) For the purposes of this decision, and in accordance with past practice,18 the Commission has looked whenever appropriate at the pharmaceutical form with reference to the first letter of the typology of form codes (the so-called "New Form Code" or "NFC") used by IMS / EphMRA. In general, the first letter ("NFC-1") differentiates between forms for systemic and topical effect, site of application (e.g. oral, nasal, parenteral or rectal), and long-acting and ordinary forms:

(16) The question whether the molecules analysed in the present decision need to be segmented by pharmaceutical form can be left open for the purposes of the competitive assessment of the Transaction since the Commission analysed all plausible market definitions (molecule and pharmaceutical form levels) where appropriate (i.e. in all cases where the competitive situation was different).

(17) Finally, in certain cases, pharmaceutical products may be further subdivided into various segments on the basis of a variety of criteria, and in particular demand-related criteria. The Commission has, in past decisions,19 defined separate markets for medicines which can be issued only on prescription and those, which can be sold over-the-counter ("OTC", that is non-prescription medicinal products). Medical indications, side effects, legal framework, distribution and marketing tend to differ between these drug categories, even if the active ingredients may be identical.

(18) The question whether the molecules analysed in the present decision need to be segmented between prescription (Rx) drugs and OTC drugs can be left open for the purposes of the competitive assessment of the Transaction since the Commission analysed all plausible market definitions (molecule and Rx/OTC levels) where appropriate (i.e. in all cases where the competitive situation was different).

Geographic market definition

(19) The Notifying Party has, in line with the Commission's prior decisions, submitted an overview of its activities on a country-by-country basis. The Commission has consistently considered that the markets for finished dose pharmaceutical products are national in scope, in particular in view of the national regulatory and reimbursement schemes and the fact that competition between pharmaceutical firms still predominantly takes place at a national level.20 Neither the Notifying Party nor the market investigation provided any indications that the Commission should depart from this approach.

IV.2.1.1.b. Pipeline generic pharmaceuticals

Product market definition

(20) Following the same approach as marketed generic pharmaceuticals and in line with past decisions,21 the Commission takes the molecule level as the most plausible relevant market for pipeline generic pharmaceuticals, considering that a pipeline generic molecule is typically the closest substitute to the other generic medicinal product based on the same molecule. Neither the Notifying Party nor the market investigation provided any indications that the Commission should depart from this approach.

(21) The question whether the pipeline molecules analysed in the present decision need to be segmented by pharmaceutical form or between prescription drugs and OTC drugs can be left open for the purposes of the competitive assessment of the Transaction since the Commission analysed all plausible market definitions where appropriate.

Geographic market definition

(22) For pipeline products, the Commission previously considered that the geographic scope of the relevant market is at least EEA-wide.22 Neither the Notifying Party nor the market investigation provided any indications that the Commission should depart from this approach.

IV.2.1.1.c. Originator pharmaceuticals

(23) The Parties identified two instances where one party (Allergan Generics) is planning to launch in the EEA the generic equivalent of the other party's (Teva) originator drug.23 This concerns the launch of the generic versions of glatiramer acetate (sold by Teva under the brand name "Copaxone") and rasagiline (sold by Teva under the brand name "Azilect").24

Product market definition

(24) In previous decisions,25 the Commission found that generic companies are usually developing a number of pipeline generic drugs which are intended to compete with originators which lose exclusivity (after expiry of patent and/or data exclusivity protections). The Commission concluded that the potential for these products to enter into competition with other products which are either on the market or at the development stage should be assessed by reference to their characteristics, intended therapeutic use, and expected therapeutic and economic substitutability.

(25) The exact scope of the product market (including or not other molecules with the same therapeutic indications) can be left open for the purposes of the competitive assessment of the Transaction since the competitive assessment will not change under any plausible product market segmentation.

Geographic market definition

(26) The approach laid out in section IV.2.1.1.a and section IV.2.1.1.b regarding marketed and pipeline generic products applies mutatis mutandis to glatiramer acetate and rasagiline.

(27) Therefore, the geographic market for pipeline generics should be defined as at least EEA-wide, while the market for marketed products should be defined at national level.

IV.2.1.2. Wholesale of pharmaceuticals

IV.2.1.2.a. Product market definition

(28) The wholesale of pharmaceuticals consists in selling a range of FDPs to customers, including pharmacies, dispensing doctors and hospitals.

(29) The Commission has previously defined a market for the wholesale of pharmaceuticals in some EEA countries.26 In previous decisions,27 the Commission has also considered a market for pre-wholesale services (including 3PLs),28 that is separate of the market for wholesale of pharmaceuticals.

(30) As to wholesale of pharmaceuticals, the Commission has previously considered three possible segmentations, based on the following categories:29

a. Categories of products (depending on whether the medicine may be sold with prescription or OTC; whether it is an originator, generic or parallel import medicine; and whether the medicine may be sold in retail pharmacies under the supervision of a pharmacist only, or also in other outlets such as supermarkets);

b. Categories of wholesalers (broad-line wholesalers30 and short-line wholesalers);31

c. Categories of customers (retail pharmacies, dispensing doctors32 and hospitals) due

to different purchasing and delivery patterns.33

(31) As acknowledged in previous Commission decisions,34 generic manufacturers can sell their products (i) indirectly through wholesalers or, (ii) directly to pharmacies and institutional customers (such as hospitals). In the latter case, pharmacies place orders to the generic manufacturer. Pharmacists may ask that the generics be provided through their wholesaler of choice, in which case the latter acts as a mere logistics provider (3PL).35 Given that the commercial terms are negotiated directly between the generic manufacturer and the pharmacy, such orders are considered as Direct-to-Pharmacy ("DTP") orders.

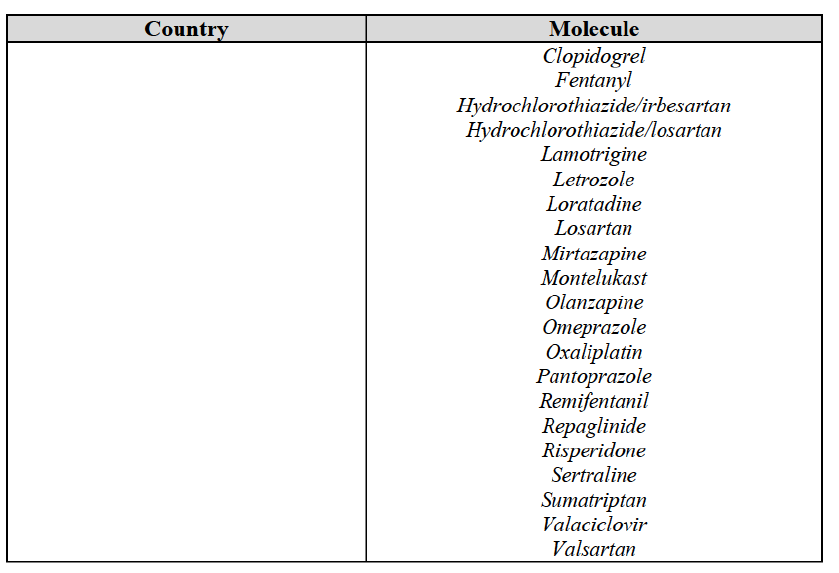

(32) In the present case, in some EEA countries, Teva and Allergan Generics are active as manufacturers selling directly generic pharmaceuticals to customers, through the DTP model.

(33) The market features however differ depending on the EEA country. For instance:

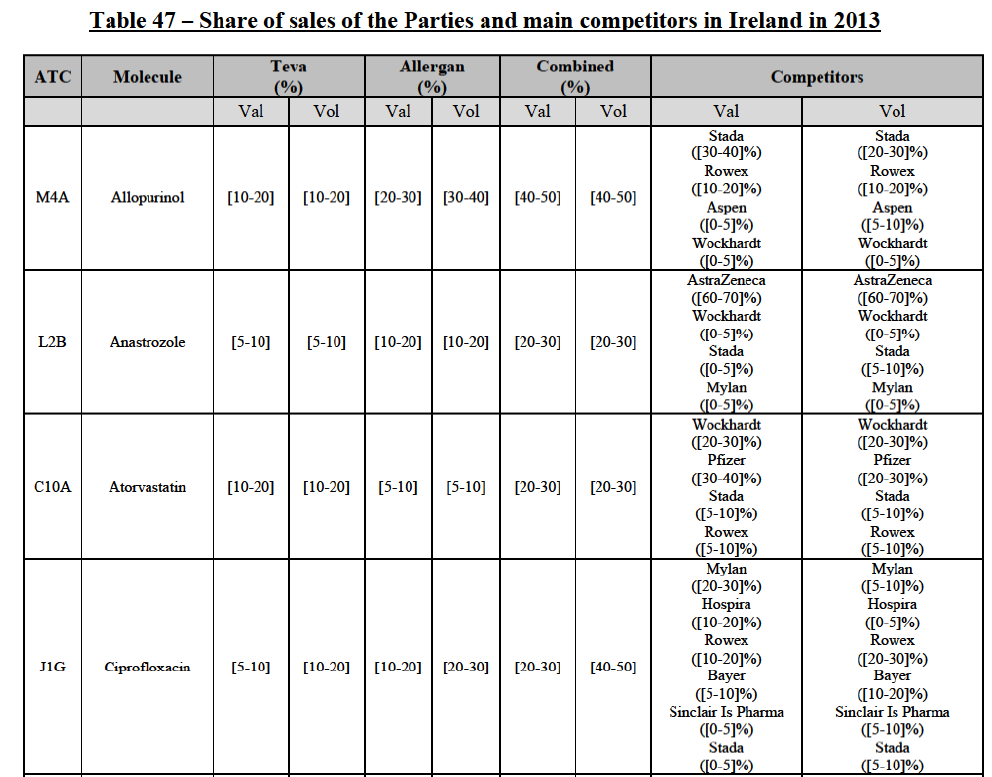

a. in Iceland, Allergan Generics is the only generic manufacturer selling generics directly to customers and it competes with wholesalers selling generics of other manufacturers (such as Lyfis for Teva; Teva does not run a DTP model);

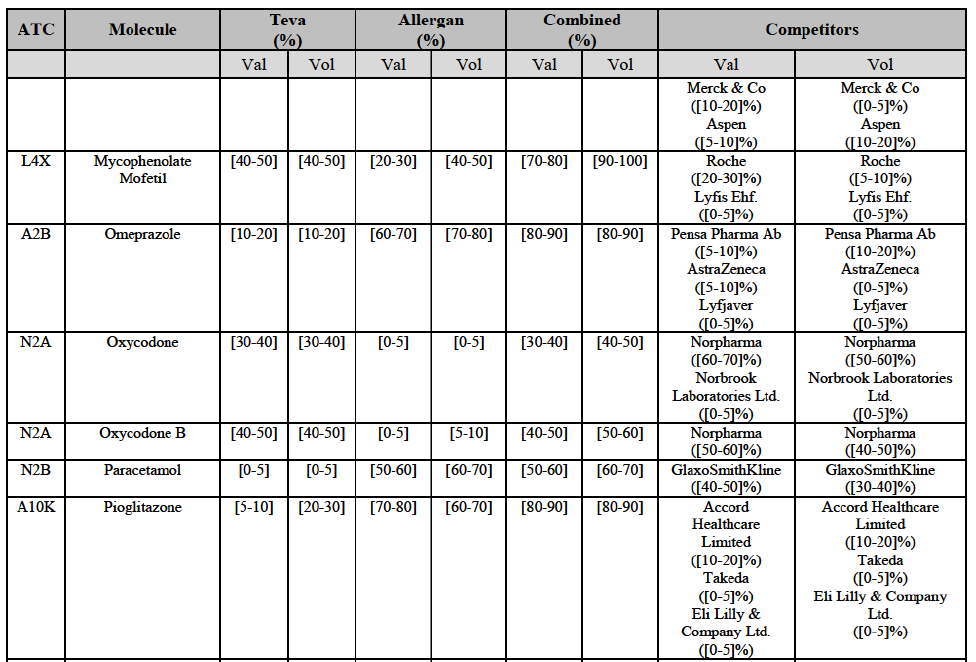

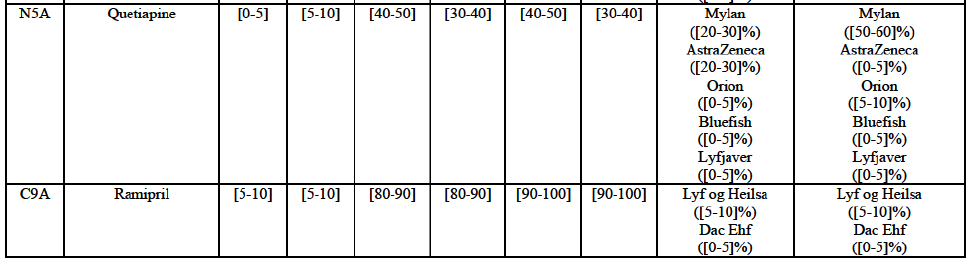

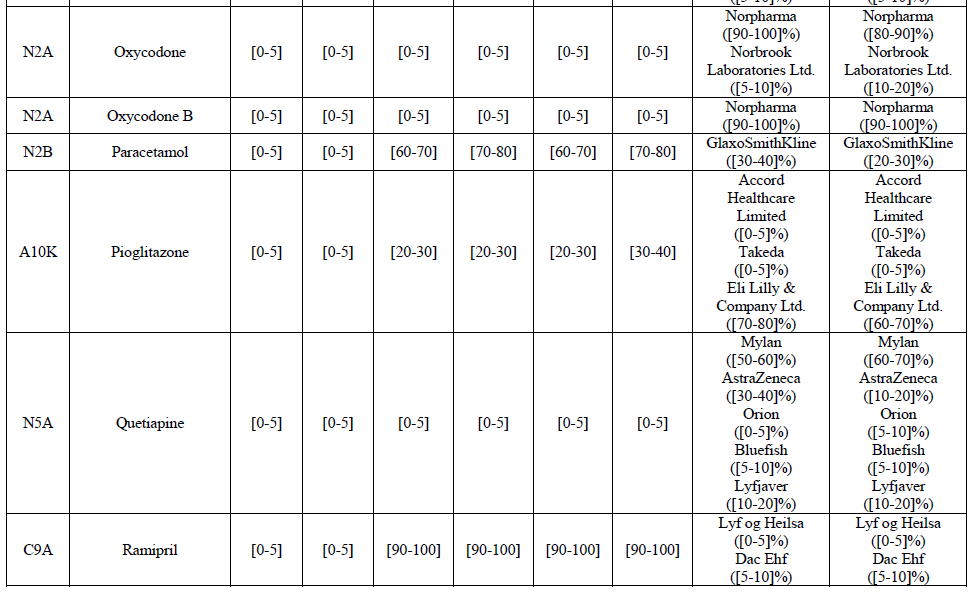

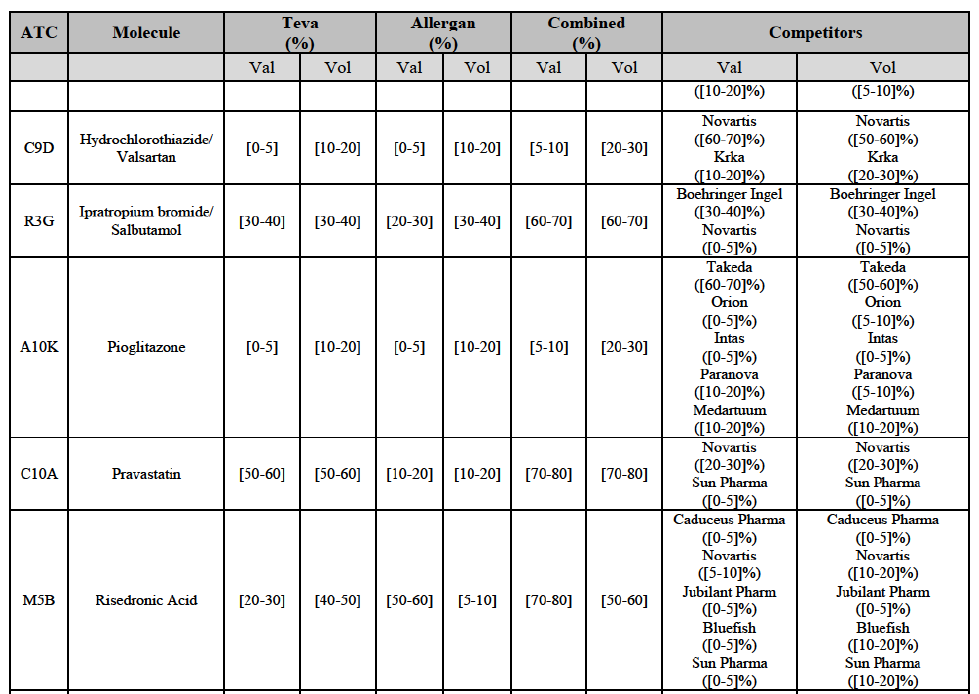

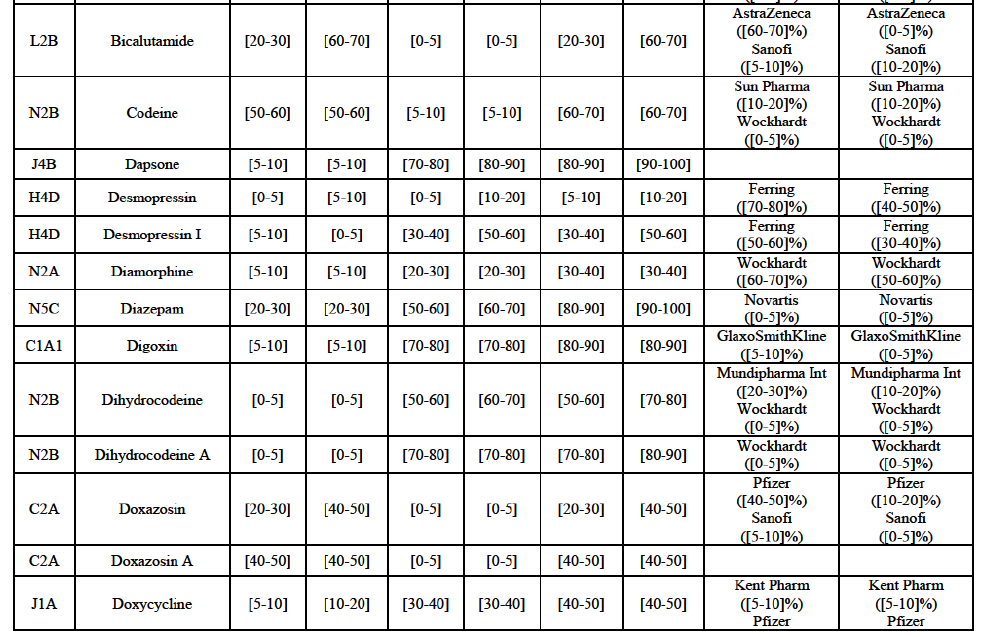

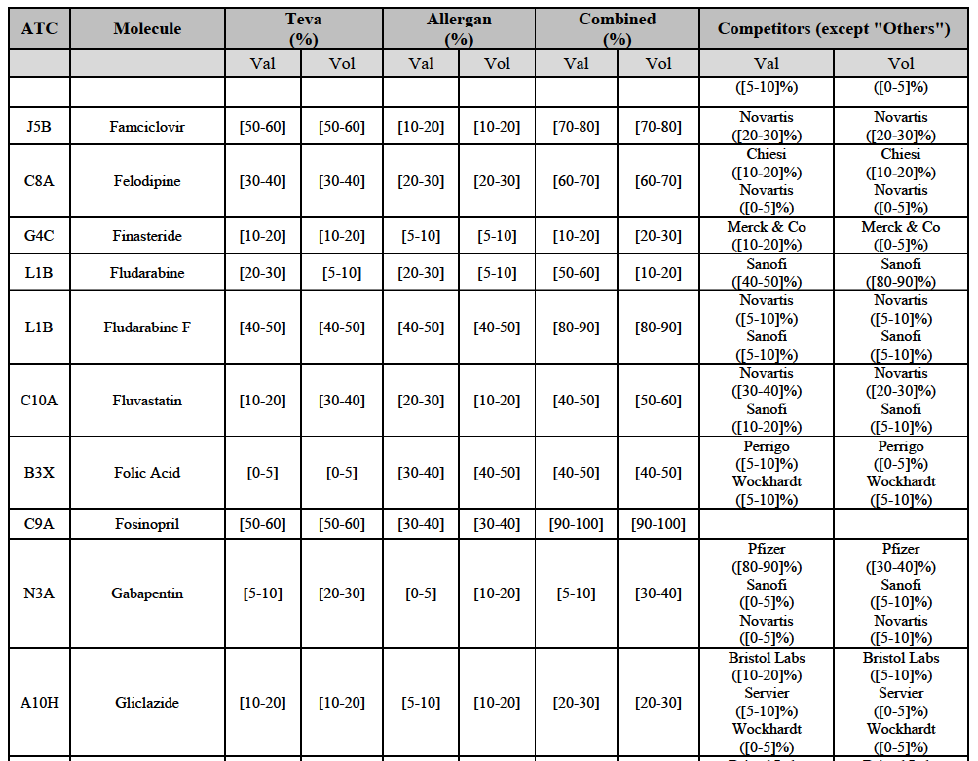

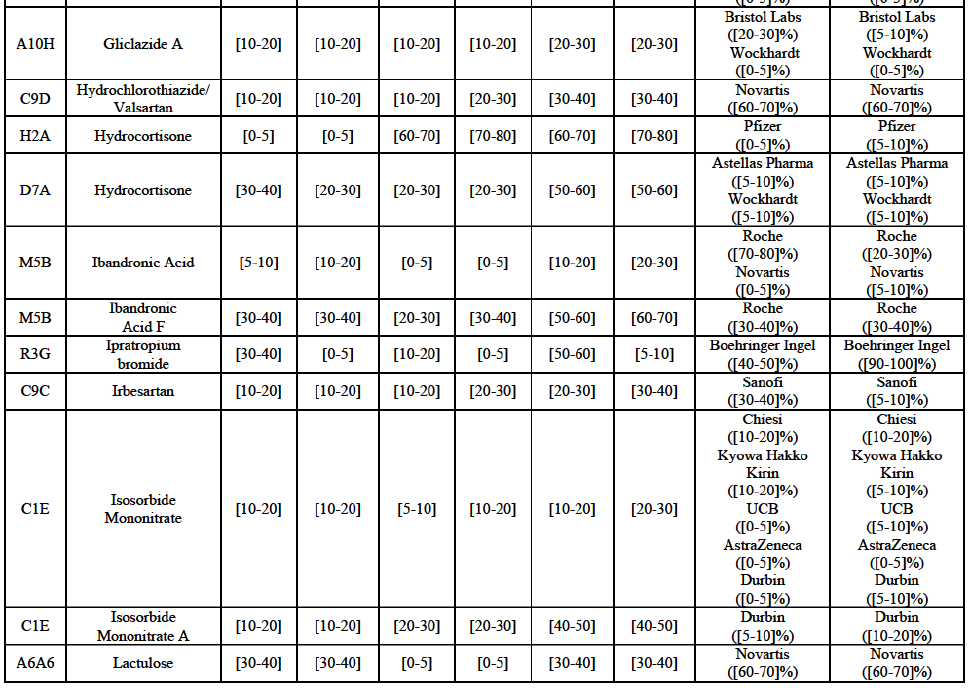

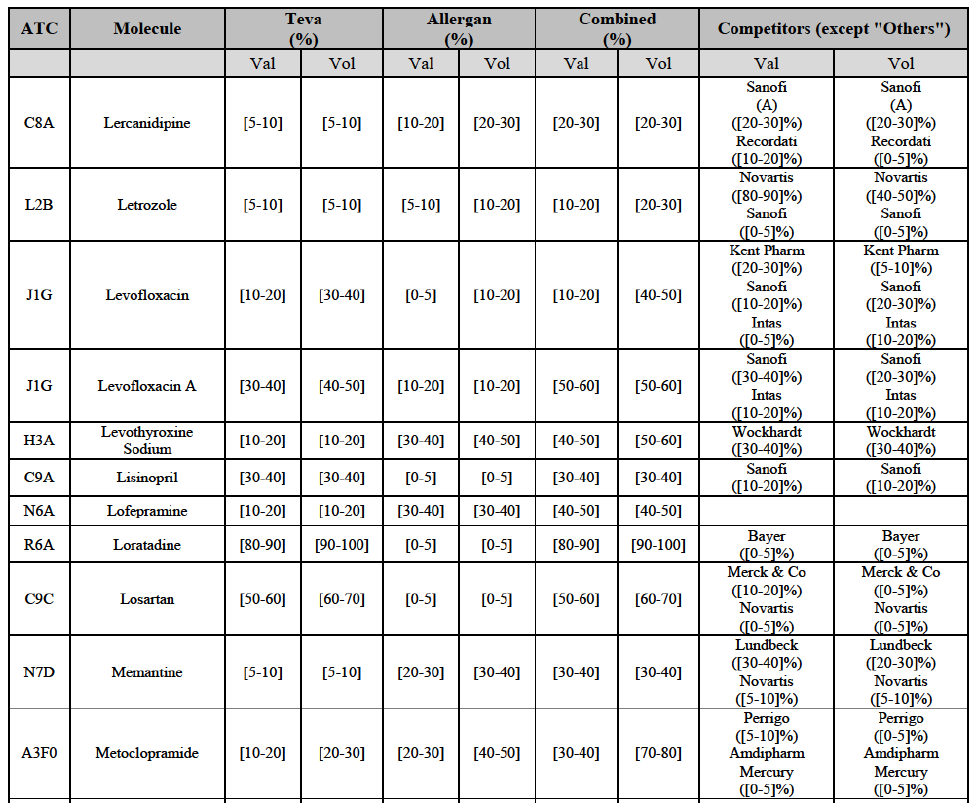

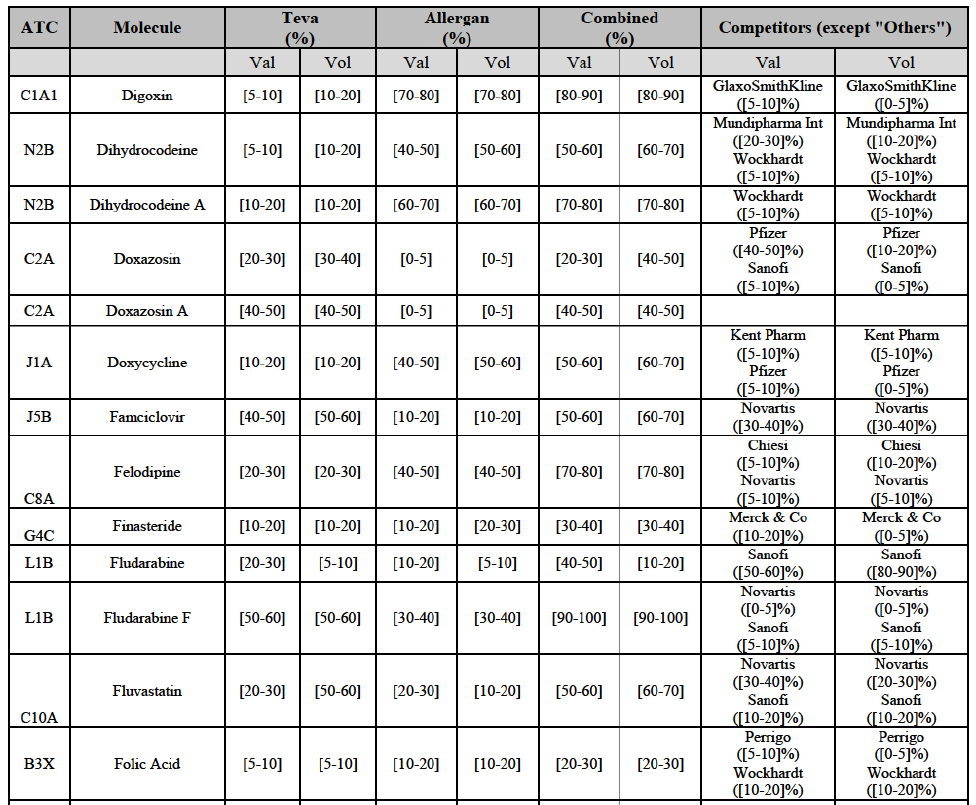

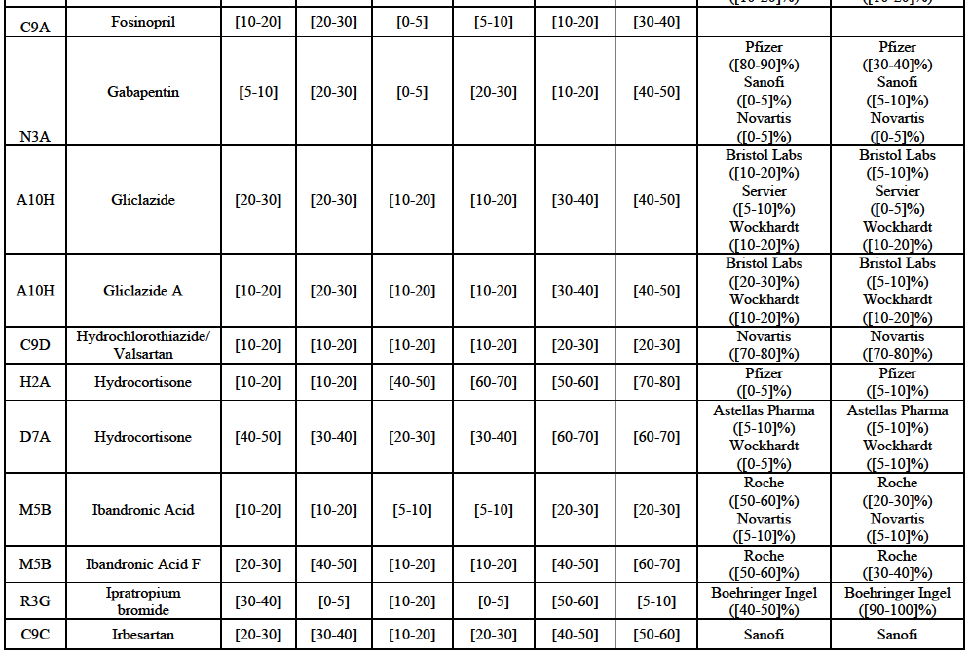

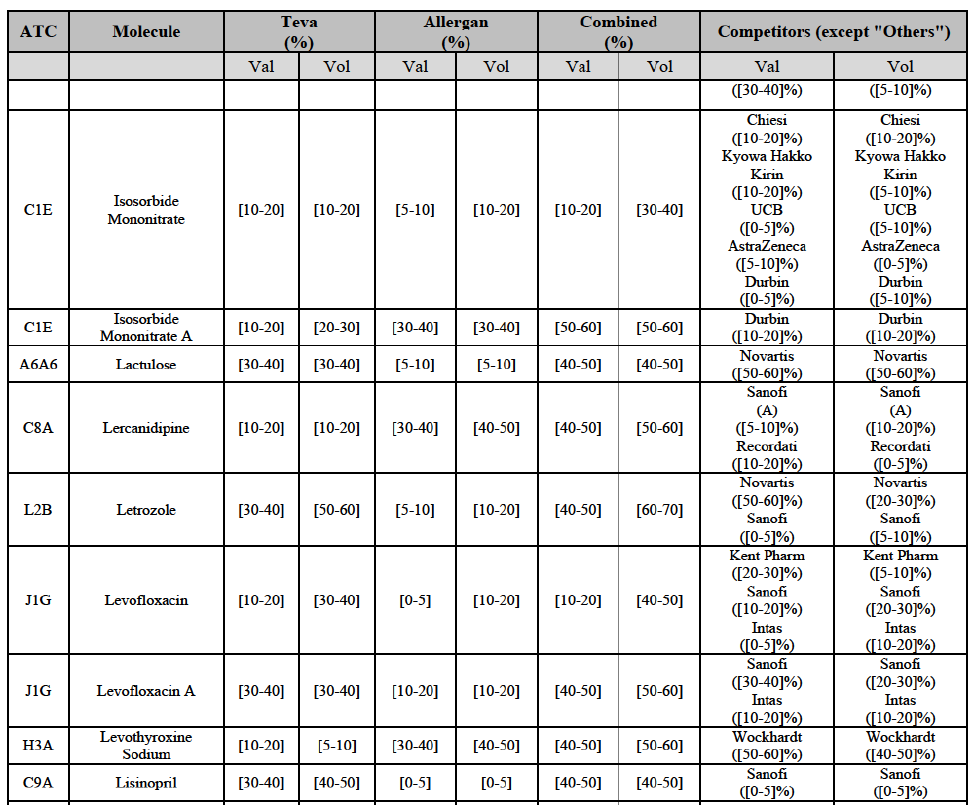

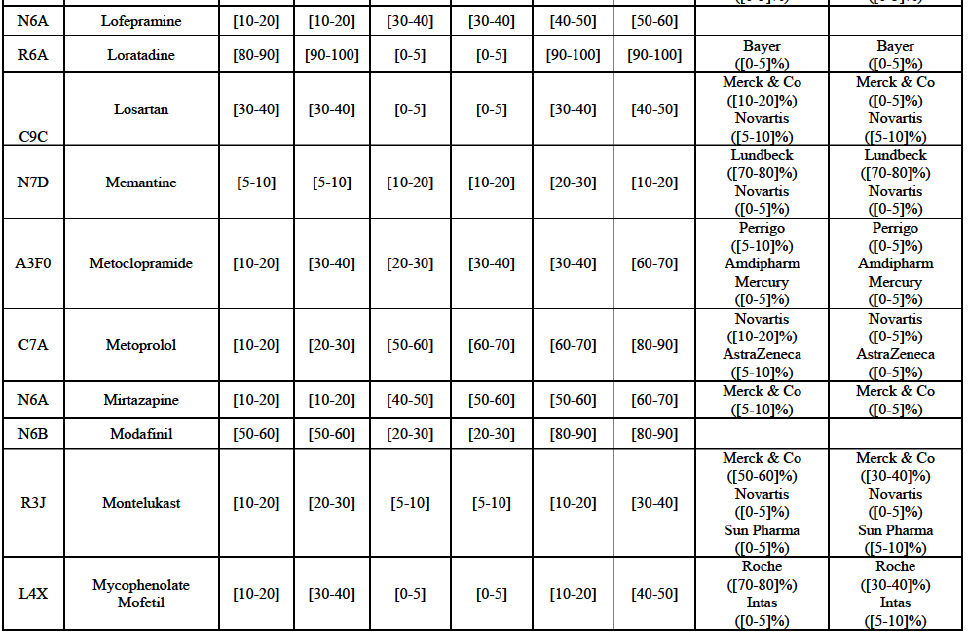

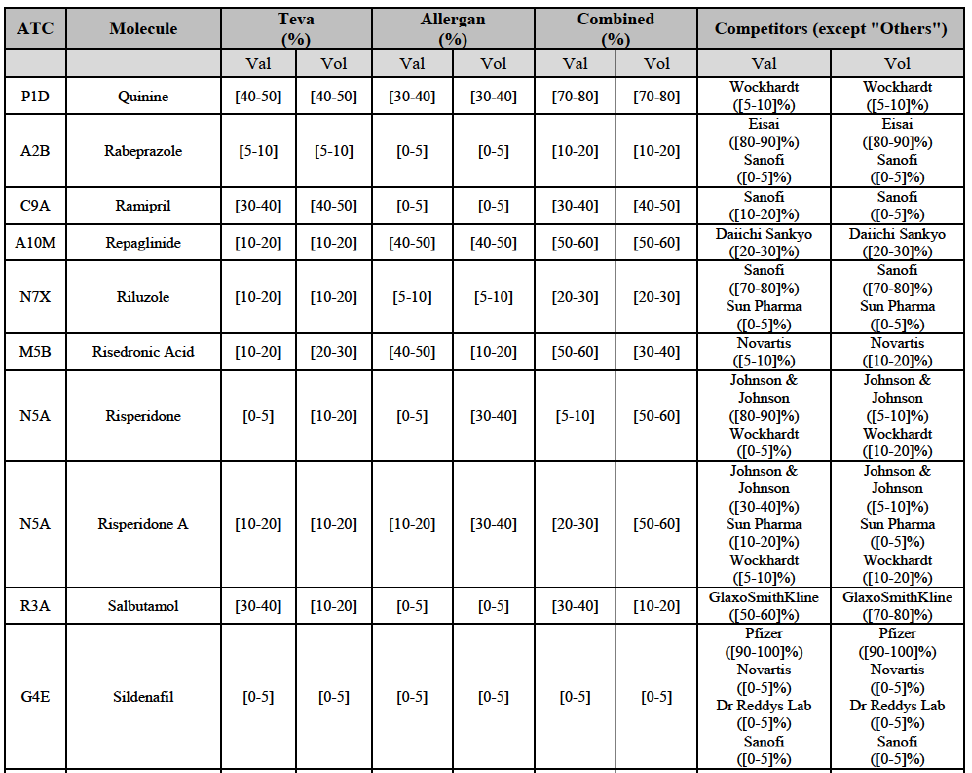

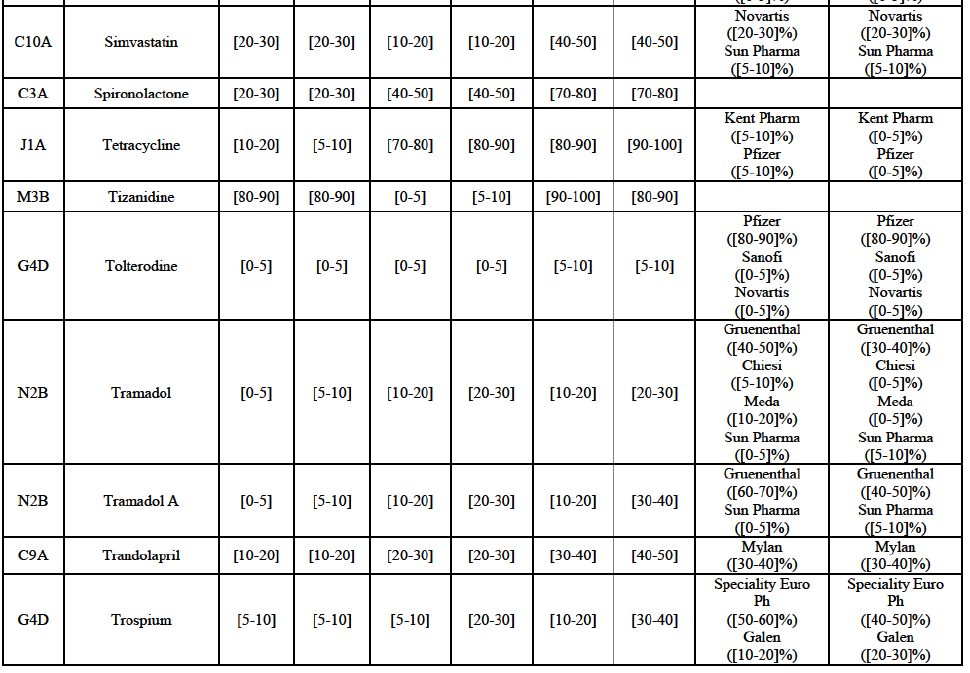

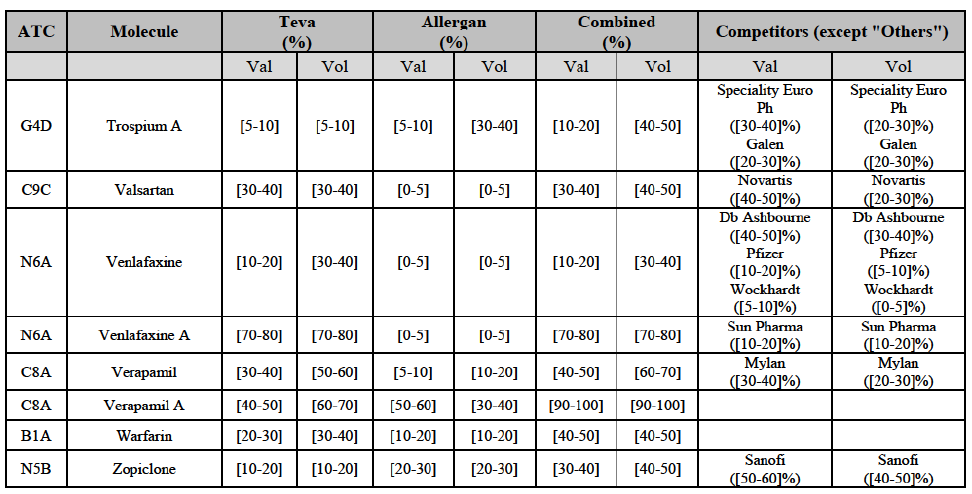

b. in Ireland, large generic manufacturers sell their products directly to customers (that is, they all use the DTP model), using wholesalers or 3PL as logistic providers). This appears to be a change following a major legislative change in 2013 impacting prices of generics in Ireland;36

c. in the United Kingdom, Teva and Allergan Generics are the only manufacturers with a DTP model, using wholesalers as logistic providers. They compete against wholesalers for the sale of FDP. At the same time, they also supply their products to wholesalers (just as other generic manufacturers do), while wholesalers purchase (and take title to) FDPs from generics manufacturers.

The Notifying Party's views

(34) The Notifying Party did not submit any views as to the market for the wholesale of pharmaceuticals and its possible segmentation(s) in general.

(35) However, the Notifying Party submitted that, in Ireland, since all manufacturers are supplying pharmacies directly, using wholesalers as distributors, it remains unclear how competition can occur simultaneously on a product-per-product basis37 and on a portfolio basis.38

The Commission's assessment

Distinction by category of product

(36) Pharmaceuticals include originator and generic products. While a given originator medicinal product typically has a single source of supply (typically the patent holder or its designee if the product is patented),39 a given generic medicinal product can often be sourced from several suppliers which offer medicinal products based on the same molecule. The number of generic suppliers typically depends on the product and on the country, and can be limited for instance for products that are difficult to manufacture or in case their manufacturing technology is protected by process patents.

(37) The market investigation indicated that the price regulation, purchasing patterns and competitive landscape differ between the sale of originator pharmaceuticals that benefit from exclusivity, on the one hand, and of originator pharmaceuticals that have lost exclusivity and generic pharmaceuticals, on the other hand.40 Indeed, there is direct competition on prices between all versions of a given off-patent molecule (including generics and the off-patent originator product).41 This competition can take place, depending on the country, in a free pricing environment, below a price ceiling set by regulatory authorities or through public tenders. This direct competition on prices, which has an impact on the purchasing patterns of customers (through comparison of price lists, tenders, etc.), does not exist for an originator pharmaceutical (except with parallel imports).

(38) In addition to competition through prices for each product separately, the market investigation indicated that some purchasing practices are specific to the purchase of generics. For instance, pharmacies tend to procure their generics through a limited number of suppliers.42 In some EEA countries, manufacturers and wholesalers selling a sufficiently large range of different generics have developed schemes with discounts to pharmacies based on a customer's overall generics spend.43 Furthermore, there are also elements of non-price competition. For instance, customers also adopt so-called cascade mechanisms for their generics purchases, establishing an ordered list of alternative generic suppliers in case of shortages (naturally, this mechanism cannot be replicated for originator pharmaceuticals, given that typically there is only a single source of supply).44

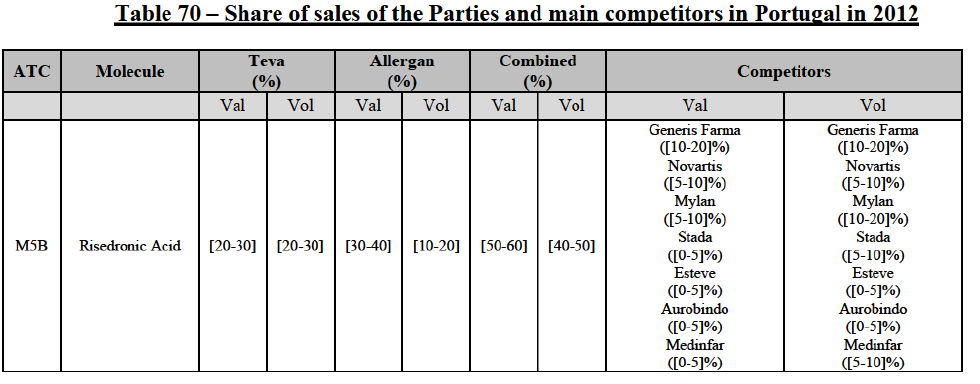

(39) As to the competitive landscape, the majority of pharmaceutical companies are either specialised in generic or originator pharmaceuticals. While certain players own both an originator business and a generics business (e.g. Teva itself, Novartis, Sanofi, Pfizer), they typically operate as very distinct business units. Teva for instance distinguishes between its Global Specialty Medicines business, for originator products, and Global Generic Medicines business, for generics. Finally, certain wholesalers (in particular short-line) can be specialised in generics.45

(40) For the purpose of the competitive assessment of the Transaction, the Commission considers that there is a separate market for the wholesale of generic pharmaceuticals.

Distinction by type of suppliers

General approach

(41) In previous cases,46 the Commission distinguished broad-line wholesalers from short-line wholesalers. The Commission noted that short-line wholesalers focus on a limited range of products, generally high volume products, and supply pharmacies with a less frequent delivery schedule.

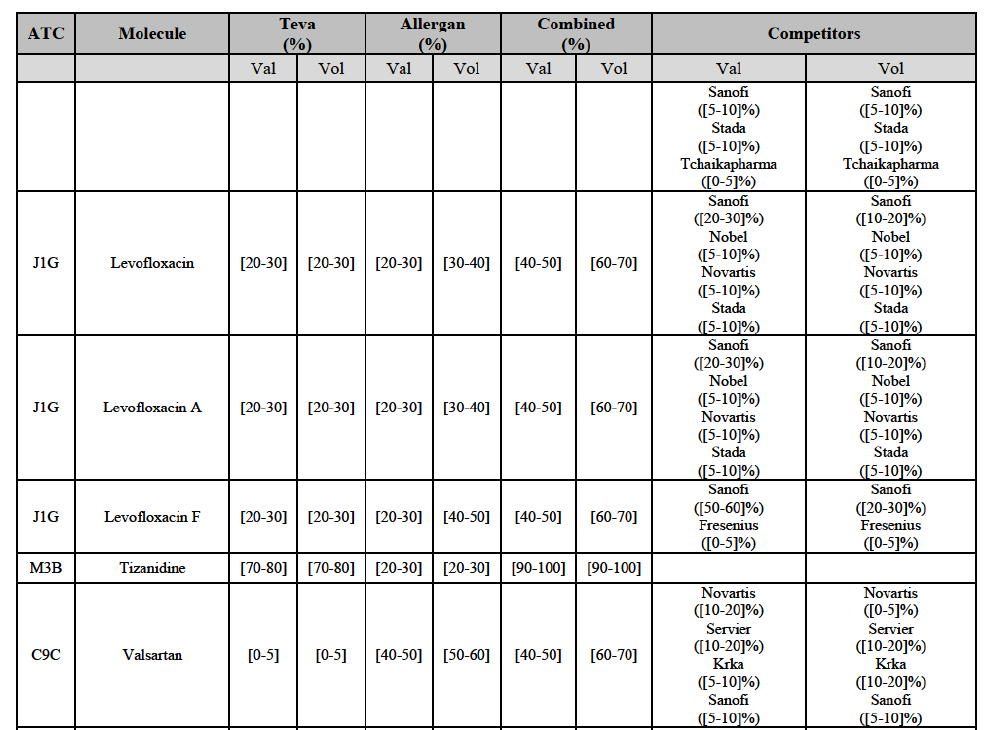

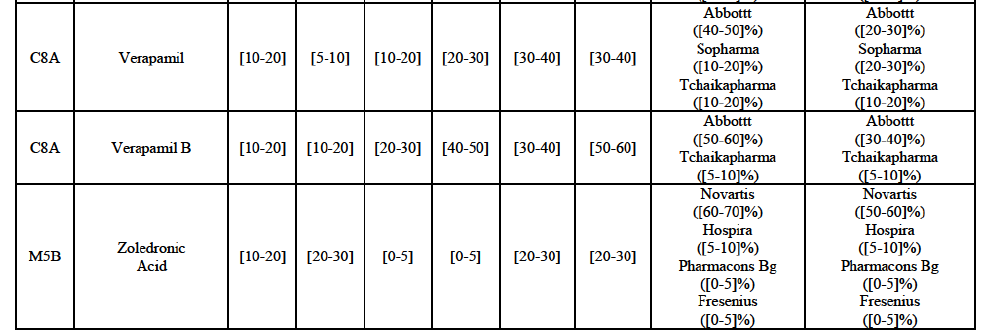

(42) When generic manufacturers develop DTP sales channels, they engage in direct competition with wholesalers and can be considered as vertically integrated companies, competing with wholesalers on the market for the wholesale of generic pharmaceuticals to pharmacies, and, if they also sell generics to wholesalers, with other suppliers in the market for the marketing of generic pharmaceuticals where wholesalers are the customers.

(43) The market investigation further indicated that broad-line wholesalers and manufacturers selling a sufficiently broad range of generics and offering the same level of services would address pharmacies' needs in a similar way and thus could be part of the same relevant market for the wholesale of generic pharmaceuticals. Conversely, manufacturers selling a smaller range of generics or distributing generics on a less frequent basis would not belong to that market.

Specific situation of Ireland

(44) As indicated by the Parties, in Ireland, currently the wholesale of generic pharmaceuticals to pharmacies appears to be mostly done by manufacturers selling directly a wide range of generics to pharmacies. Therefore, the question arises as to whether the Parties can be considered as being active both in the wholesale market for generic pharmaceuticals in Ireland (without wholesalers being present) and in the markets for the marketing of individual molecules.

(45) In accordance with the previous practice of the Commission discussed above, the Irish Competition Authority, notably in its 2013 decision Uniphar/CMR,47 defined a market for the wholesale of pharmaceuticals in Ireland, where broad line wholesalers, short line wholesalers and manufacturers selling directly to pharmacies (DTP sales)48 would be active and would each be part of a separate segment due to the different range of products and services they would offer.

(46) For the wholesale of generics, the market investigation provided indications that, following a legislative change in 2013 impacting prices of generics in Ireland,49 wholesalers would now rather act as logistic providers for generics manufacturers, the latter selling their products directly to pharmacies.50 In particular, in this context, broad-line wholesalers have recently adopted a fee-per-pack model.51 Therefore, wholesalers no longer seem to materially influence commercial offers to pharmacies. Instead, generics manufacturers, such as Teva and Allergan Generics, sell directly to pharmacies and have developed their own sales and loyalty schemes, but would not compete with wholesalers.

(47) However, contrary to the Party's views, it is not inconsistent to conclude that the Parties compete both on the marketing of individual molecules and on the wholesale of generic pharmaceuticals in Ireland. Indeed, as evidenced by the market investigation and further detailed in the competitive assessment, pharmacies would typically source part of their generic pharmaceutical needs as a purchase of a broad portfolio of molecules from preferred suppliers, and complete these purchases with smaller scale, molecule-by-molecule type of purchases. Generic manufacturers having a broad portfolio of molecules, such as the Parties, compete on the market for wholesale of a wide range of generic molecules to pharmacies against other generic manufacturers of similar scale and offering similar level of services. Meanwhile, as regards the market for marketing of individual generic molecules all generic manufacturers offering the molecule are active, irrespective of their size.52

Conclusion

(48) For the purpose of the competitive assessment of the Transaction, the Commission considers that the segmentation of the market for the wholesale of generic pharmaceuticals by type of suppliers can be left open since the conclusion of the Commission as to whether serious doubts arise or not in the market for the wholesale of generic pharmaceuticals will not change under any plausible product market definition.

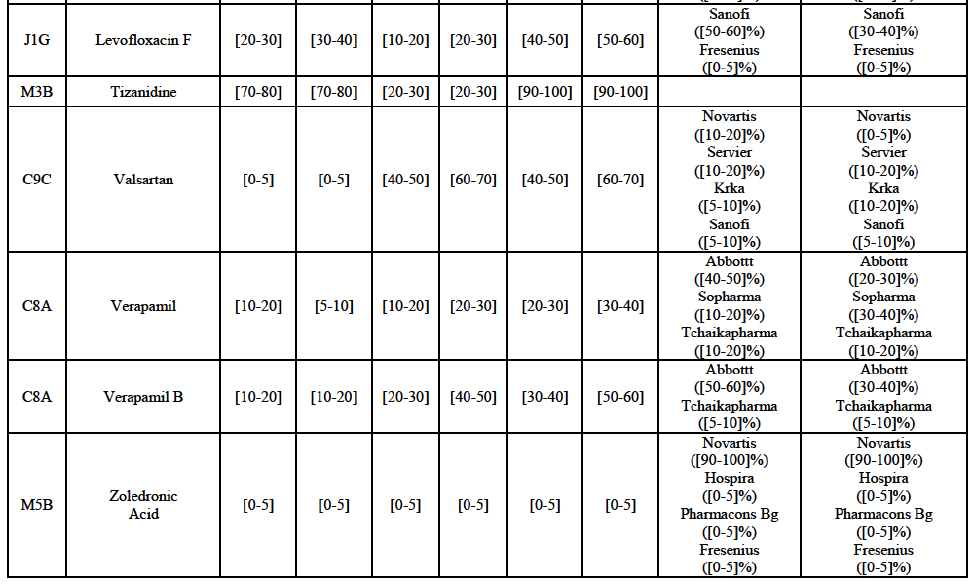

Distinction by category of customers

(49) Finished dose pharmaceuticals can be sold to individual pharmacies and pharmacy chains, dispensing doctors and hospitals.

(50) In previous cases,53 the Commission envisaged a segmentation of the wholesale market of finished dose pharmaceuticals by category of customers, such as retail pharmacies, doctors and hospitals, due to different purchasing and delivery patterns.

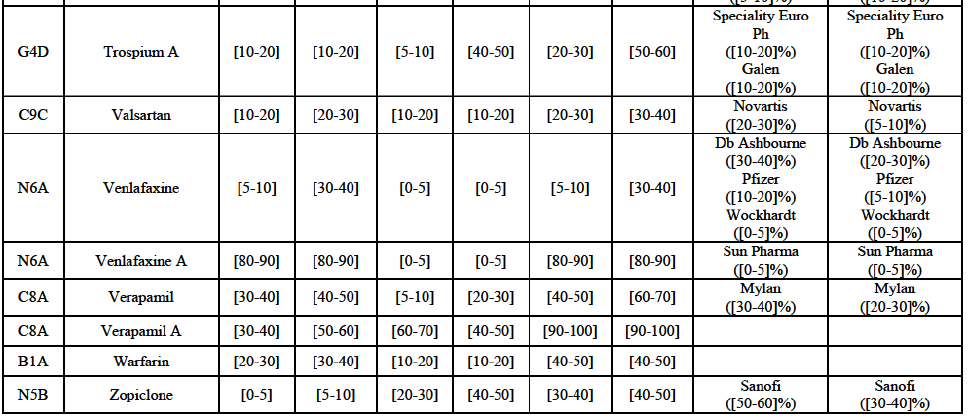

(51) The market investigation confirmed that purchasing patterns may differ depending on the category of customers. For instance, pharmacy chains which are vertically integrated to a wholesaler would generally purchase generics from the wholesaling arm of the group.54 In a number of EEA countries, hospitals would more frequently use tendering procedures to select its supplier of one specific generic.55 Independent pharmacies and pharmacy chains may or may not be part of purchasing groups depending on the country.56

(52) The exact scope of the product market for the wholesale of generic FDPs can be left open for the purposes of the competitive assessment of the Transaction since the conclusion of the Commission as to whether serious doubts arise or not in the market for the wholesale of generic finished dose pharmaceuticals will not change under any plausible product market definition.

IV.2.1.2.b. Geographic market definition

(53) In previous decisions,57 the Commission considered that pharmaceutical wholesaling is either national or regional (sub-national) in scope, due to the emphasis placed by customers on the frequency and speed of delivery of medical products.

(54) The market investigation in this case confirmed that the market for the wholesale of generic pharmaceuticals is not larger than national, in view of the existence of national regulatory and reimbursement schemes and purchasing practices and of the fact that competition between pharmaceutical companies still predominantly takes place at a national level.58

(55) The exact scope of the geographic market for the wholesale of generic pharmaceuticals can be left open for the purposes of the competitive assessment of the Transaction since the competitive assessment will not change under any plausible geographic market segmentation.

IV.2.2. Competitive assessment

IV.2.2.1. Introduction

Marketed generic pharmaceuticals

(56) In this case, affected markets were identified under all plausible market definitions, at the level of the molecule (ATC5) and at the level of the pharmaceutical form (NFC-1), with a distinction between prescribed and OTC sales, where relevant.

(57) Given the large number of affected markets in relation to marketed FDPs, and in accordance with past practice,59 the Commission has applied a system of filters aimed at determining the group of markets where concerns are most likely and on which it focused its analysis.

(58) Based on these filters, affected markets in relation to marketed FDPs are analysed according to four categories:

* Group 1: the Parties' combined market share exceeds 35% and the increment exceeds 1%.

* Group 1+: either (a) the Parties' combined market share is below 35%, but only one other competitor remains on the market, or (b) the Parties' combined market share exceeds 35% and the increment is below 1% but the Party with the small increment is a recent entrant.

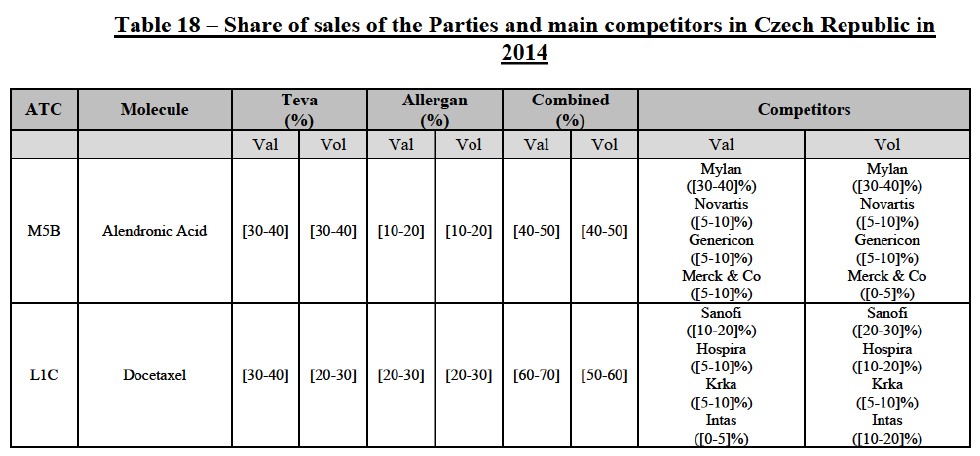

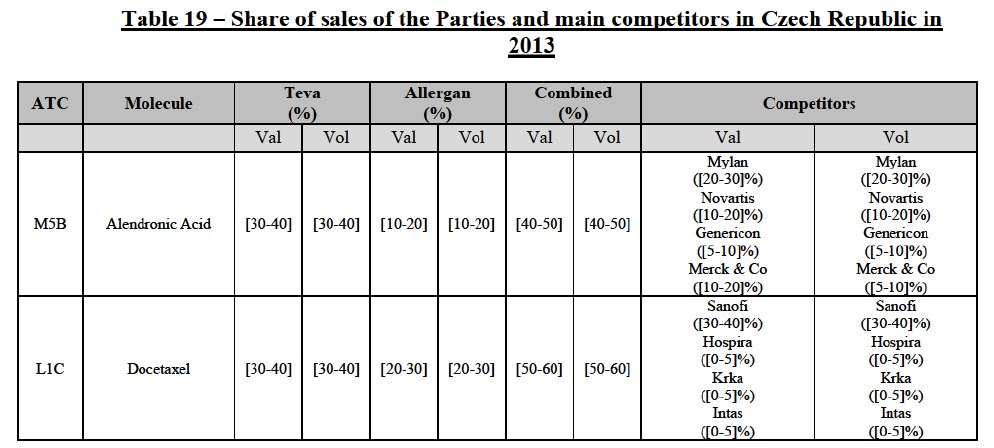

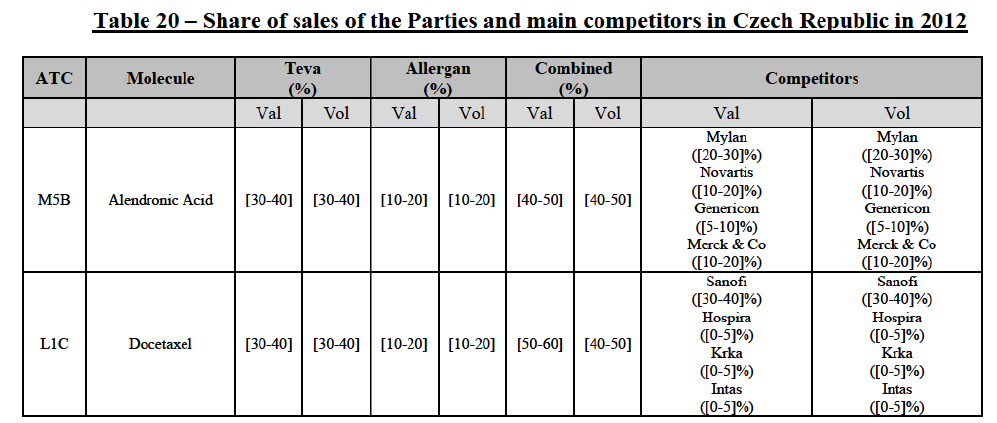

* Group 2: the Parties' combined market share exceeds 35% but the increment is less than 1% (and the Party with the small increment is not a recent entrant).

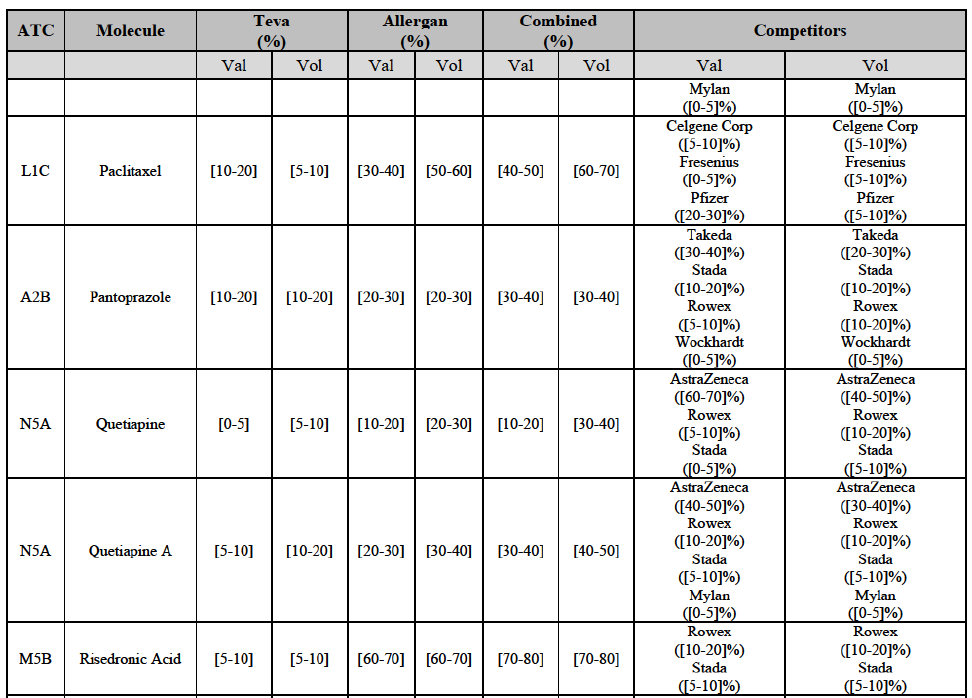

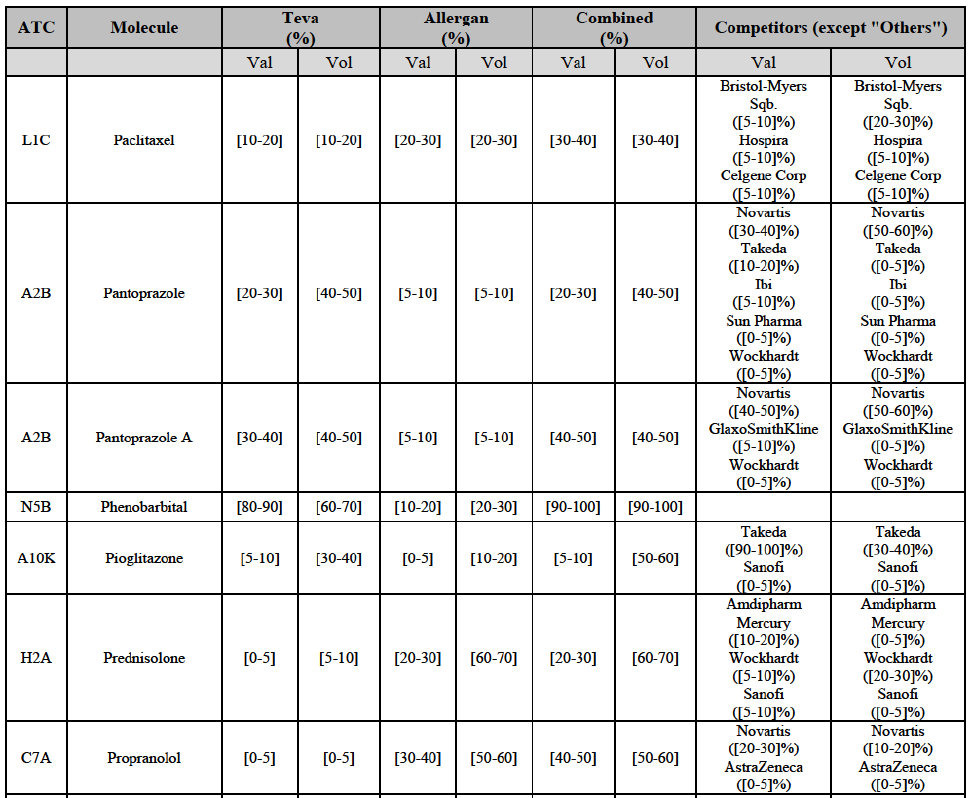

* Group 3: the market is horizontally affected but the Parties' combined market share is less than 35% (and more than one competitor remains on the market).

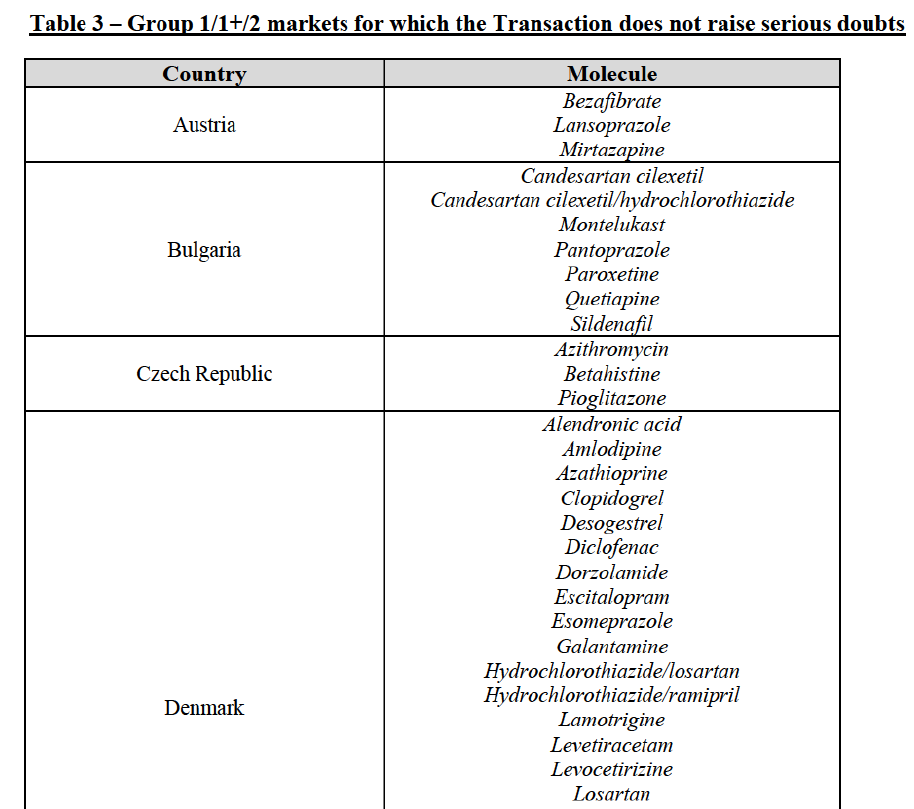

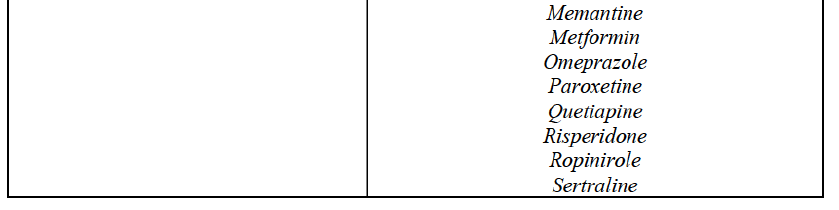

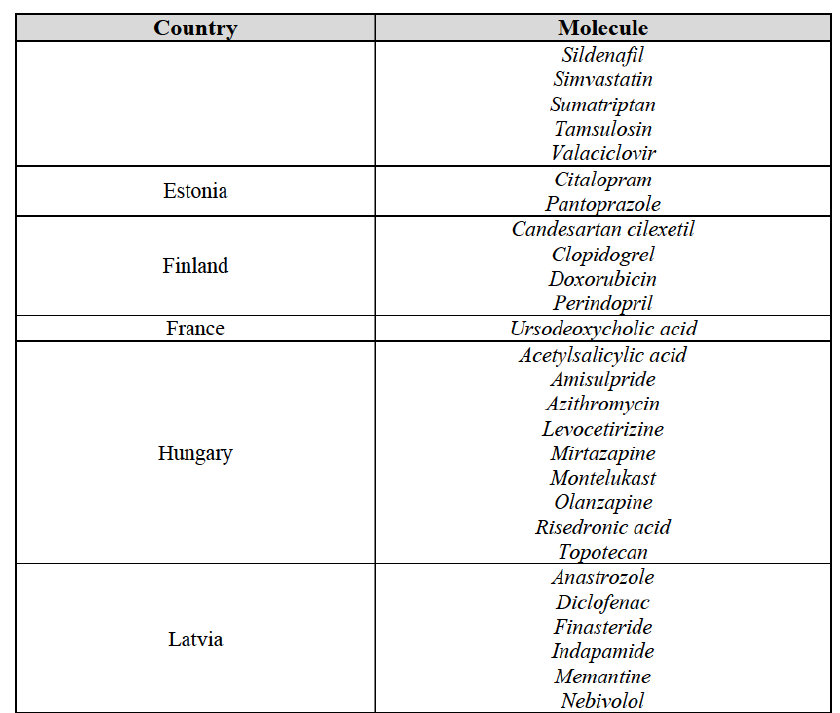

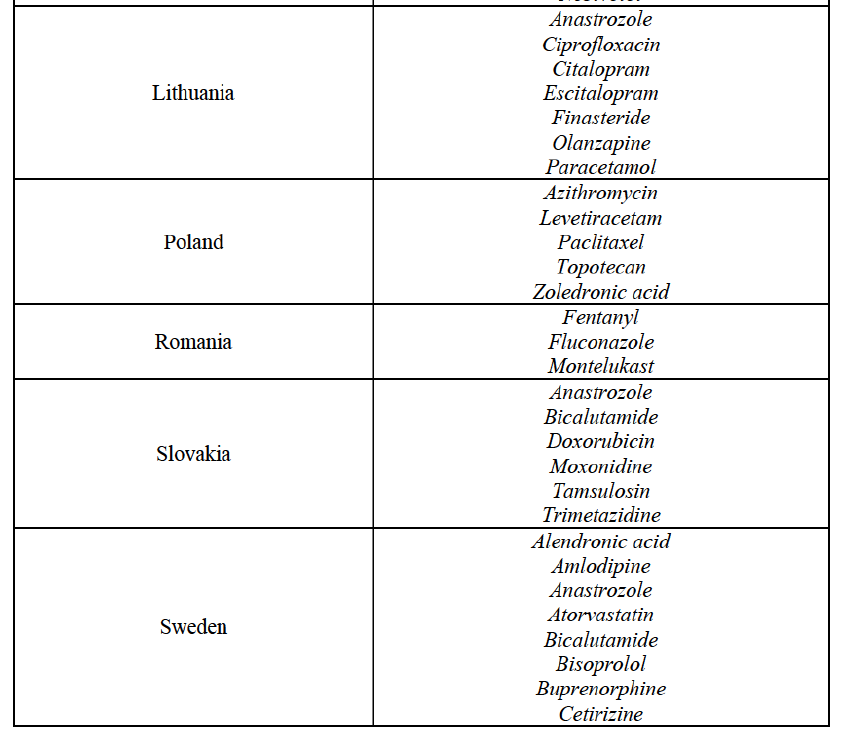

(59) In light in particular of the combined market shares of the Parties and their competitors over the last three years, the date of patent expiry, the recent evolution of prices, the level of complexity of the Parties' products,60 the Parties' pipeline products, as well as replies to the market investigation, the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to all Group 3 markets, as well as the following Group 1/1+/2 markets, under all plausible product market definitions:

(60) The markets with respect to which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market in relation to marketed FDPs are further detailed below for each EEA country under the section "Marketed generic pharmaceuticals".

Pipeline generic pharmaceuticals

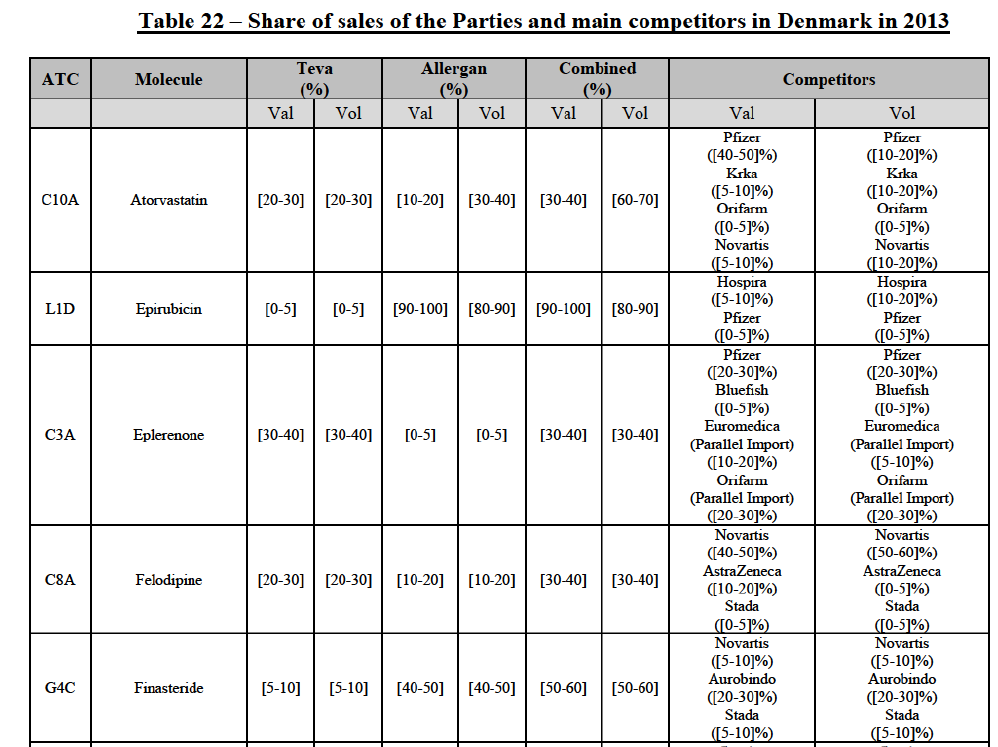

(61) Given the large number of markets in relation to pipeline FDPs, and in accordance with past practice,61 the Commission has applied a system of filters aimed at determining the group of markets where concerns are most likely and on which it focused its analysis.

(62) Based on these filters, markets in relation to pipeline FDPs are analysed according to four categories:

* Pipeline in affected markets: One Party is planning to launch a generic pipeline in a market where both Parties already hold a combined market share in excess of 35% (under all plausible market definitions, including distinction by pharmaceutical form and between Rx and OTC where relevant). For example, in E...], both Parties are active for [...] which is a Group 1 affected market and Allergan Generics has a pipeline for [...J.

* Pipeline-to-marketed affected markets: One Party is planning to launch a generic pipeline in a market where the other Party is the originator or holds a market share in excess of 35% (under all plausible market definitions, including distinction by pharmaceutical form and between Rx and OTC where relevant).

* Pipeline-to-pipeline affected markets: Both Parties are planning to launch a generic pipeline in a market where there is only one or two competitors (including the originator company, this is the case for instance in relation to molecules close to patent expiry).

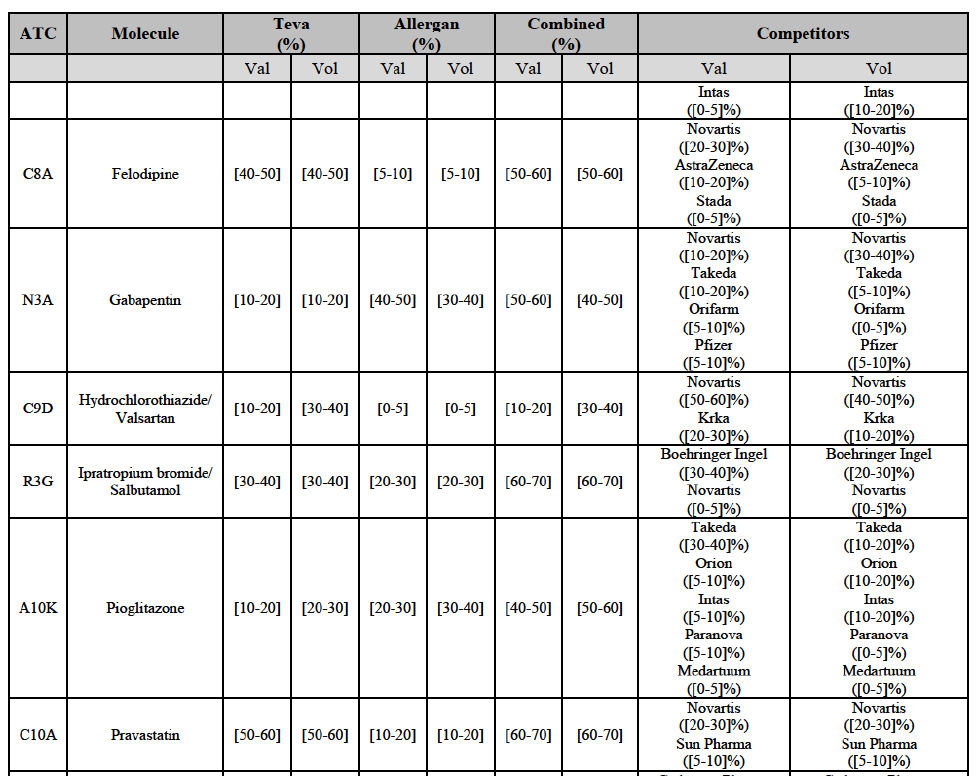

* Originator-to-generic pipeline overlaps: One Party is planning to launch a generic version of a product for which the other Party is the originator. This is the case of Teva's Copaxone (glatiramer acetate) and Azilect (rasagiline), for which Allergan Generics is developing a generic version.

(63) In light, in particular, of the market shares of the in-market Party (pipeline-to-marketed affected markets) and the timing of the entry of pipeline products from competitors (pipeline-to-pipeline affected markets), the Commission considers that the Transaction does not raise serious doubts as to its compatibility with the internal market with respect to the following markets under all plausible product market definitions:

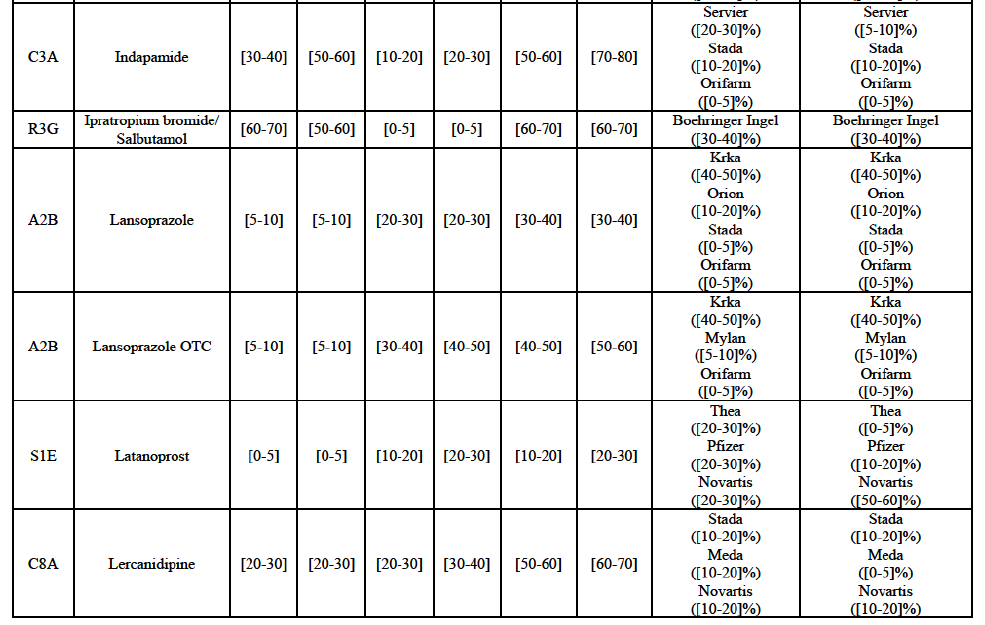

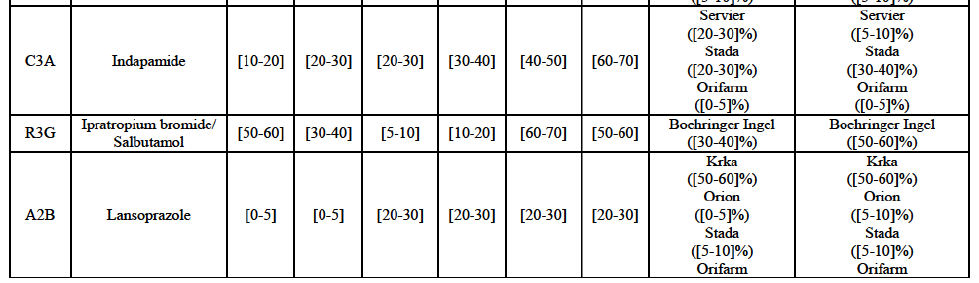

(64) The markets with respect to which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market in relation to pipeline FDPs are further detailed below:

* Pipeline in affected markets: For each EEA country, under the section "Marketed generic pharmaceuticals".

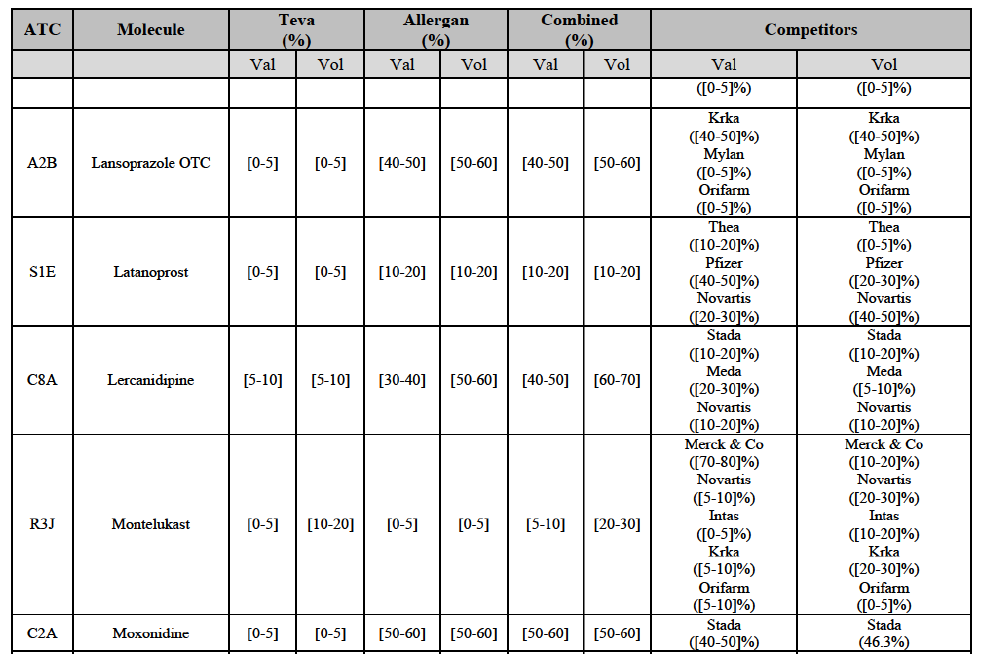

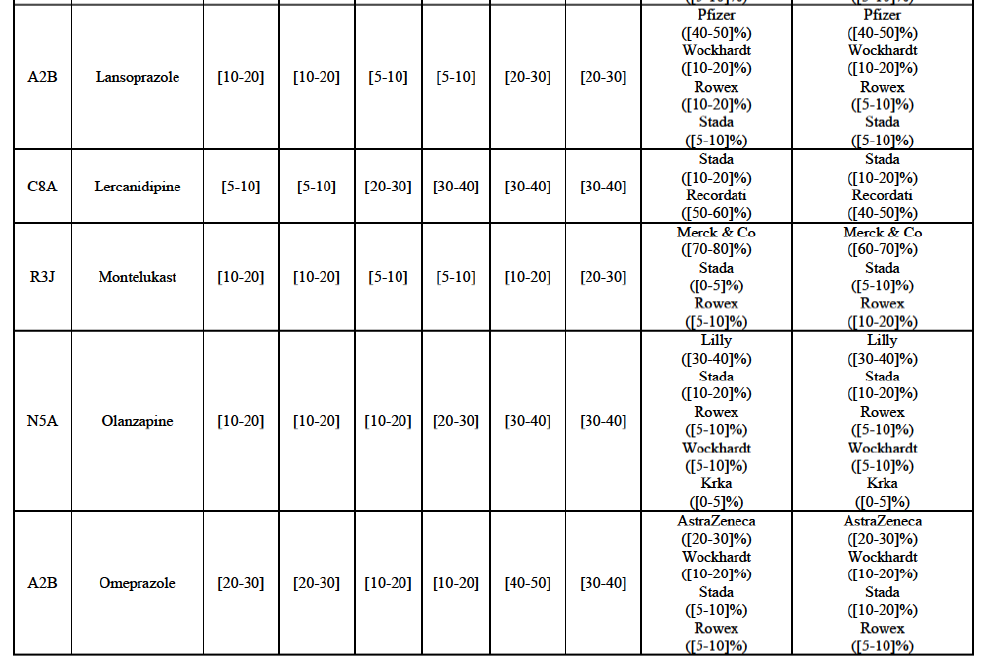

* Pipeline-to-marketed affected markets: For each EEA country, under the section "Pipeline generic pharmaceuticals".

* Pipeline-to-pipeline affected markets: Under section IV.2.2.29, "Pipeline-to-pipeline overlaps ").

* Originator-to-generic pipeline overlaps: Under section IV.2.2.30, "Originator-to-generic pipeline overlaps").

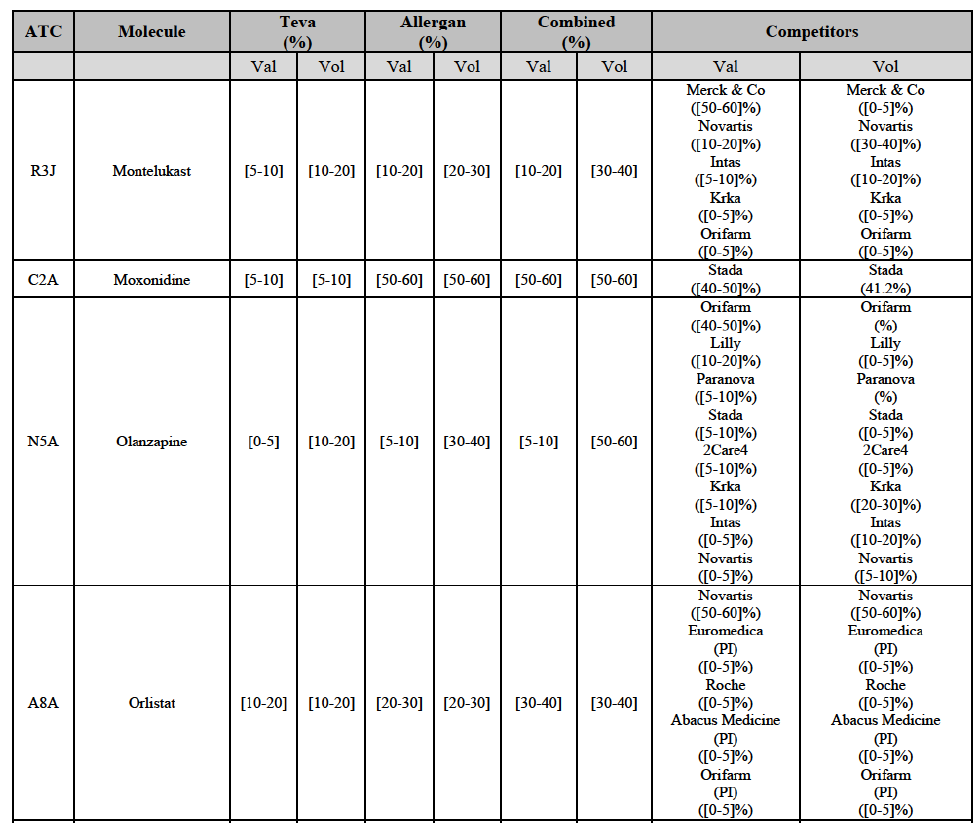

Wholesale of generic pharmaceuticals

(65) The Commission also considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the markets for the wholesale of generic pharmaceuticals in Iceland, Ireland and the United Kingdom. The competitive assessment of the impact of the Transaction on these markets is included in the relevant country sections.

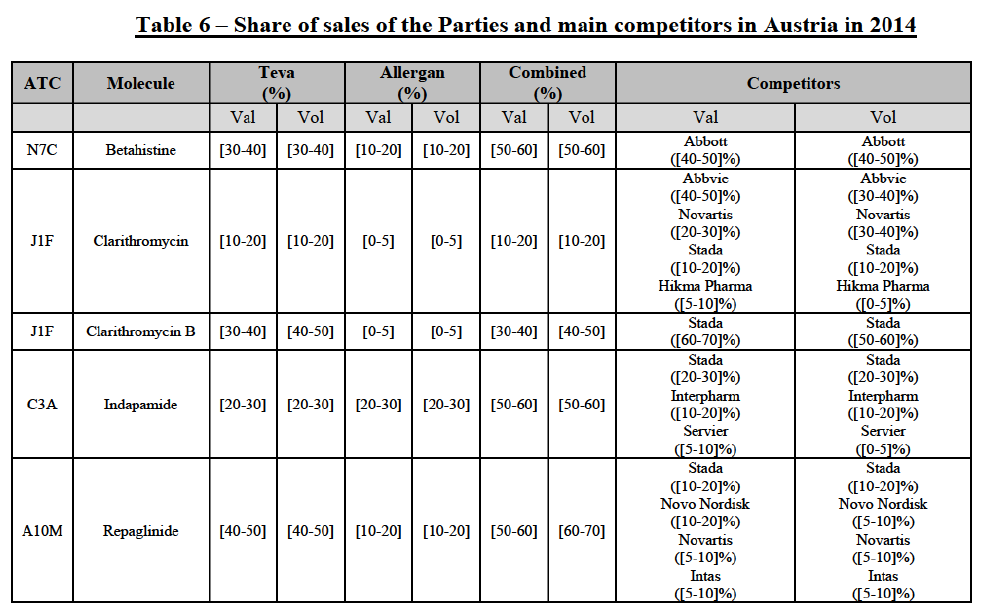

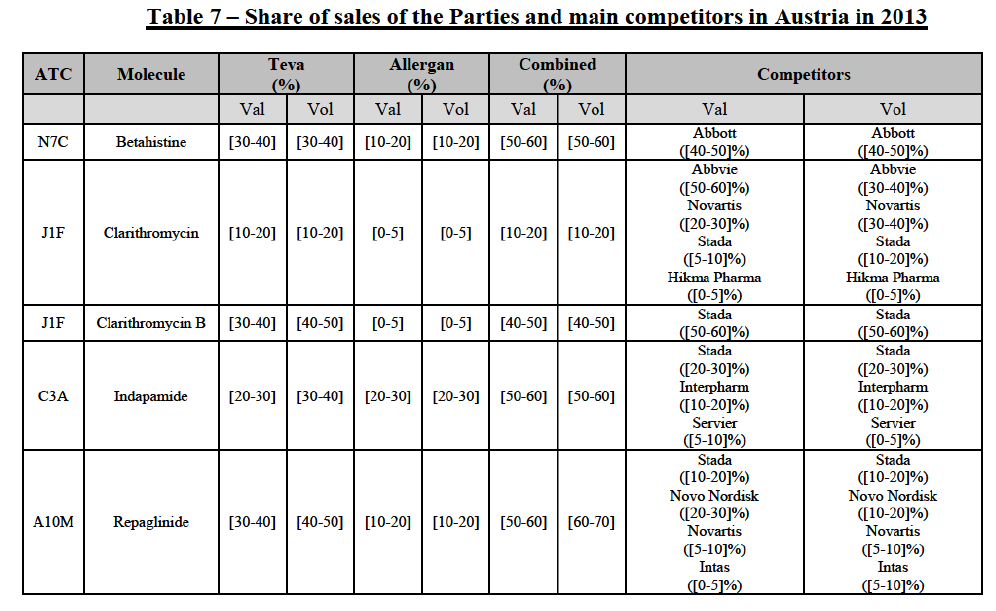

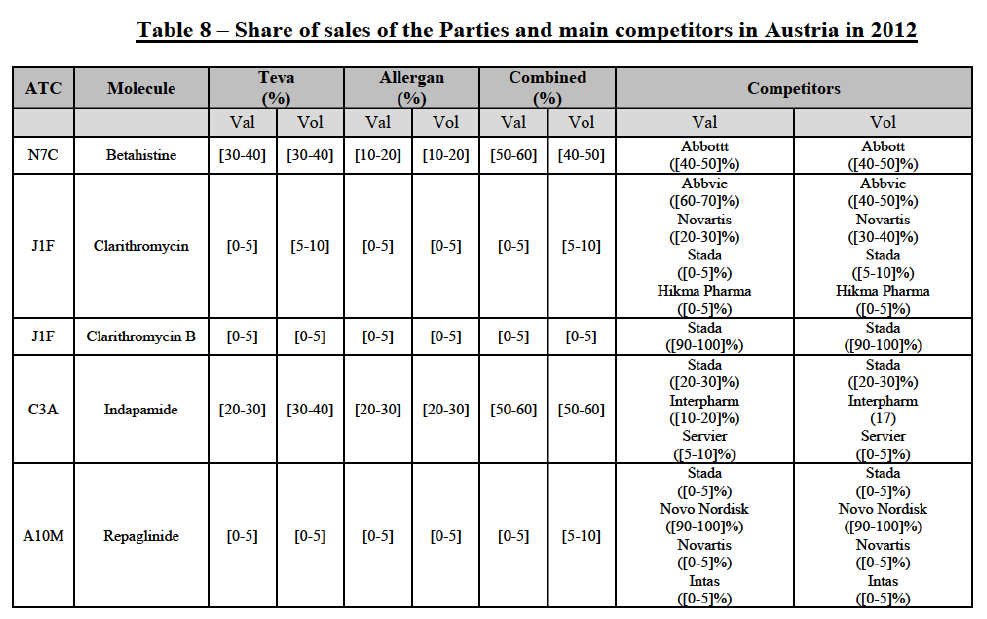

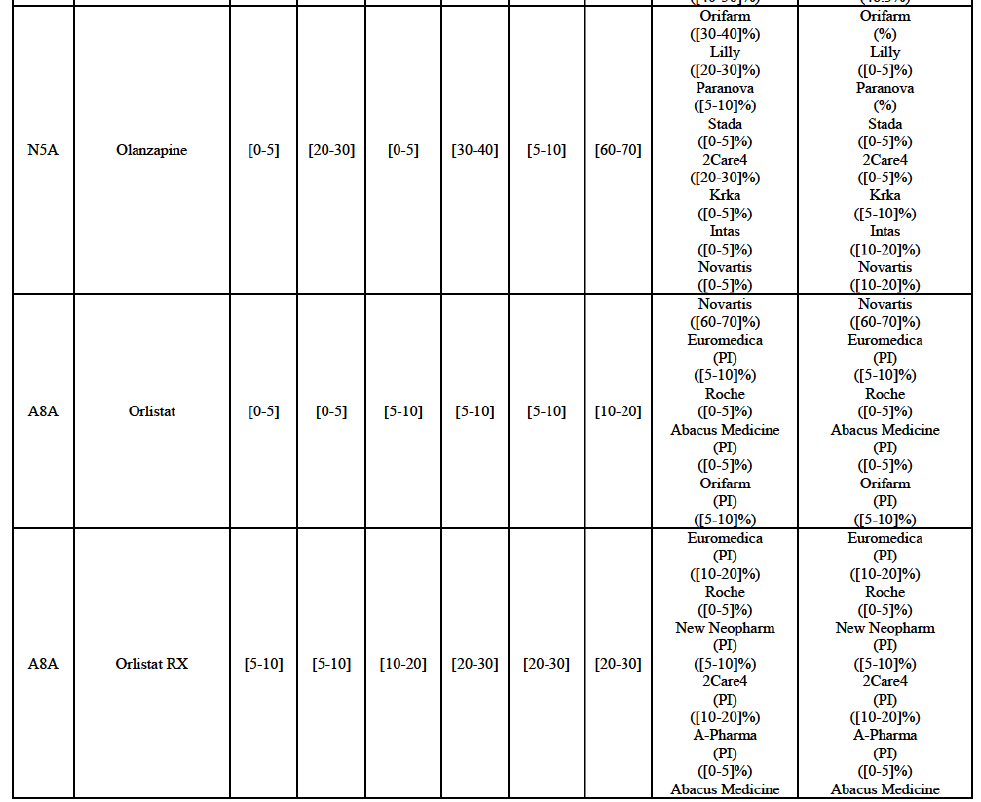

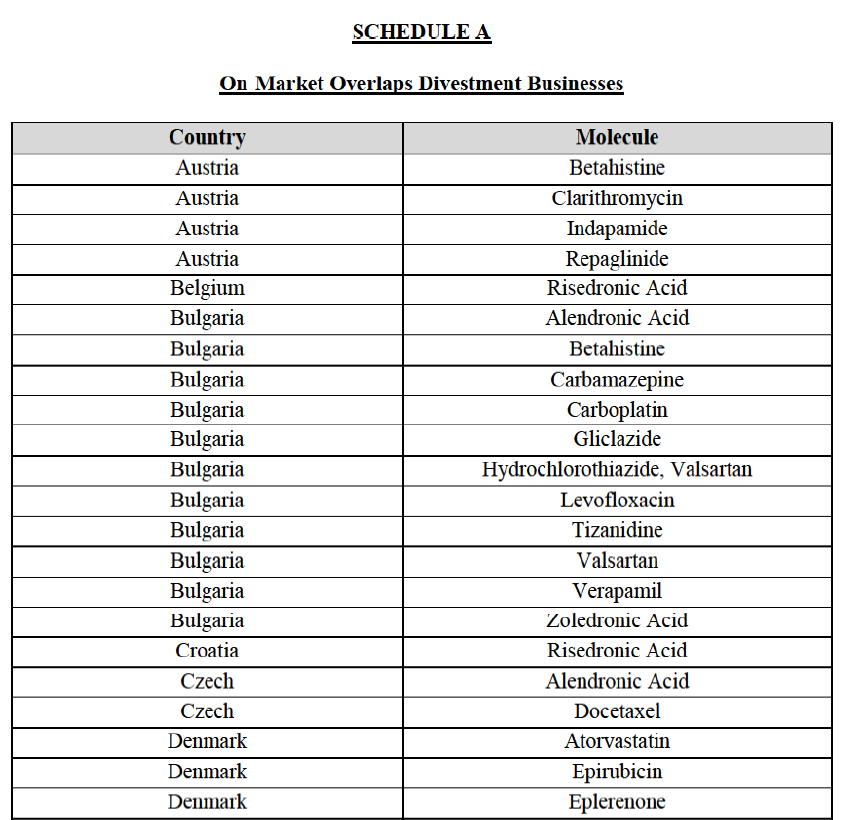

IV.2.2.2. Austria

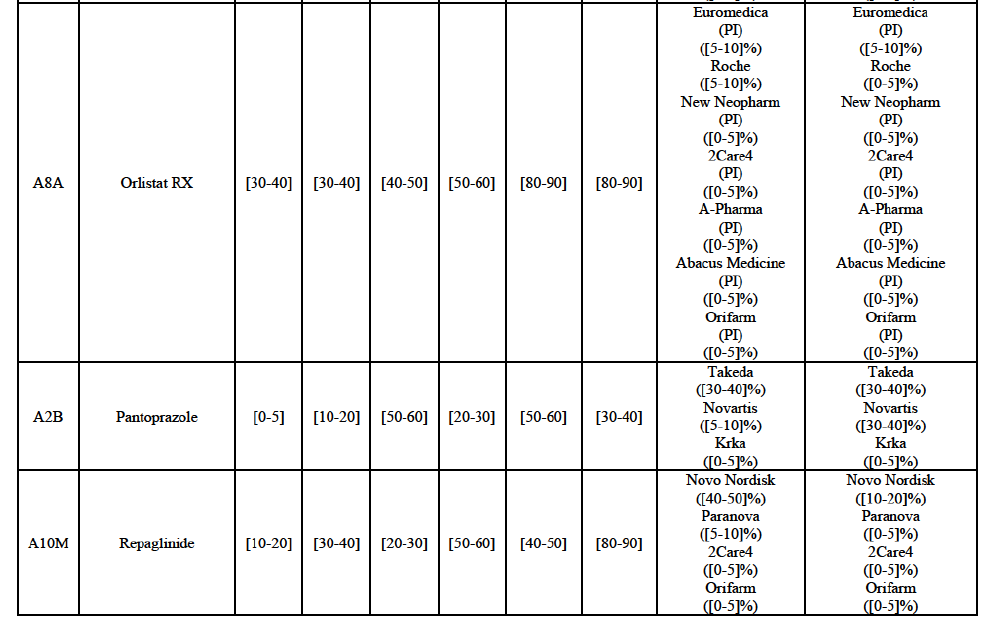

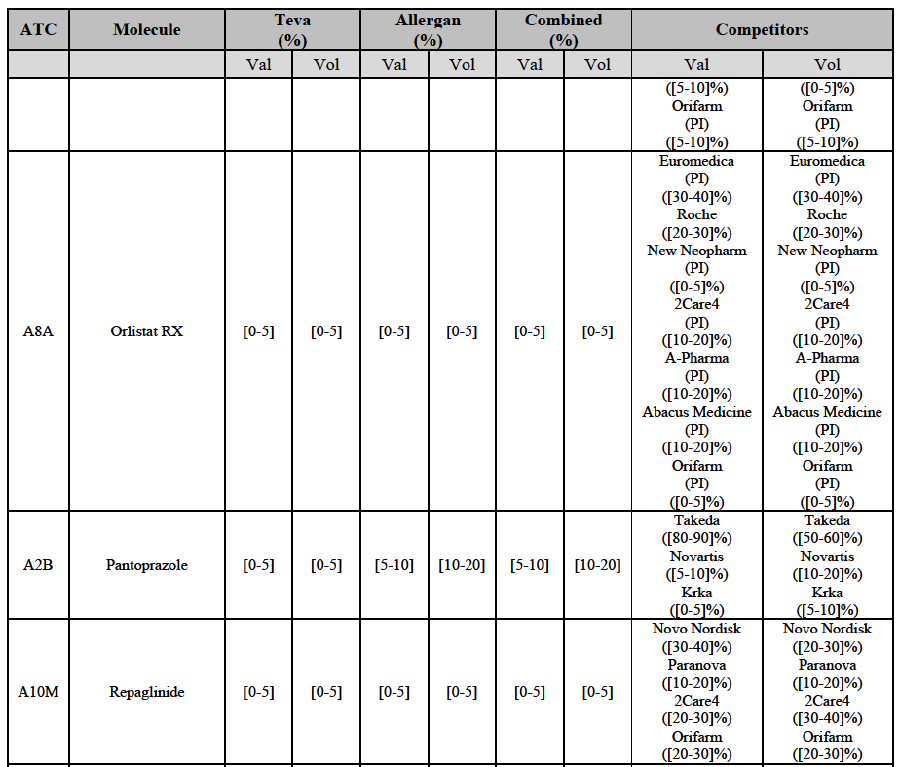

IV.2.2.2.a. Marketed generic pharmaceuticals

(66) The following tables present the market shares of the Parties and their main competitors in 2012, 2013 and 2014 for the Group 1/1+/2 markets for which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market.

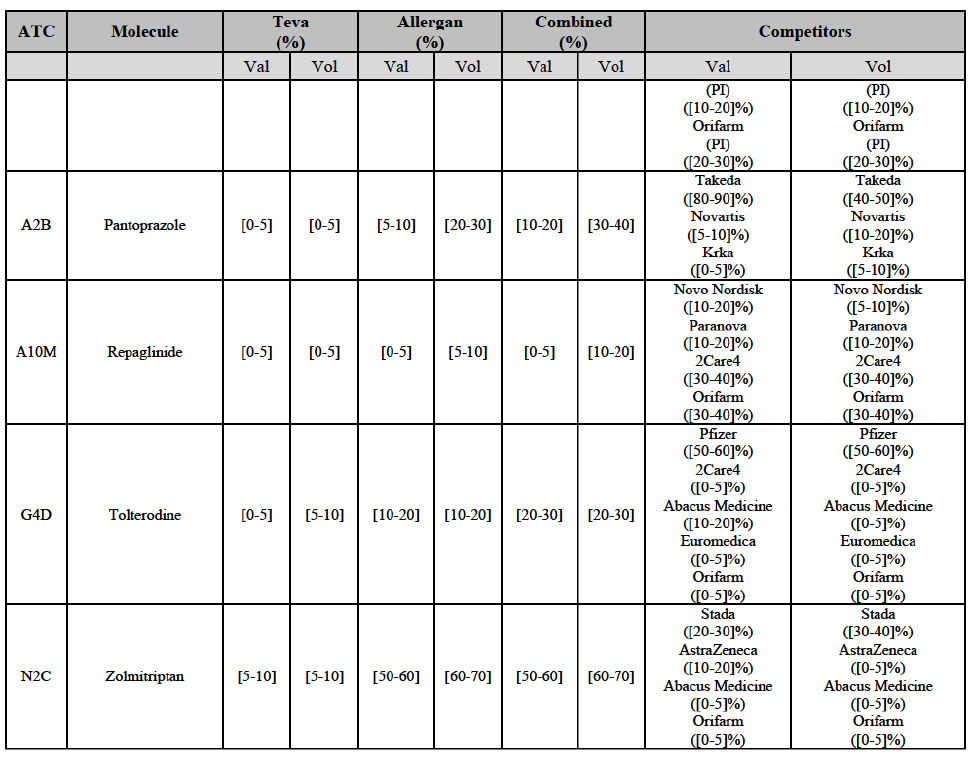

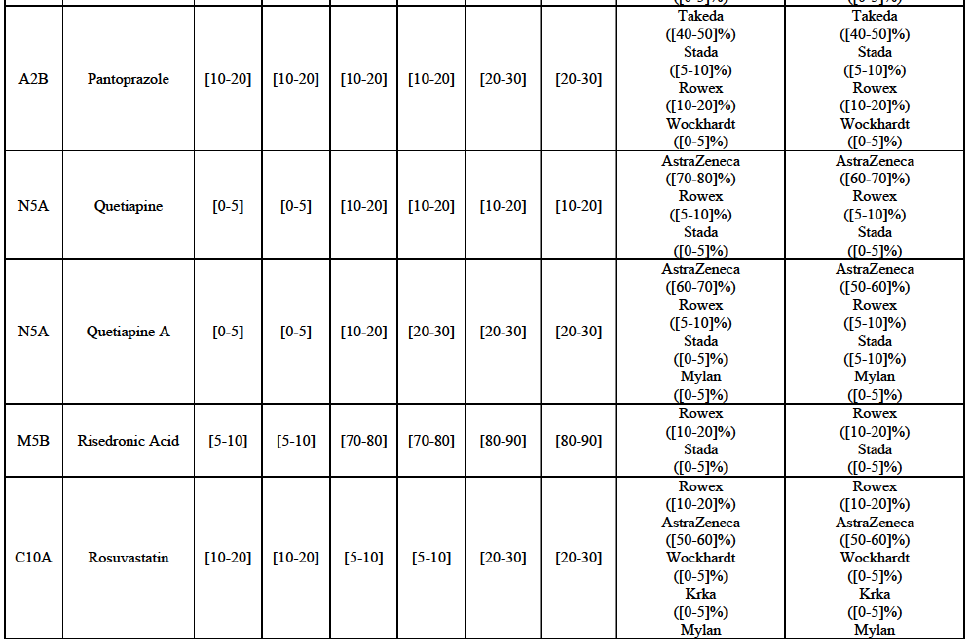

(67) The Commission presents below the competitive analysis on these markets, at molecule level, indicating also the ATC3 class to which it belongs, with a possible distinction by pharmaceutical form (at NFC1 level) and between prescribed and OTC sales where relevant.

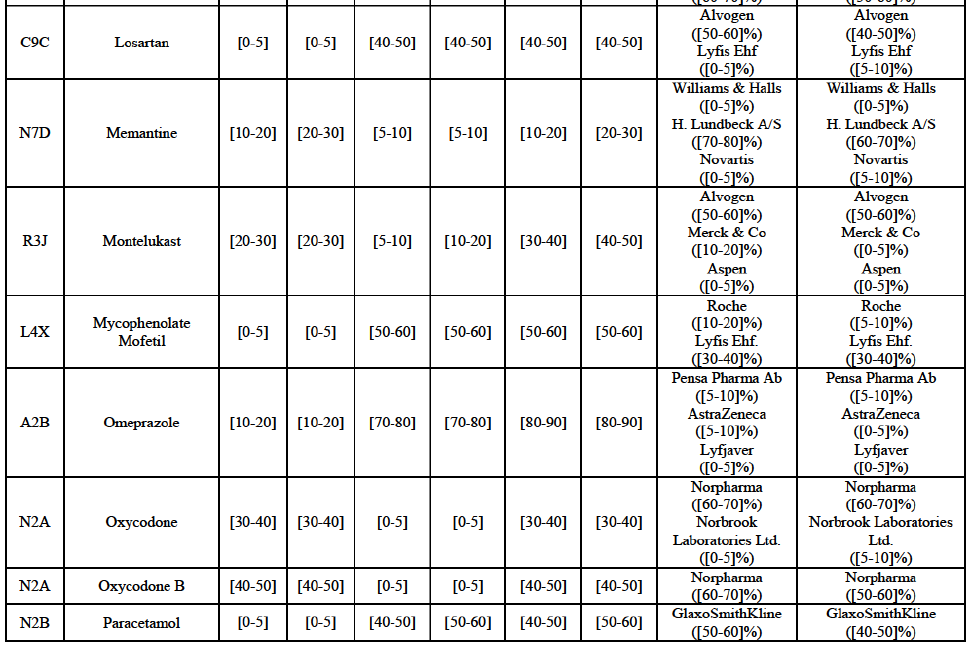

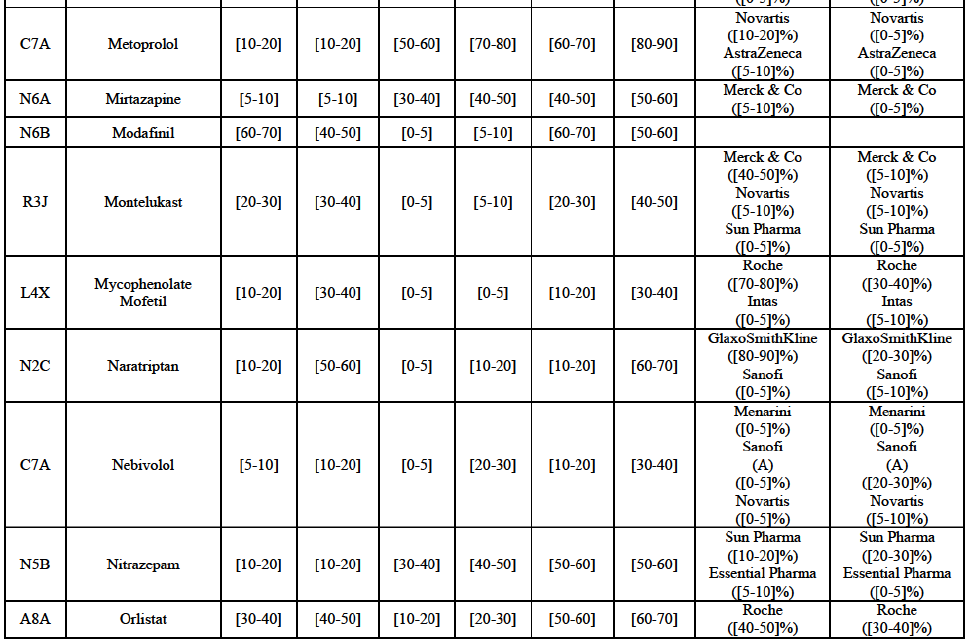

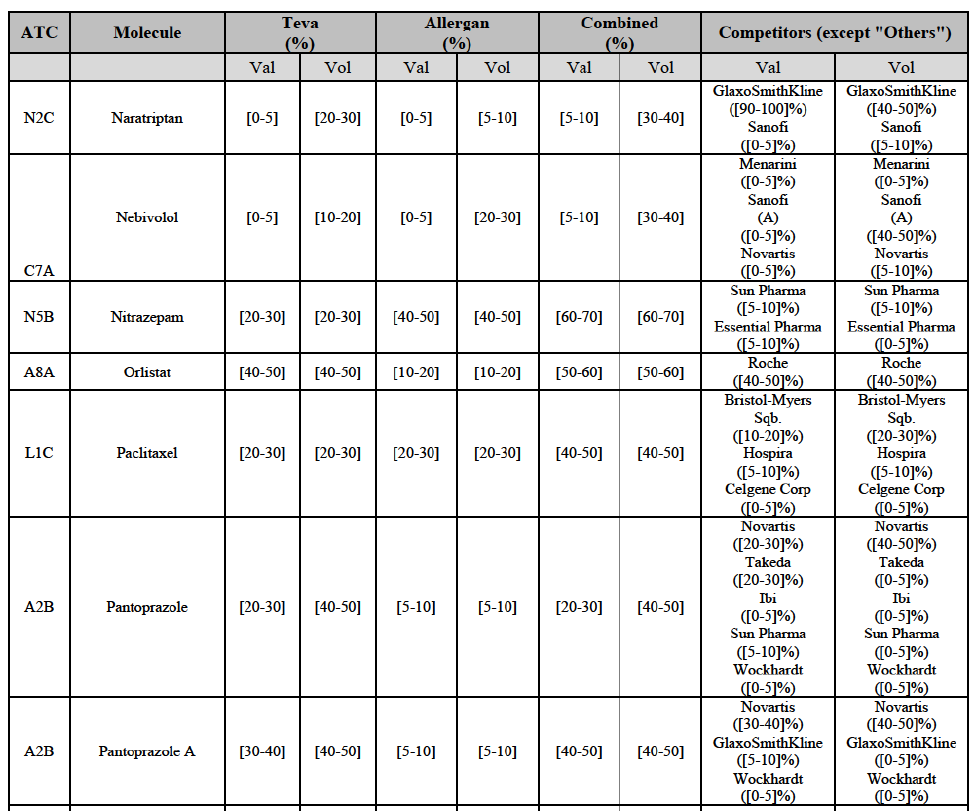

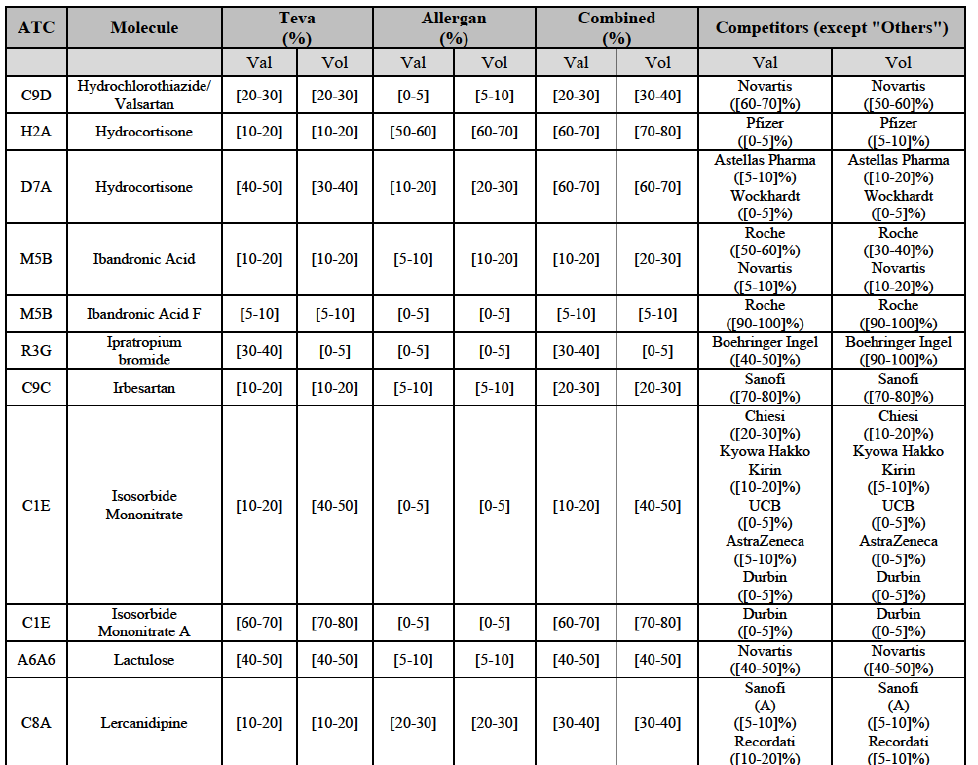

Betahistine (N7C)

(68) For betahistine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above [50-60]% in value and in volume, at the molecule and pharmaceutical form level, with a significant increment (above [10-201%). Only one other competitor with a market share above 5% would remain. Furthermore, the market investigation indicated that there would be a negative impact of the Transaction on this molecule.62

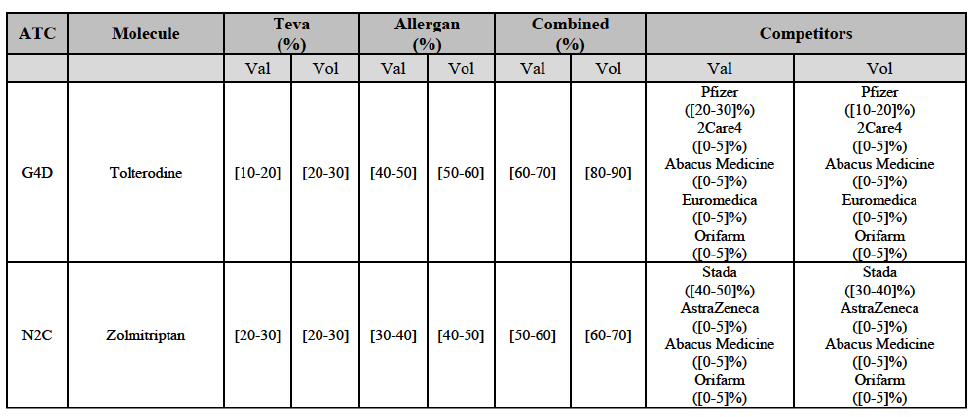

Clarithromycin (J1F)

(69) For clarithromycin, the Transaction gives rise to a Group 1 market at the level of the pharmaceutical form B in 2013. Allergan Generics recently entered the market (in 2012), and its market share fluctuated over the last three years (up to [5-10]% in 2013). In 2014, the combined market share of the Parties remained above [40-50]%. Only one other competitor would remain active on the market. Furthermore, the market investigation indicated that there would be a negative impact of the Transaction on this molecule.63

Indapamide (C3A)

(70) For indapamide, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above [50-60]% in the last three years in value and in volume, with an increment always above [20-30]%. Only two competitors that have a market share above 5% would remain on the market. Furthermore, the market investigation indicated that there would be a negative impact of the Transaction on this molecule."

Repaglinide (A1011I)

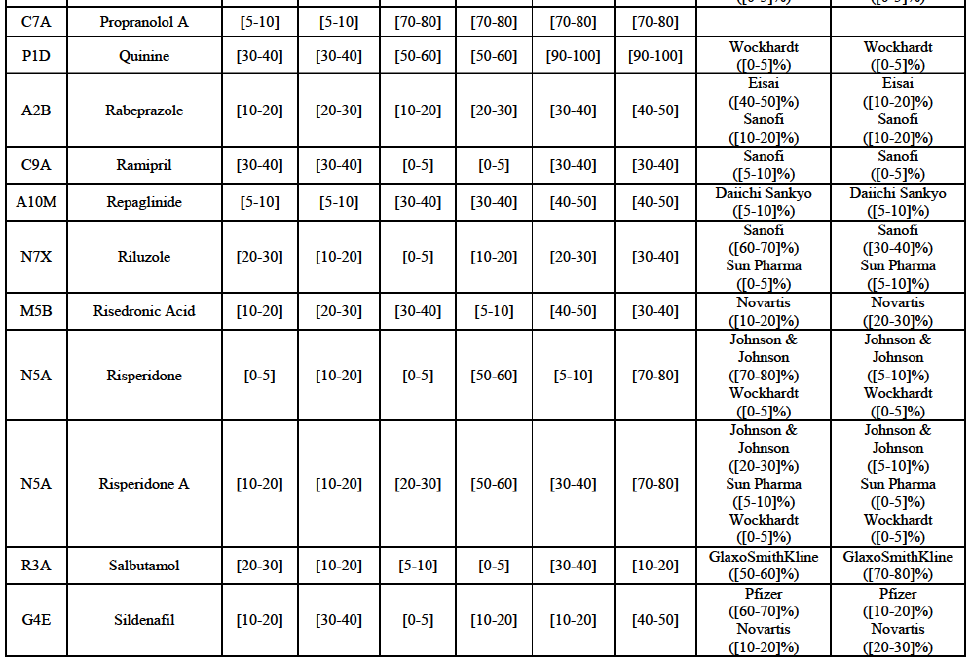

(71) For repaglidine, the Transaction gives rise to a Group 1 market at molecule level. The Parties recently entered and achieved in two years a combined market share above 50% ([50-601% in value and [60-70]% in volume), with a significant increment ([10-20]% in value and [10-20]% in volume). The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.65

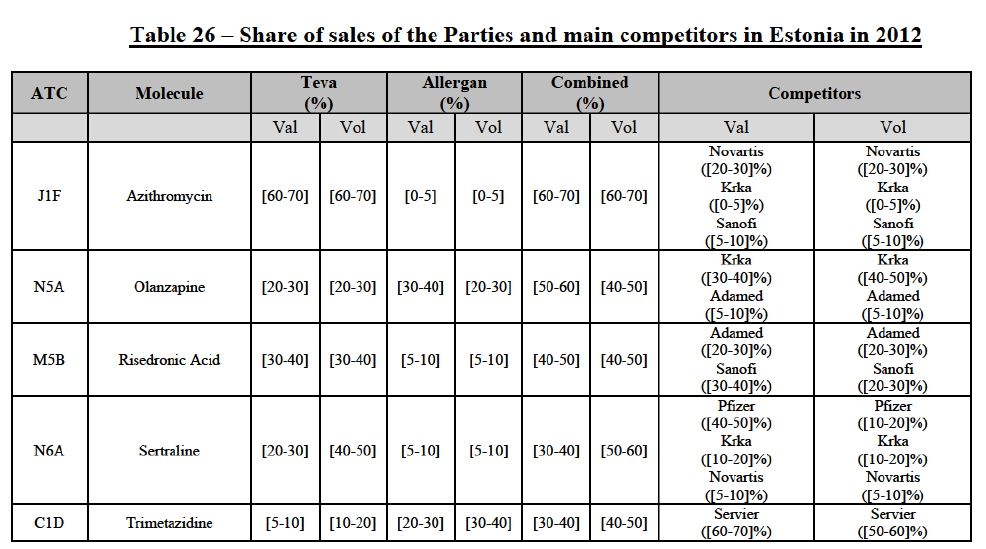

Conclusion

(72) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the markets for the marketing of betahistine, clarithromycin, indapamide and repaglinide in Austria.

IV.2.2.2.b. Pipeline generic pharmaceuticals

(73) The Transaction does not raise serious doubts as to its compatibility with the internal market with respect to pipeline generic pharmaceuticals in Austria.

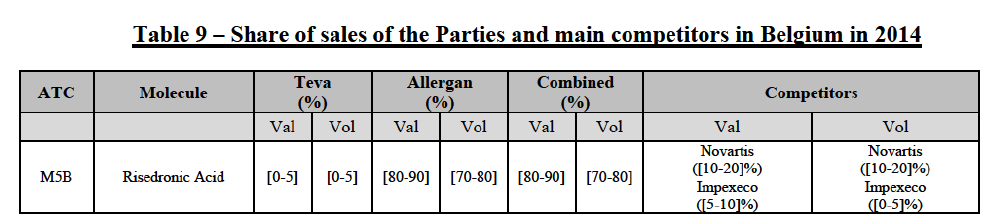

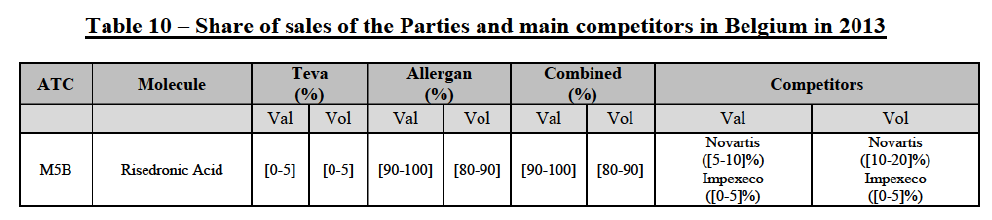

IV.2.2.3. Belgium

IV.2.2.3.a. Marketed generic pharmaceuticals

(74) The following tables present the market shares of the Parties and their main competitors in 2012, 2013 and 2014 for the Group 1/1+/2 market for which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market.

(75) The Commission presents below the competitive analysis on this market, at molecule level, indicating also the ATC3 class to which it belongs, with a possible distinction by pharmaceutical form (at NFC1 level) and between prescribed and OTC sales where relevant.

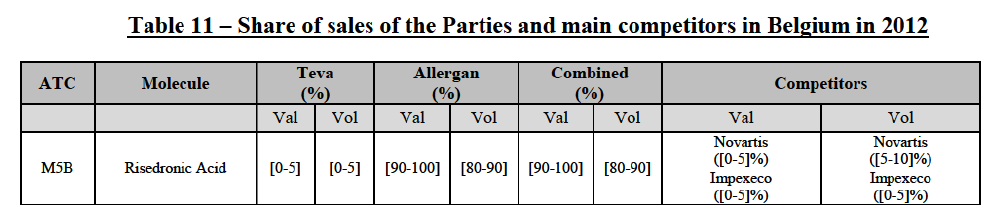

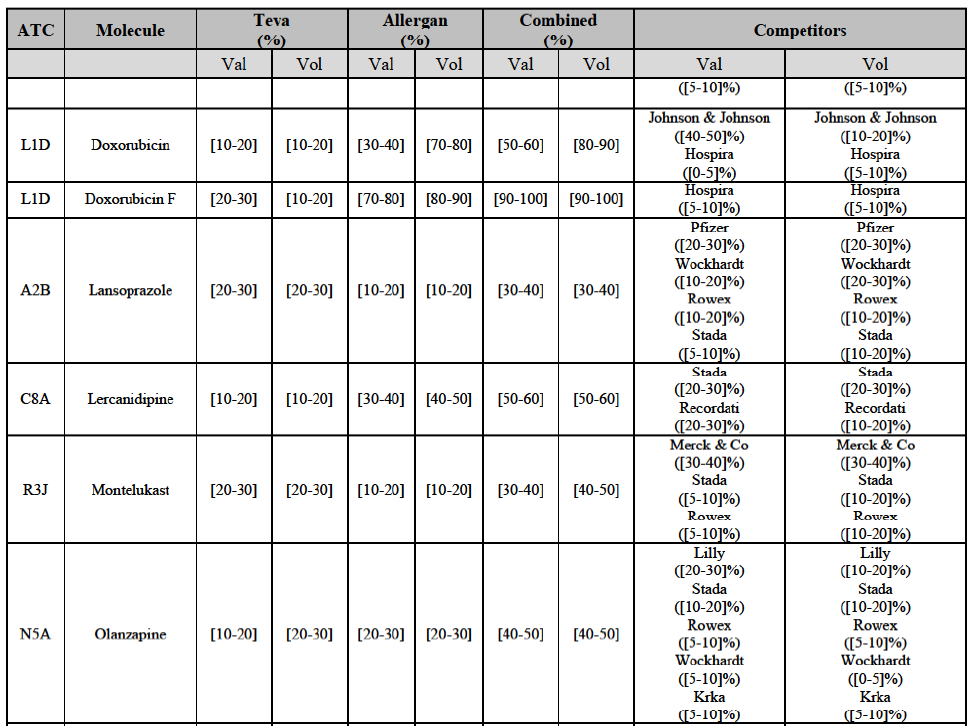

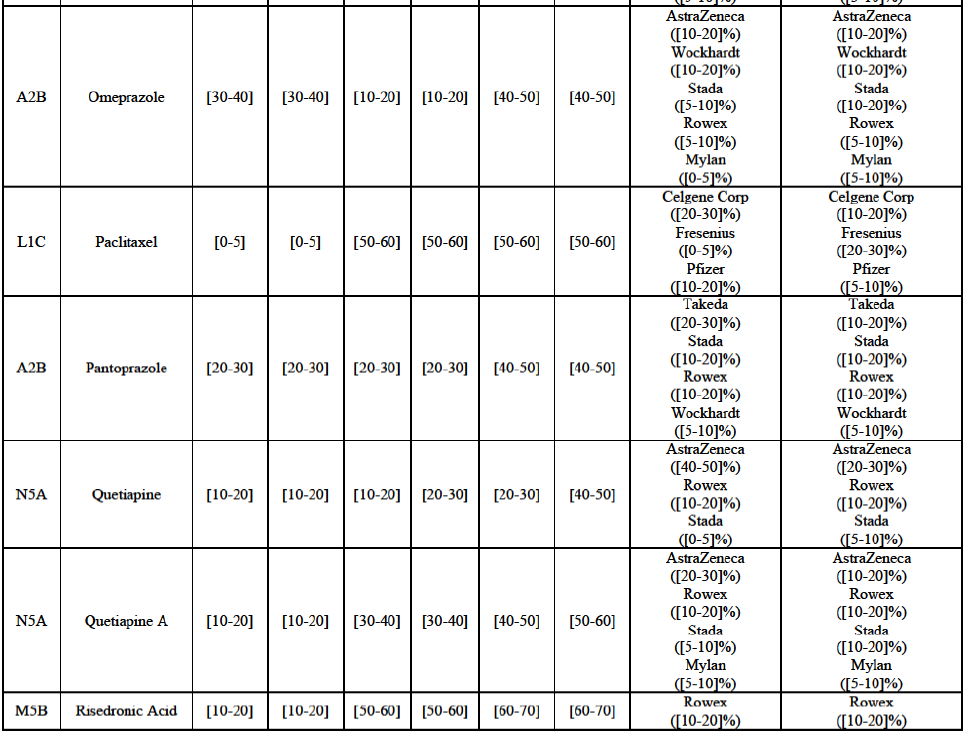

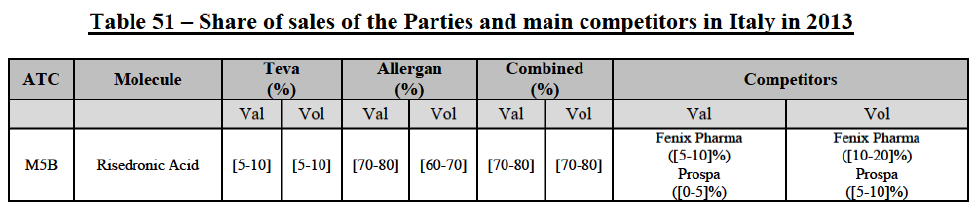

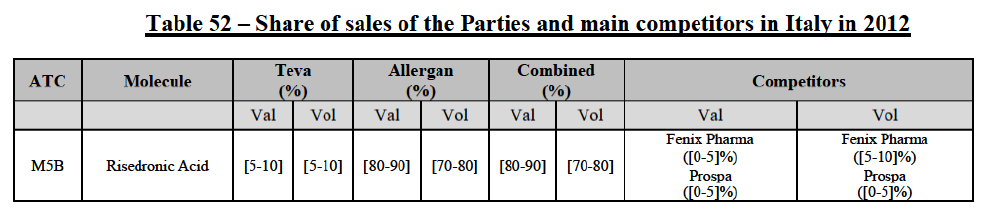

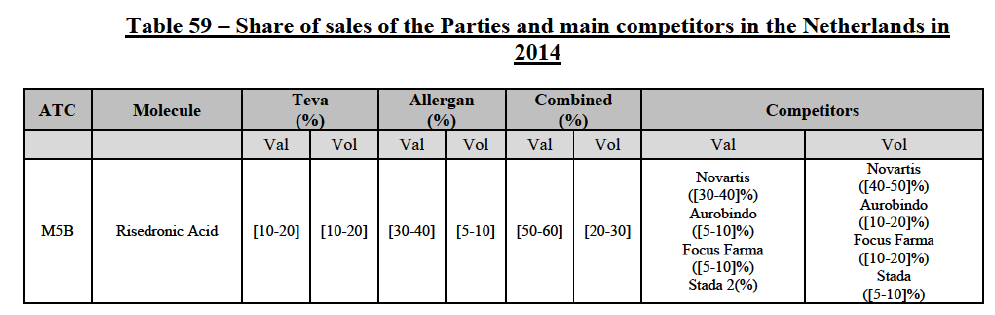

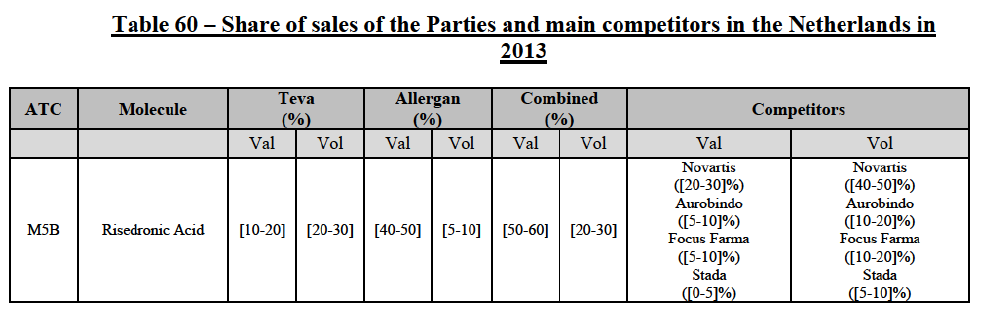

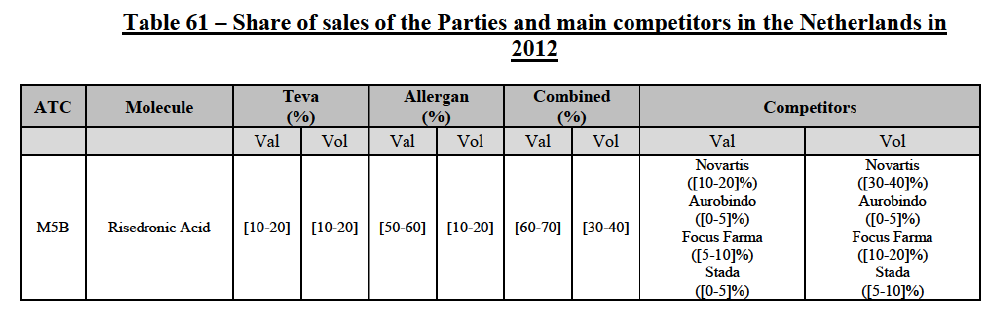

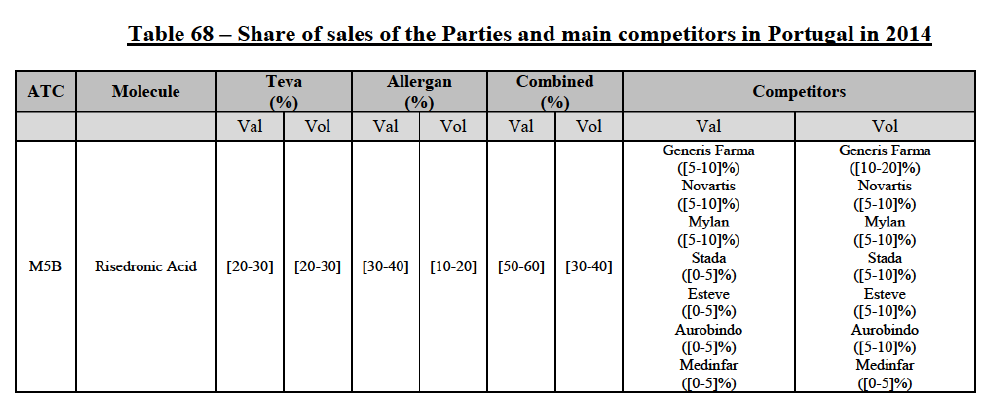

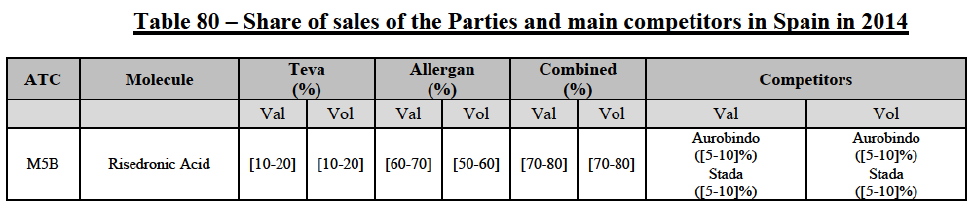

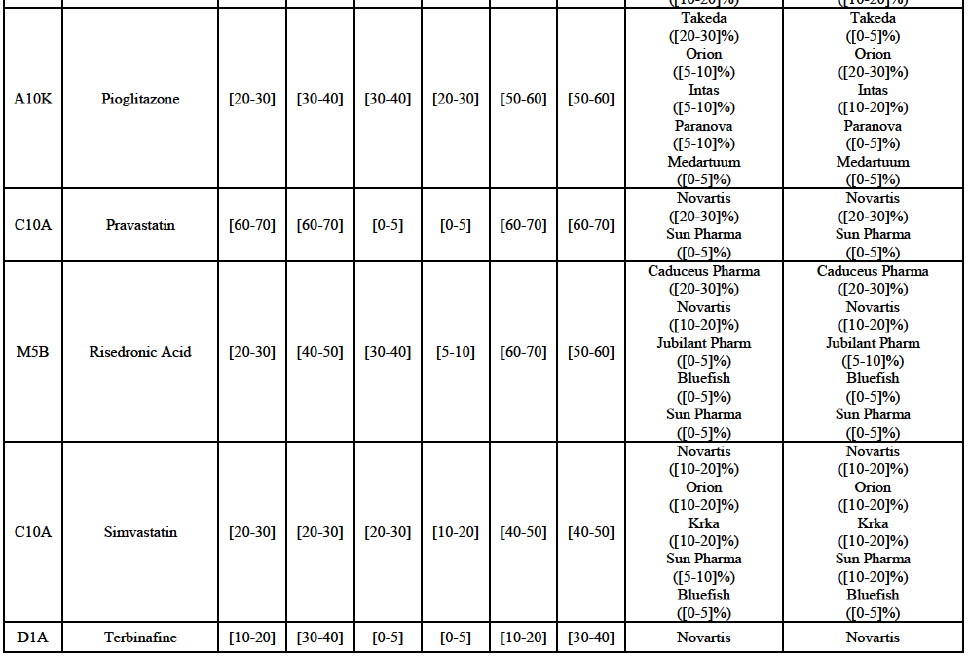

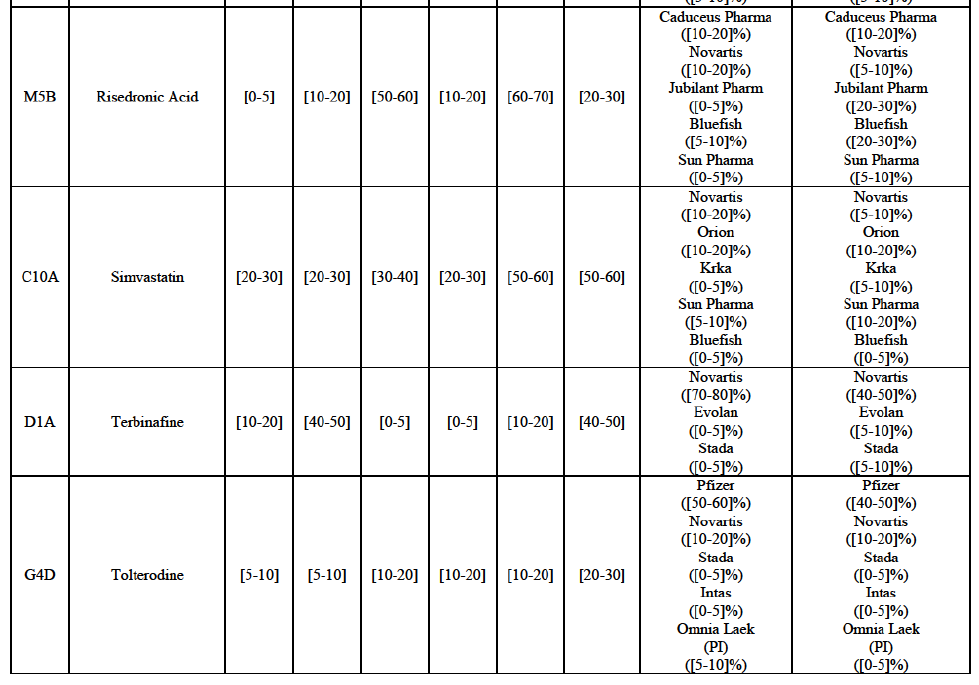

Risedronic Acid (M5B)

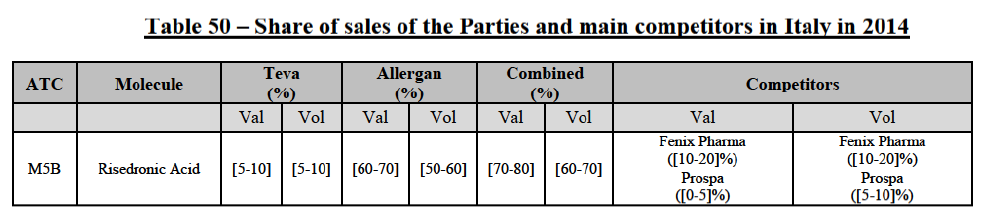

(76) For risedronic acid, the Transaction gives rise to a Group 1 market at molecule level. Allergan Generics is the originator of this molecule. The combined market share of the Parties is very high, above [80-90]% in volume and [90-100]% in value since 2013. Only one competitor with a market share above 5% would remain on the market. Furthermore, the market investigation confirmed the strong position of the Parties.66

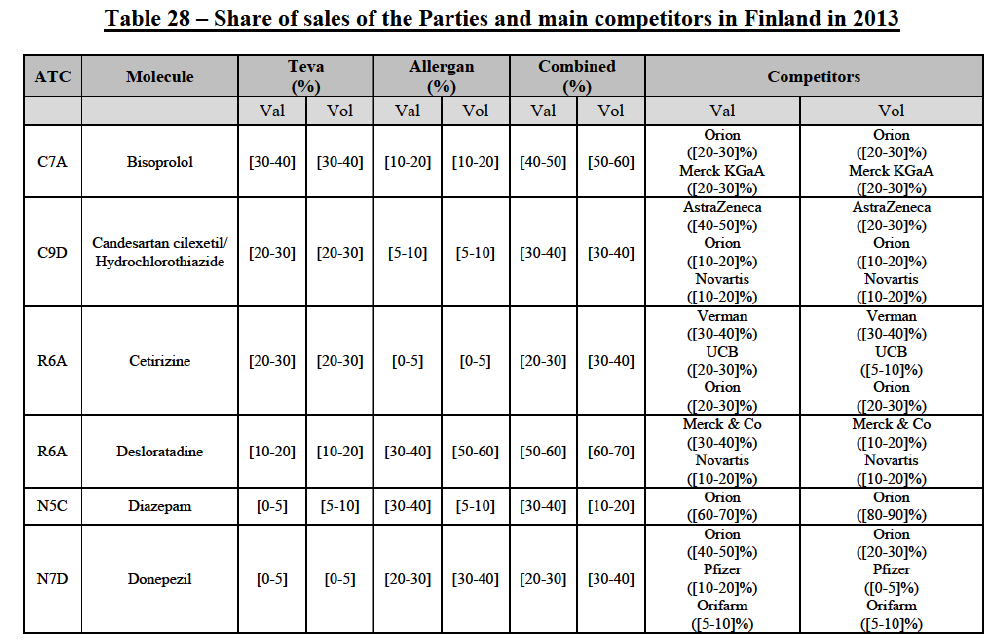

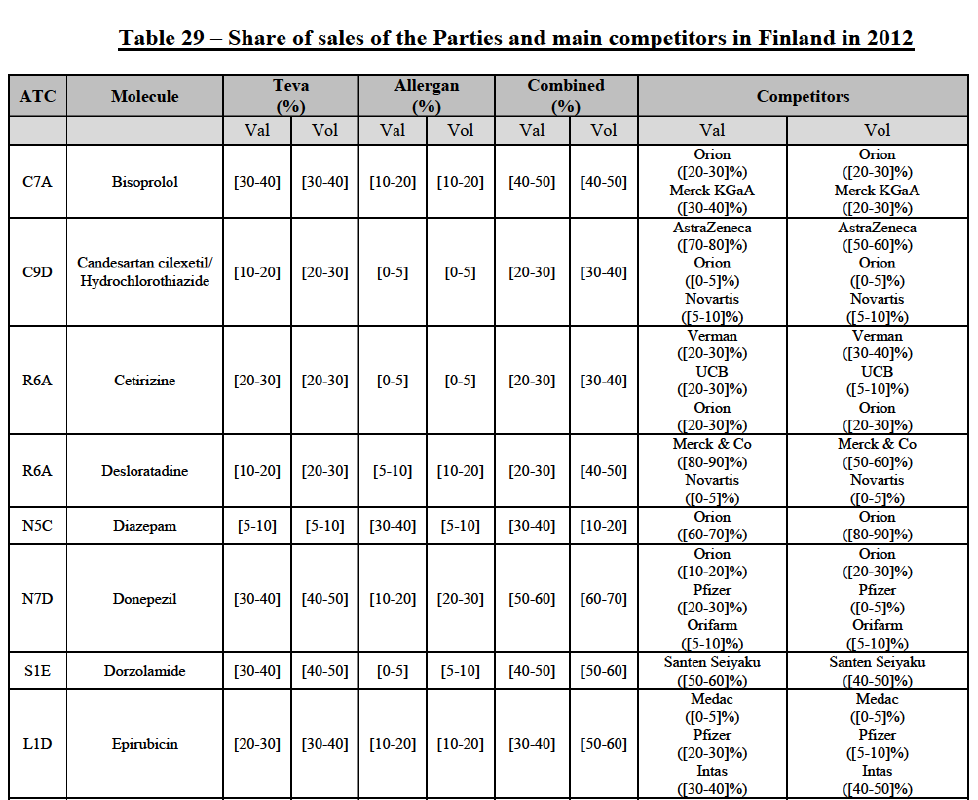

(77) The Notifying Party submits that the molecule risedronic acid has been delisted by Teva prior to the announcement of the Transaction. However, Teva's marketing authorisation is still valid, and the Parties acknowledge that it would therefore take up to six months only to come back to the market.67 Therefore, the Commission considers that the Parties' activities overlap irrespective of Teva's decision to delist the product.

Conclusion

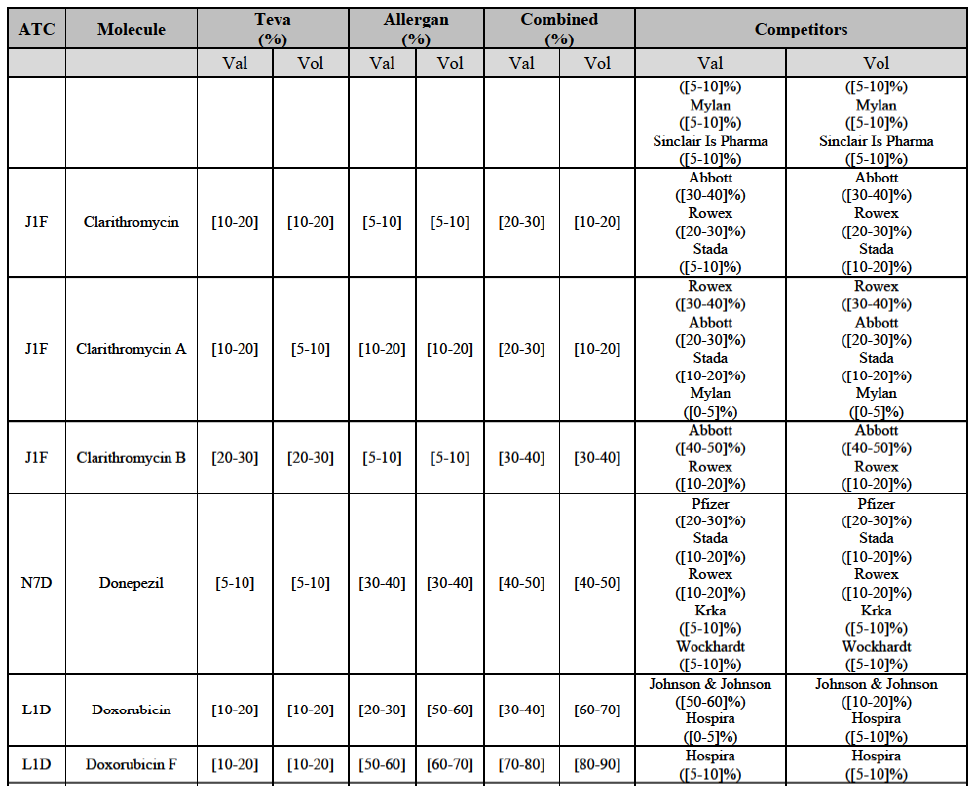

(78) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the marketing of risedronic acid in Belgium.

IV.2.2.3.b. Pipeline generic pharmaceuticals

(79) Allergan Generics is planning to launch a generic [...] (pharmaceutical form [...]), for which Teva had a[40-50]% market share in value ([10-201% in volume) in 2014 on the same pharmaceutical form, and only one other competitor was active on the market in 2012-2014.

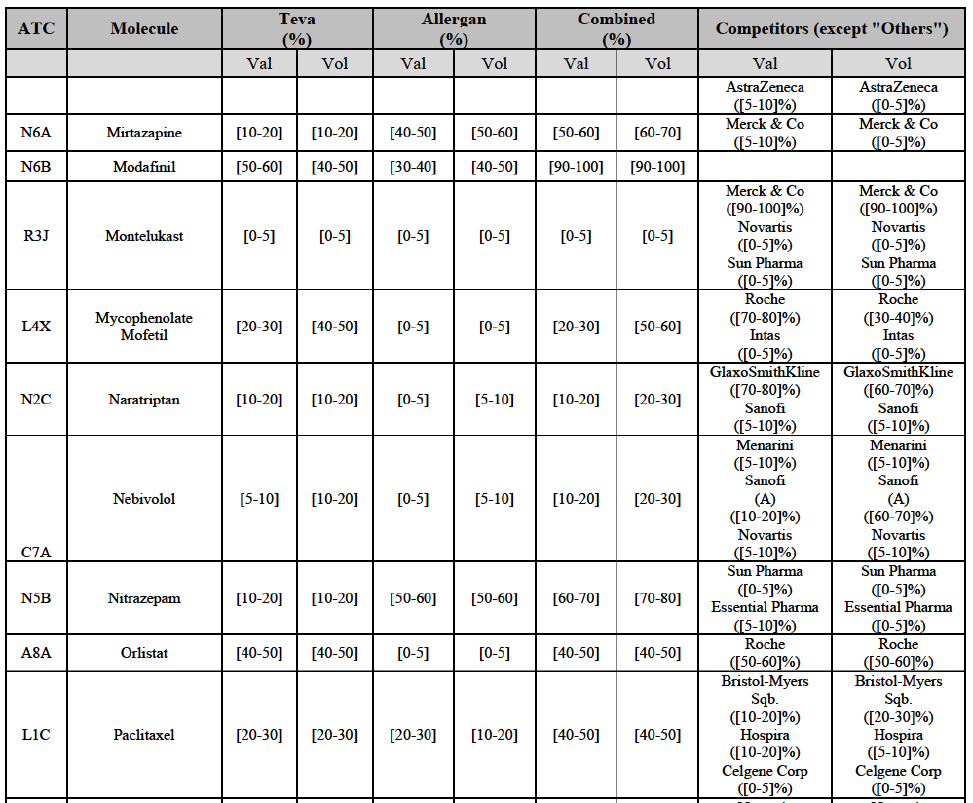

Conclusion

(80) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the market for the marketing of [...] in Belgium.

IV.2.2.4. Bulgaria

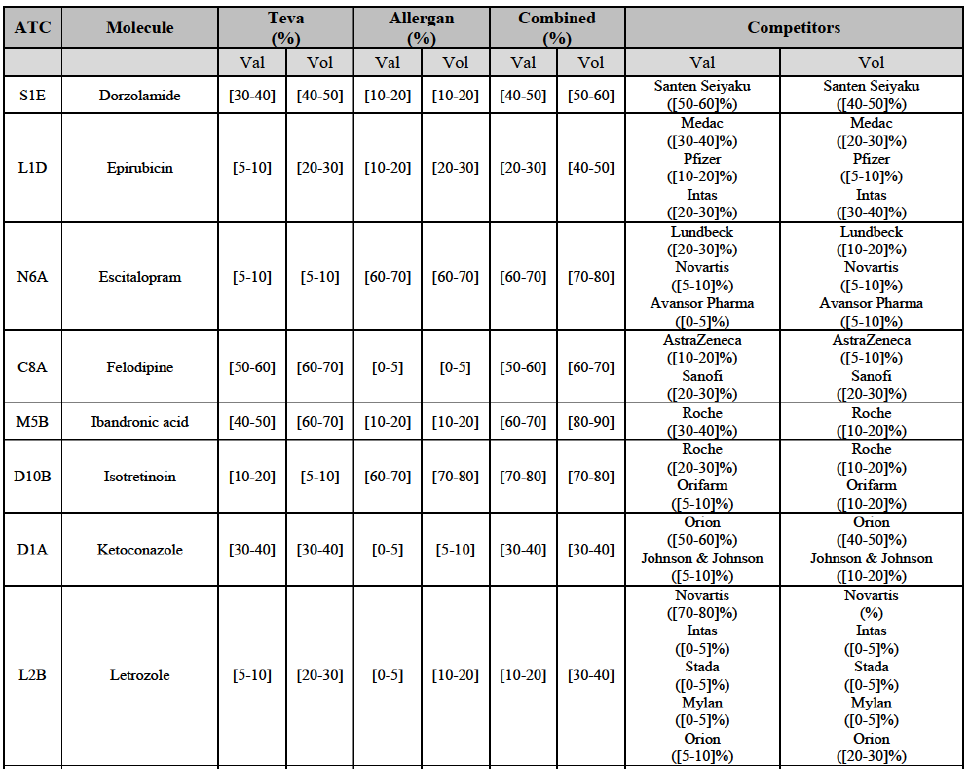

IV.2.2.4.a. Marketed generic pharmaceuticals

(81) The following tables present the market shares of the Parties and their main competitors in 2012, 2013 and 2014 for the Group 1/1+/2 markets for which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market.

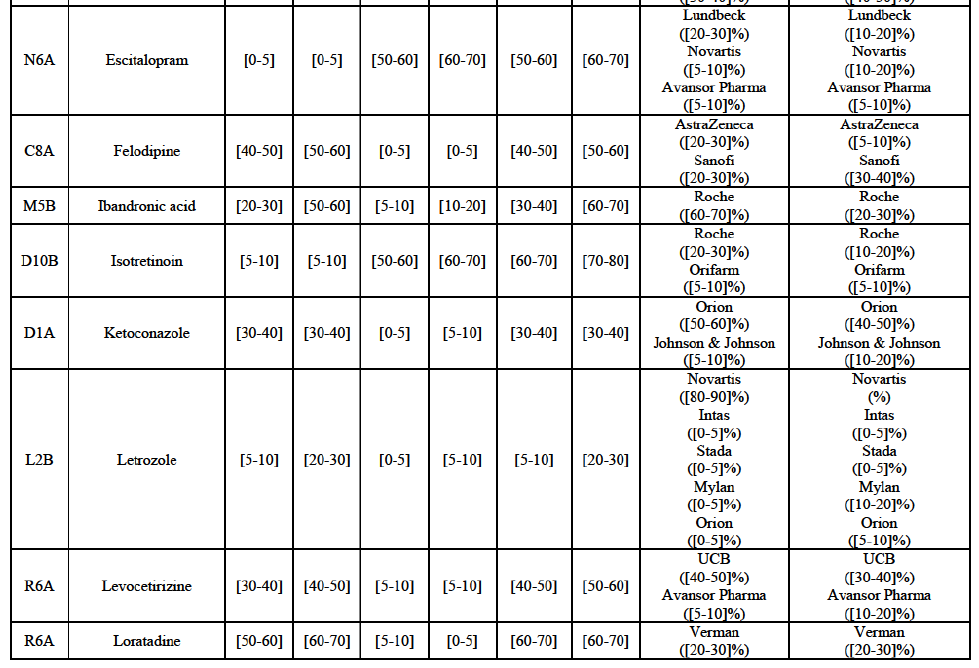

(82) The Commission presents below the competitive analysis on these markets, at molecule level, indicating also the ATC3 class to which it belongs, with a possible distinction by pharmaceutical form (at NFC1 level) and between prescribed and OTC sales where relevant.

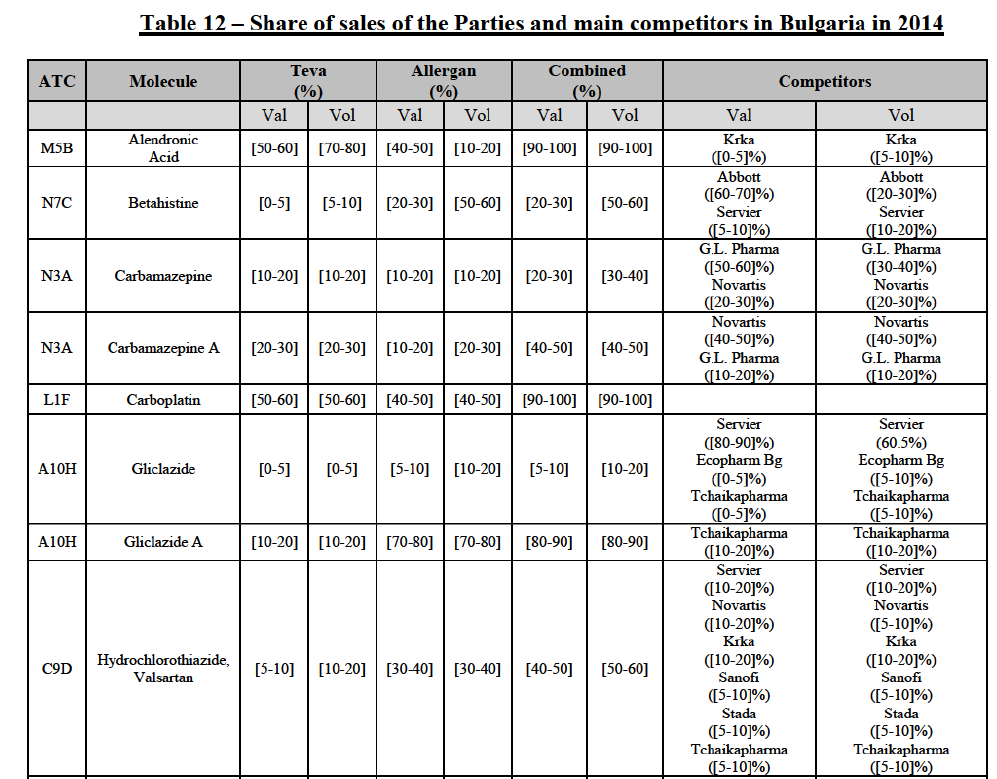

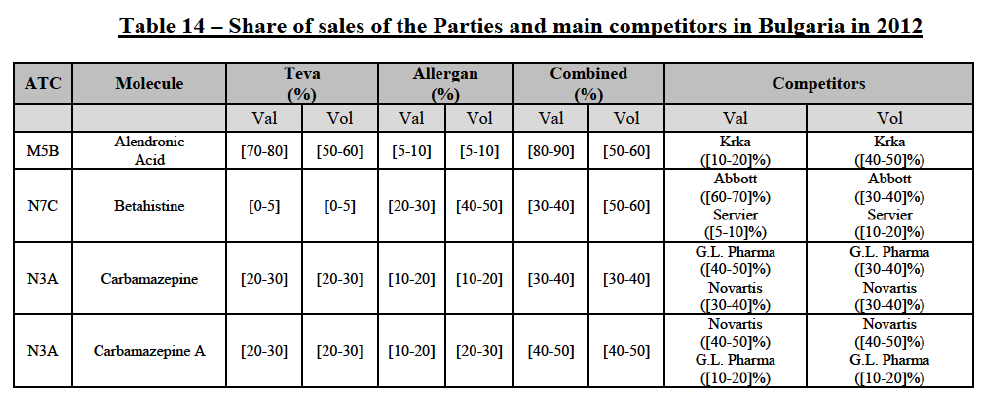

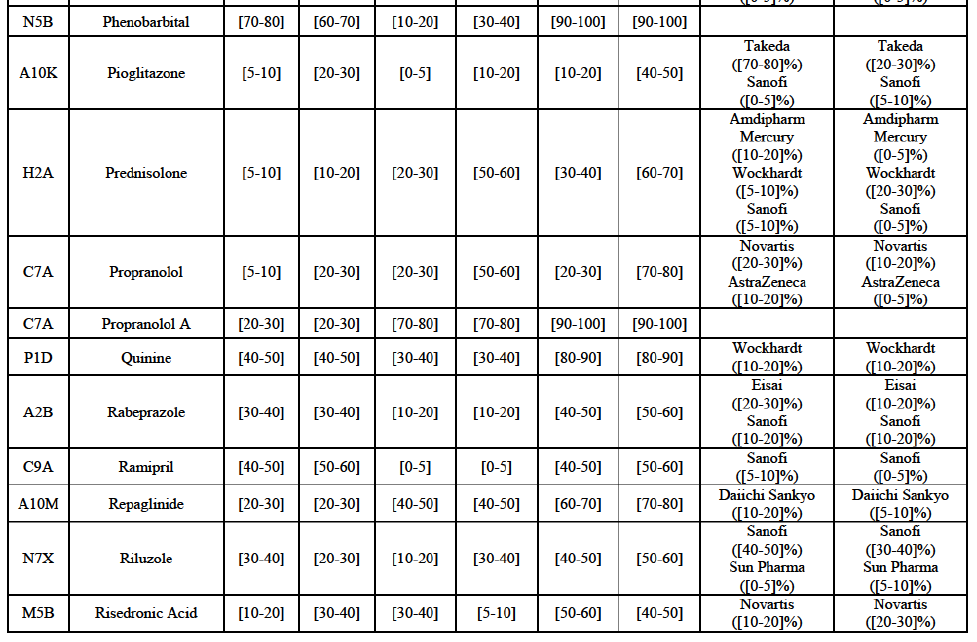

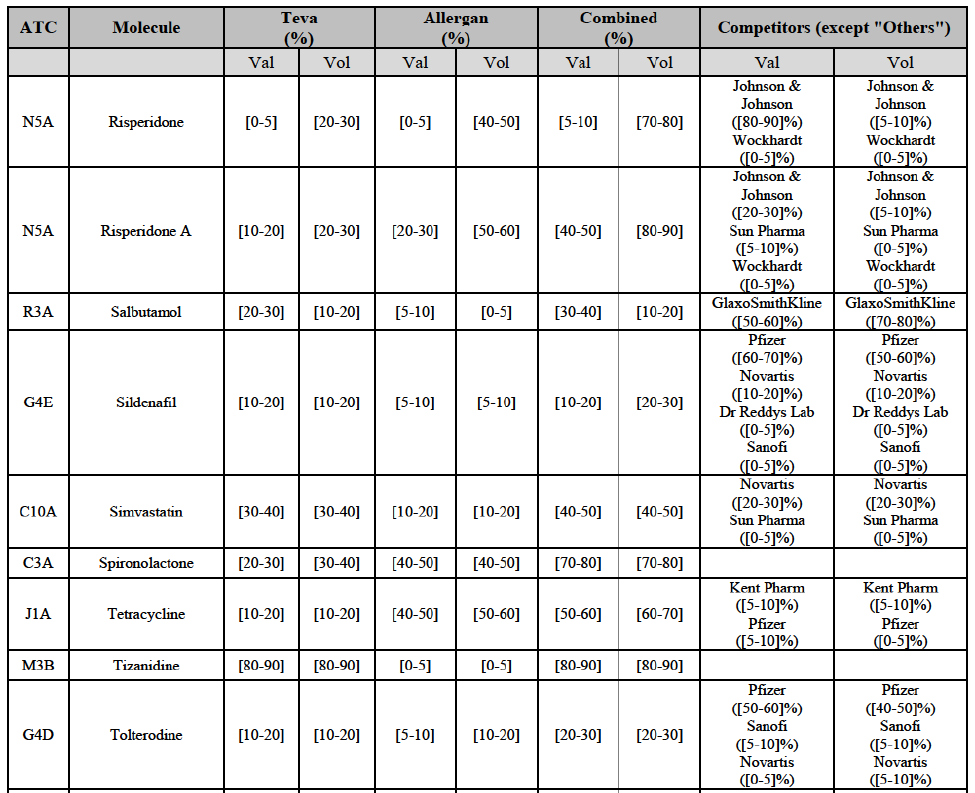

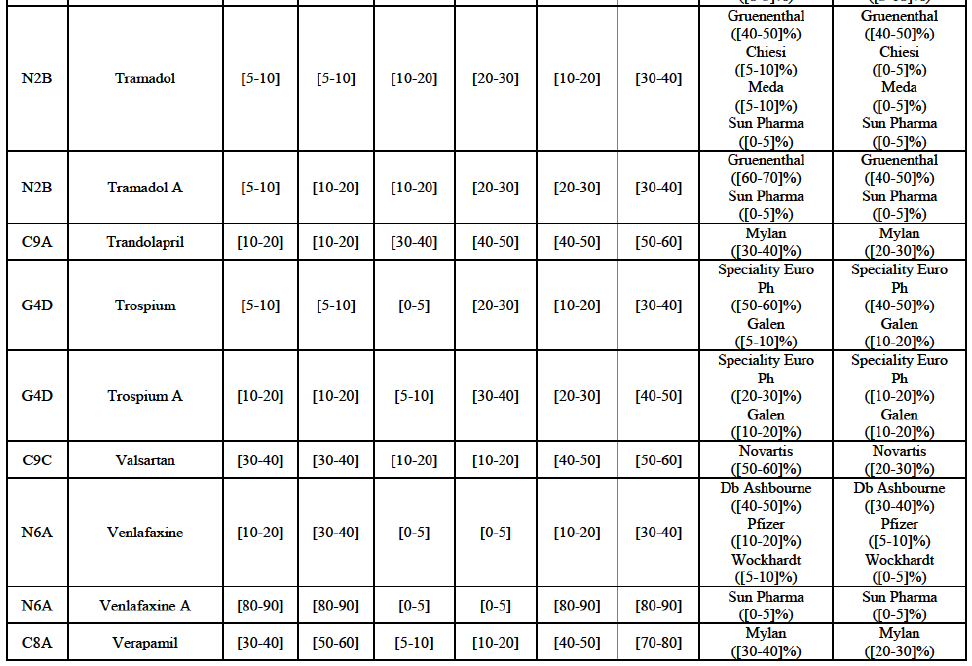

Alendronic Acid (M5B)

(83) For alendronic acid, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above[90-100]% in value and in volume in 2014, with a significant increment (respectively [40-50]% and [10-20]% in 2014). There would be no remaining competitor with a market share above 5% in value (and only one in volume). Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market and that it would be difficult to switch to alternative suppliers.68

Betahistine (N7C)

(84) For betahistine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above [50-60]% in volume in the last three years. Only two competitors, including the originator, would remain with a market share above 5%. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market.69

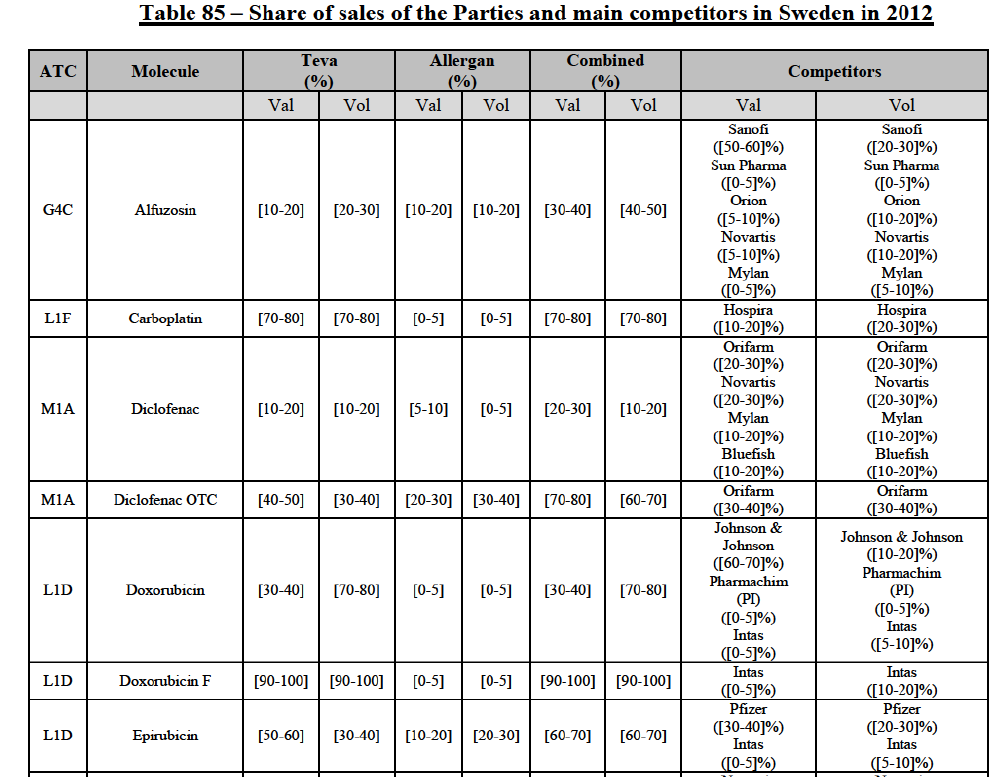

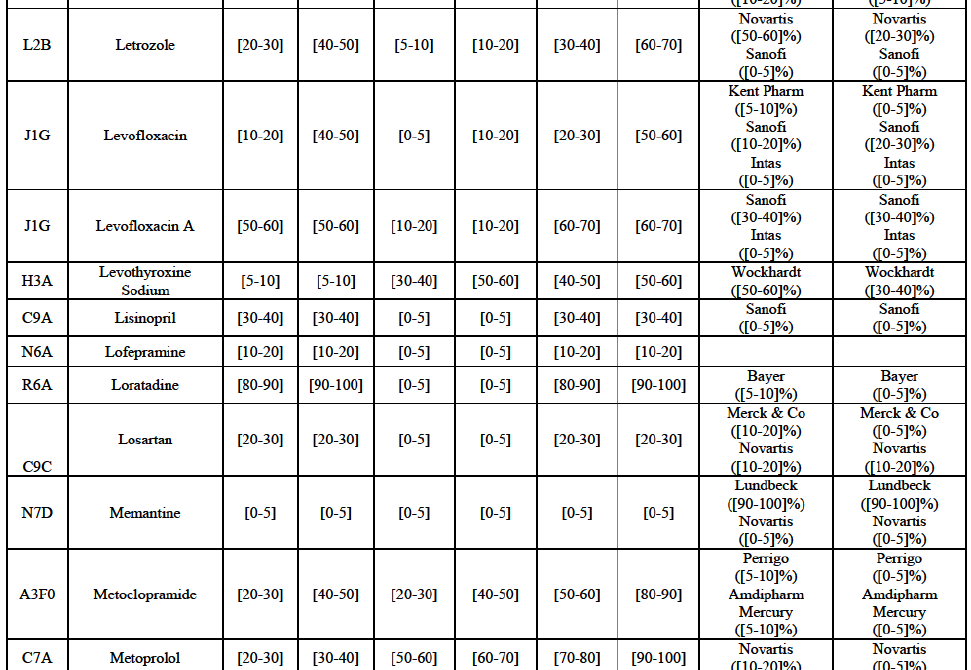

Carbamazepine (N3A)

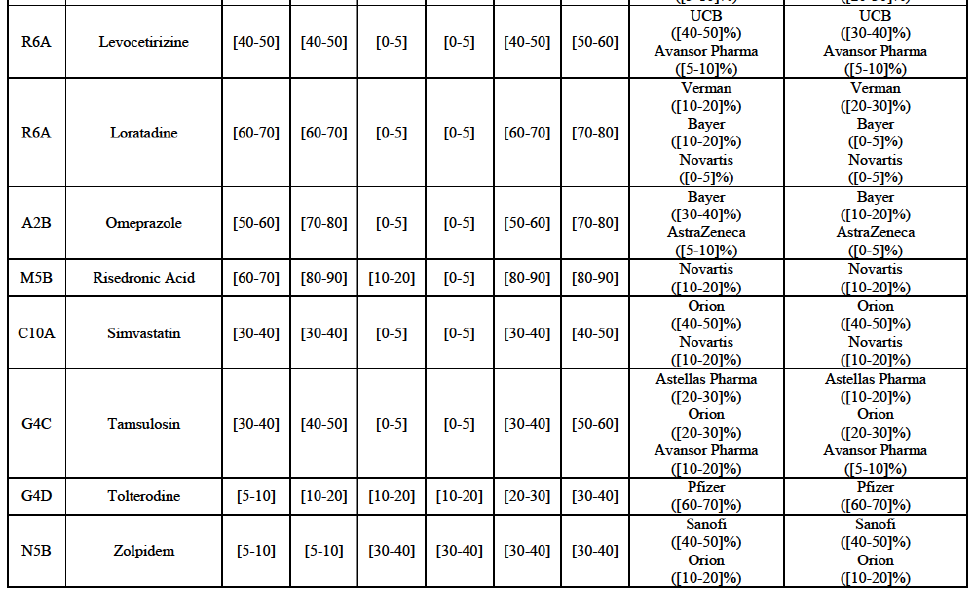

(85) For carbamazepine, the Transaction gives rise to a Group 1 market at the level of the pharmaceutical level A. The Parties' combined market share was high over the last three years in value and in volume, between [30-40]% and [40-50]%. Only two competitors, including the originator, would remain on the market. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market.70

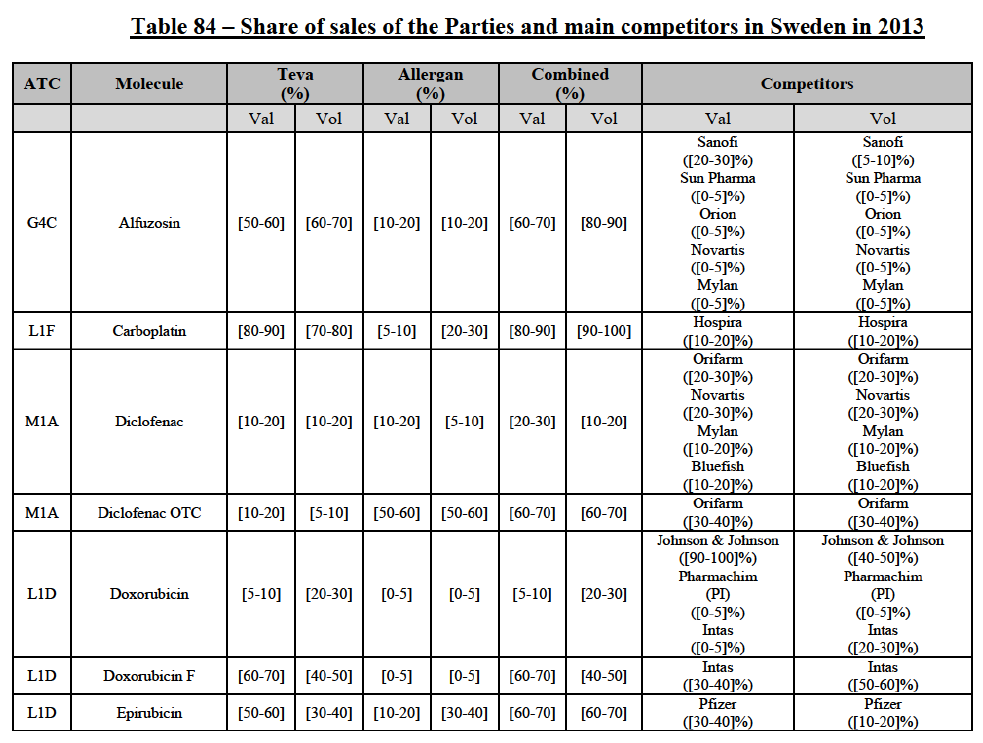

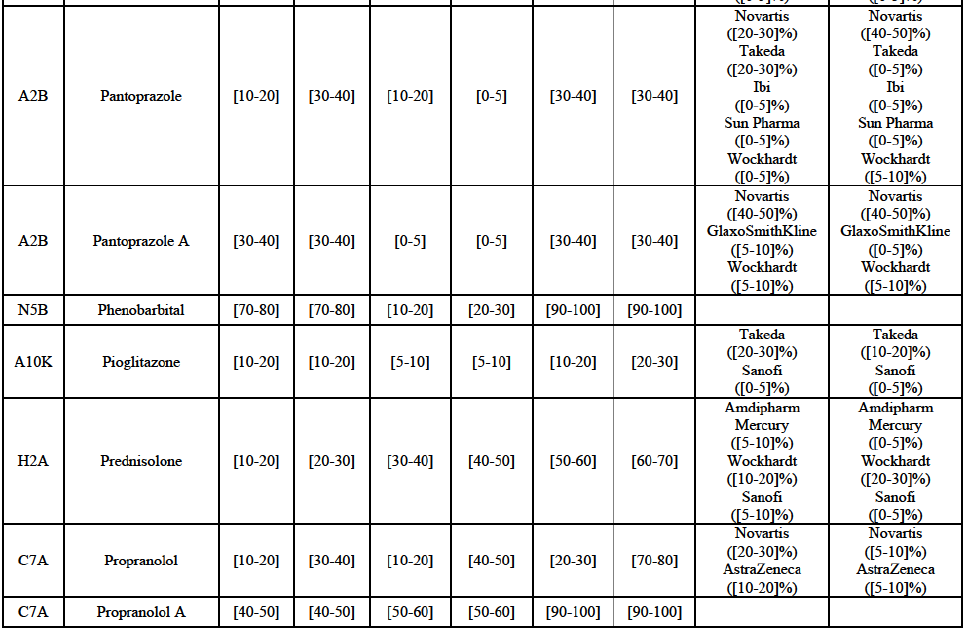

Carboplatin (L1F)

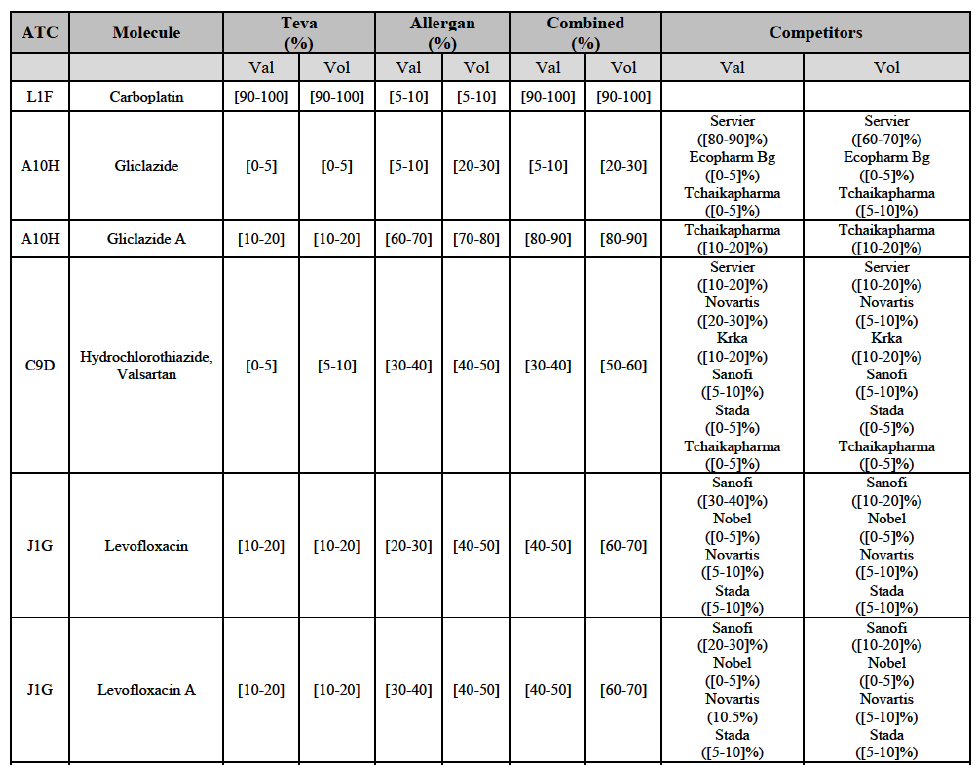

(86) For carboplatin, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was >[90-100]% in value and volume in 2013 and 2014, with a significant increment (above [40-50]%). No alternative competitors would remain on the market. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market.71

(87) The Notifying Party submits that the molecule carboplatin has been delisted by Teva prior to the announcement of the Transaction. However, Teva's marketing authorisation is still valid, and the Parties acknowledge that it would therefore take up to six months only to come back to the market.72 Therefore, the Commission considers that the Parties' activities overlap irrespective of Teva's decision to delist the product.

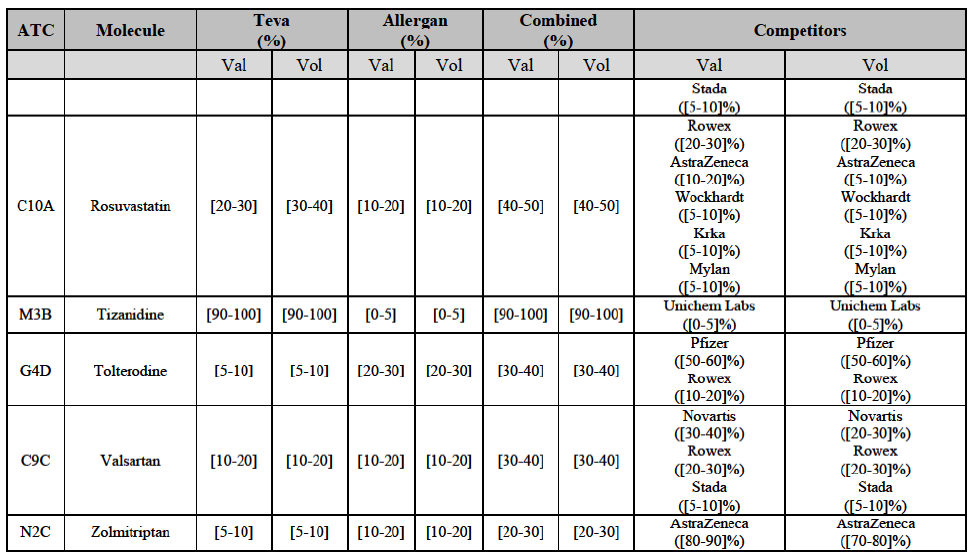

Gliclazide (A10H)

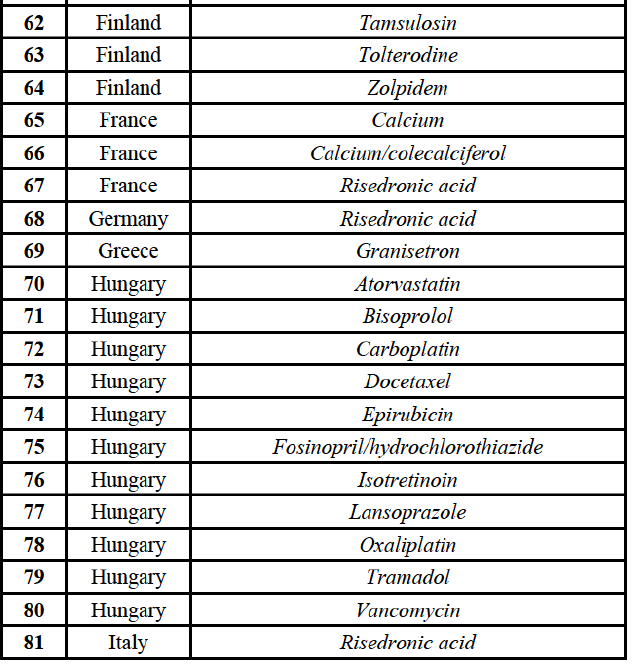

(88) For gliclazide, the Transaction gives rise to a Group 1 market at the level of the pharmaceutical form A. The Parties' combined market share was above [80-90]% both in value and volume over the last three years, with a significant market share increment. Only one competitor with a market share above 5% would remain on the market at the given pharmaceutical form level. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market and that it would be difficult for customers to switch to alternative suppliers.73

(89) The Notifying Party submits that the molecule gliclazide has been delisted by Teva prior to the announcement of the Transaction. However, Teva's marketing authorisation is still valid, and the Parties acknowledge that it would therefore take up to six months only to come back to the market.74 Therefore, the Commission considers that the Parties' activities overlap irrespective of Teva's decision to delist the product.

Hydrochlorothiazide/valsartan (C9D)

(90) For hydrochlorothiazide/valsartan, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined volume market share was high, above [50-60]% over the last three years. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market.75

Levofloxacin (J1G)

(91) For levofloxacin, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined value and volume market share was high, in particular up to [60-70]% for pharmaceutical form A and [70-80]% for pharmaceutical form F in volume. For both pharmaceutical forms, only two competitors with a market share above 5% in 2014 would remain on the market. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market.76

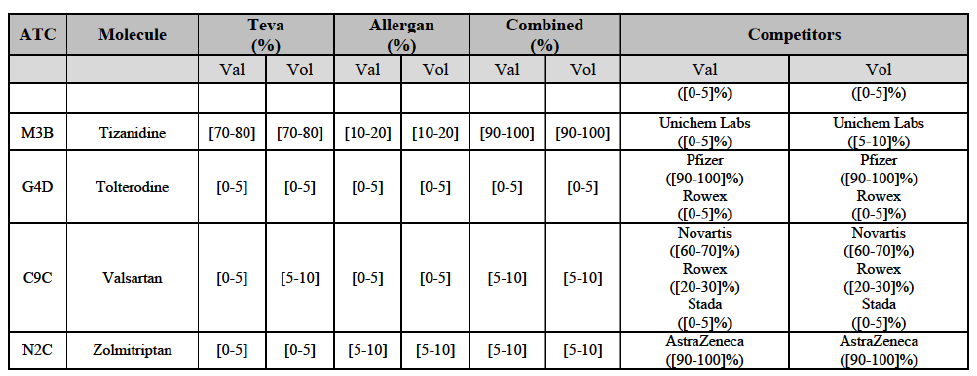

Tizanidine (M3B)

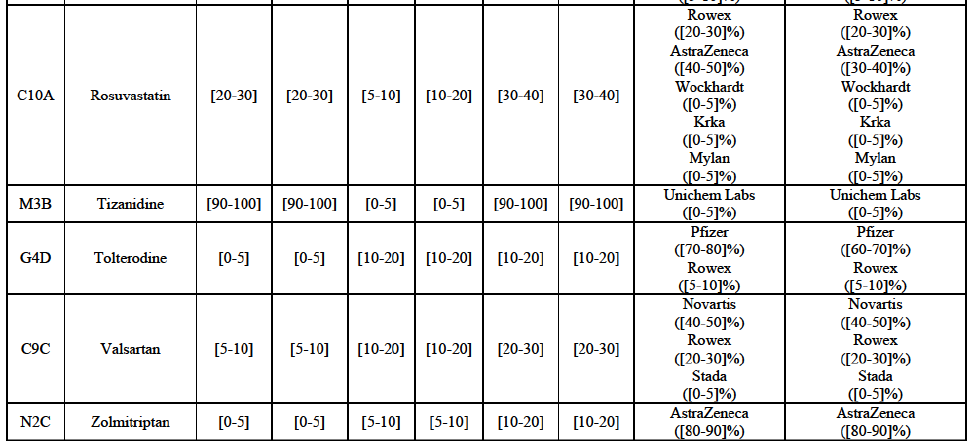

(92) For tizanidine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was >[90-100]% in value and volume, with a significant increment (above [30-40]%). Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market.77

Valsartan (C9C)

(93) For valsartan, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was high in value and volume over the last three years, ranging between [40-50]% and [60-70]%. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market.78

Verapamil (C8A)

(94) For verapamil, the Transaction gives rise to a Group 1 market at the level of the pharmaceutical form B. The combined market share of the Parties was above [50-60]% in volume over the last three years. Only two competitors, including the originator, would remain on the market. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market and that it would be difficult for customers to switch to alternative suppliers.79

Zoledronic Acid (M5B)

(95) For zoledronic acid, the Transaction gives rise to a Group 1 market at molecule level. The Parties recently entered and achieved in two years a combined market share of [3040]% in value and [40-50]% in volume, with a significant increment ([5-10]% in value and [10-20]% in volume). Only two competitors with a market share above 5% would remain on the market, one of them being the originator. Finally, the market investigation indicated that the Transaction would have a negative impact in the market and that it would be difficult to switch to alternative suppliers.80

(96) The Notifying Party submits that the molecule zoledronic acid has been delisted by Teva prior to the announcement of the Transaction. However, Teva's marketing authorisation is still valid, and the Parties acknowledge that it would therefore take up to six months only to come back to the market.81 Therefore, the Commission considers that the Parties' activities overlap irrespective of Teva's decision to delist the product.

Conclusion

(97) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the marketing of alendronic acid, betahistine, carbamazepine, carboplatin, gliclazide, hydrochlorothiazide/valsartan, levofloxacin, tizanidine, valsartan, verapamil and zoledronic acid in Bulgaria.

IV.2.2.4.b. Pipeline generic pharmaceuticals

(98) The Transaction does not raise serious doubts as to its compatibility with the internal market with respect to pipeline generic pharmaceuticals in Bulgaria.

IV.2.2.5. Croatia

IV.2.2.5.a. Marketed generic pharmaceuticals

(99) The following tables present the market shares of the Parties and their main competitors in 2012, 2013 and 2014 for the Group 1/1+/2 markets for which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market.

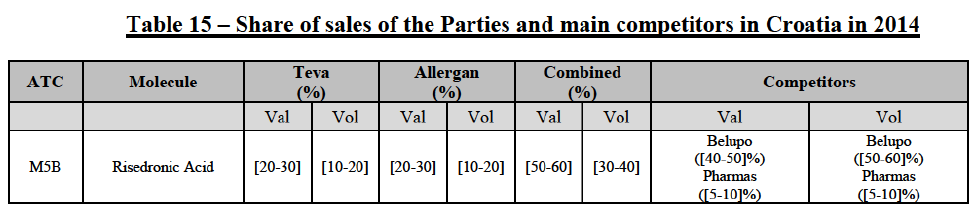

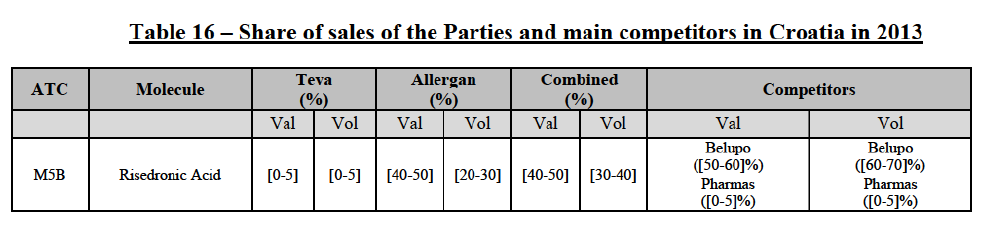

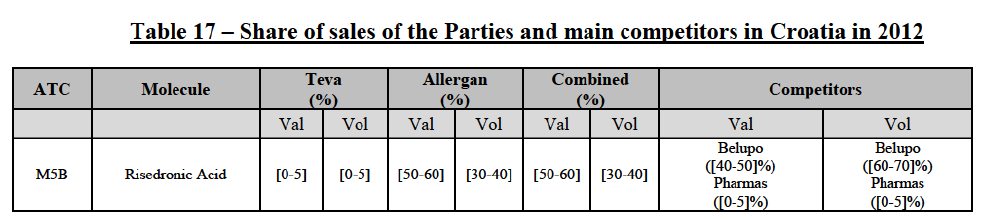

Risedronic Acid (M5B)

(100) For risedronic acid, the Transaction gives rise to a Group 1 market at molecule level. Allergan Generics is the originator of this molecule. The Parties' combined market share was high, above[50-60]% in value in 2014, and only two competitors with a market share above 5% would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position in value.82

Conclusion

(101) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the marketing of risedronic acid in Croatia.

IV.2.2.5.b. Pipeline generic pharmaceuticals

[...]

(102) Allergan Generics is planning to launch a generic [...] (pharmaceutical form [...]), for which Teva had a >[90-100]% market share in volume ([20-30]% in value) in 2014.

[...]

(103) Allergan Generics is planning to launch a generic [...] (pharmaceutical form [...]), for which Teva had [90-100]% of the market in 2014 on the same pharmaceutical form.

Conclusion

(104) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the markets for the marketing of [...] and [...]in Croatia.

IV.2.2.6. Czech Republic

IV.2.2.6.a. Marketed generic pharmaceuticals

(105) The following tables present the market shares of the Parties and their main competitors in 2012, 2013 and 2014 for the Group 1/1+/2 markets for which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market.

(106) The Commission presents below the competitive analysis on these markets, at molecule level, indicating also the ATC3 class to which it belongs, with a possible distinction by pharmaceutical form (at NFC1 level) and between prescribed and OTC sales where relevant.

Alendronic Acid (M5B)

(107) For alendronic acid, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market shares in value and volume were high in the last three years, ranging from [40-50]% to [40-50]%, with a significant increment (>[10-20]%). Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market and that it would be difficult for customers to switch to alternative suppliers.83

Docetaxel (L1C)

(108) For docetaxel, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was high over the last three years in value and in volume, ranging from [40-50]% to [60-70]%. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market.84

Conclusion

(109) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction does raise serious doubts as to its compatibility with the internal market with respect to the marketing of alendronic acid and docetaxel in Czech Republic.

IV.2.2.6.b. Pipeline generic pharmaceuticals

[...]

(110) Allergan Generics is planning to launch a generic [...] (pharmaceutical form [...]), for which Teva had a [60-70]% market share in value and [70-80]% in volume in 2014, and only one other competitor was active on the market in 2012-2014.

Conclusion

(111) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the markets for the marketing of [...] in Czech Republic.

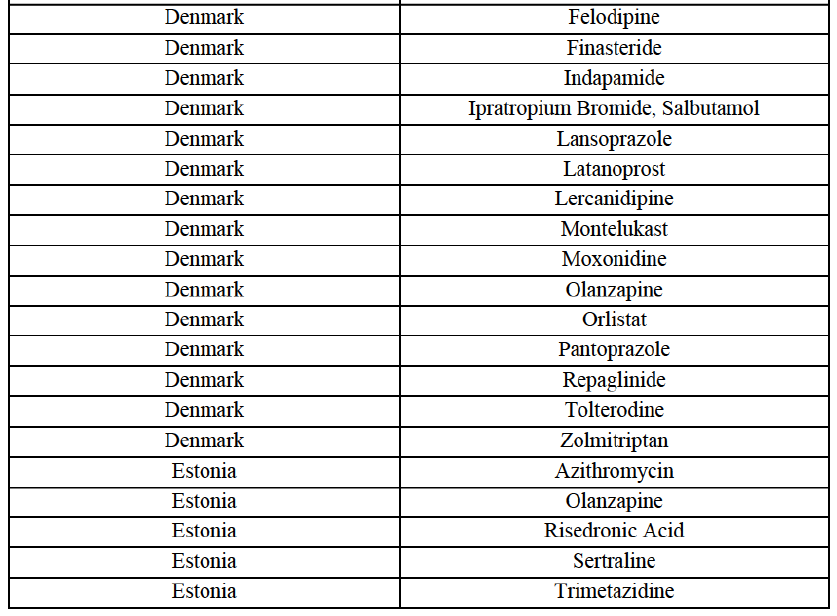

IV.2.2.7. Denmark

IV.2.2.7.a. Marketed generic pharmaceuticals

(112) The following tables present the market shares of the Parties and their main competitors in 2012, 2013 and 2014 for the Group 1/1+/2 markets for which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market.

(113) The Commission presents below the competitive analysis on these markets, at molecule level, indicating also the ATC3 class to which it belongs, with a possible distinction by pharmaceutical form (at NFC 1 level) and between prescribed and OTC sales where relevant.

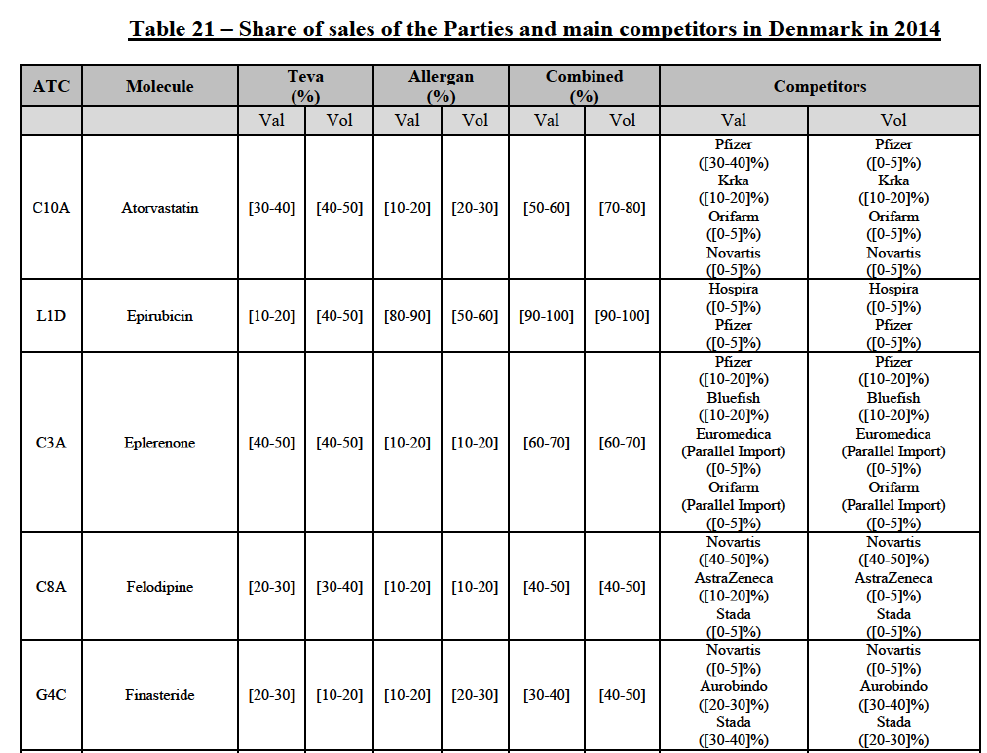

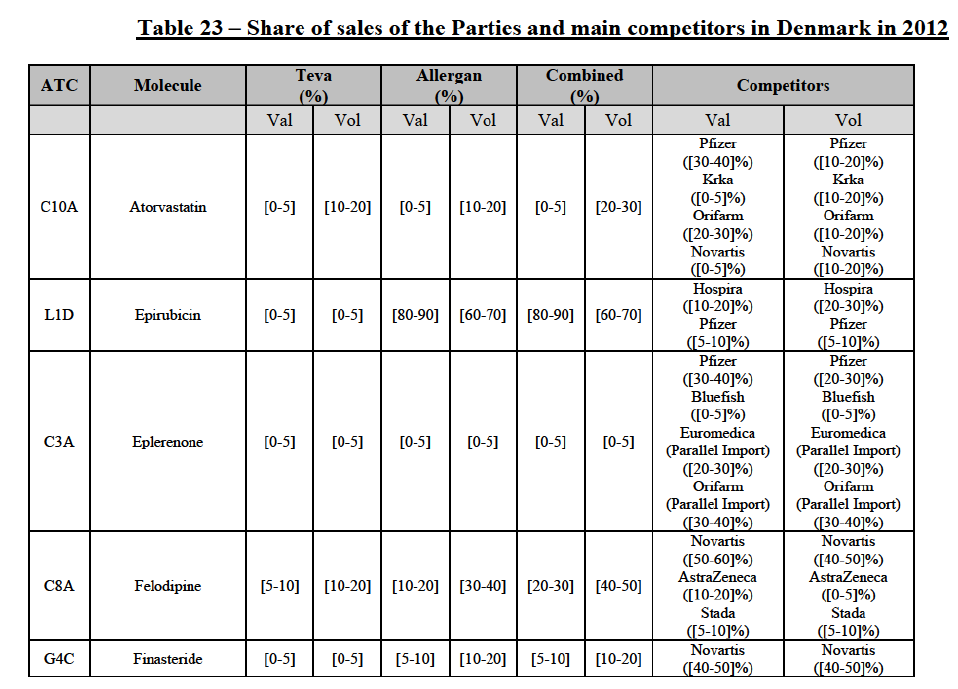

Atorvastatin (C10A)

(114) For atorvastatin, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market shares increased over the last three years, up to [50-70]% in value and [70-801% volume in 2014, with a significant increment from Allergan Generics' market share. Only one competitor with a market share above 5% in value and volume in 2014 would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.85

Epirubicin (L1D)

(115) For epirubicin, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was >[90-100]% in value and volume in 2014, with a significant increment from Teva's market share ([10-20]% in value and [40-50]% in volume). There would be no remaining competitor with a market share above 5%. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.86

Eplerenone (C3A)

(116) For eplerenone, the Transaction gives rise to a Group 1 market at molecule level. The Parties recently entered (in 2013) and achieved a combined market shares of [60-70]% in value and [60-70]% in volume in 2014, with a significant increment from Allergan Generics' market share. Only two competitors with market share above 5% would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.87

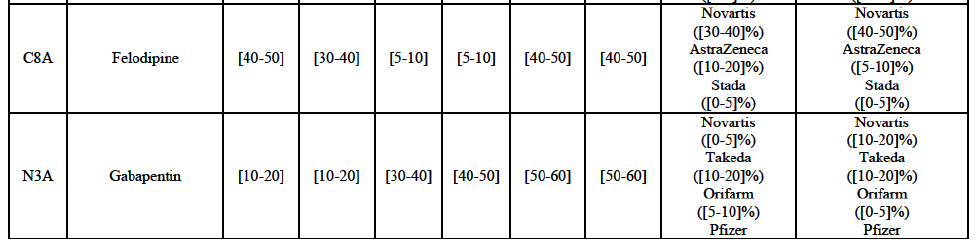

Felodipine (C8A)

(117) For felodipine, the Transaction gives rise to a Group 1 market at molecule level. The Parties’ combined market shares increased over the last three years, up to [40-50]% in value (which would lead to the merged entity being number 1) and [40-50]% in volume in 2014, with a significant increment from Allergan Generics' market share. Only one competitor with a market share above 5% in volume would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.88

Finasteride (G4C)

(118) For finasteride, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market shares fluctuate over the years, up to [50-60]% in value and [50-60]% in volume in 2013. In 2014, the merged entity would still be the number 1 player, with only two remaining competitors with market share above 5%. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.89

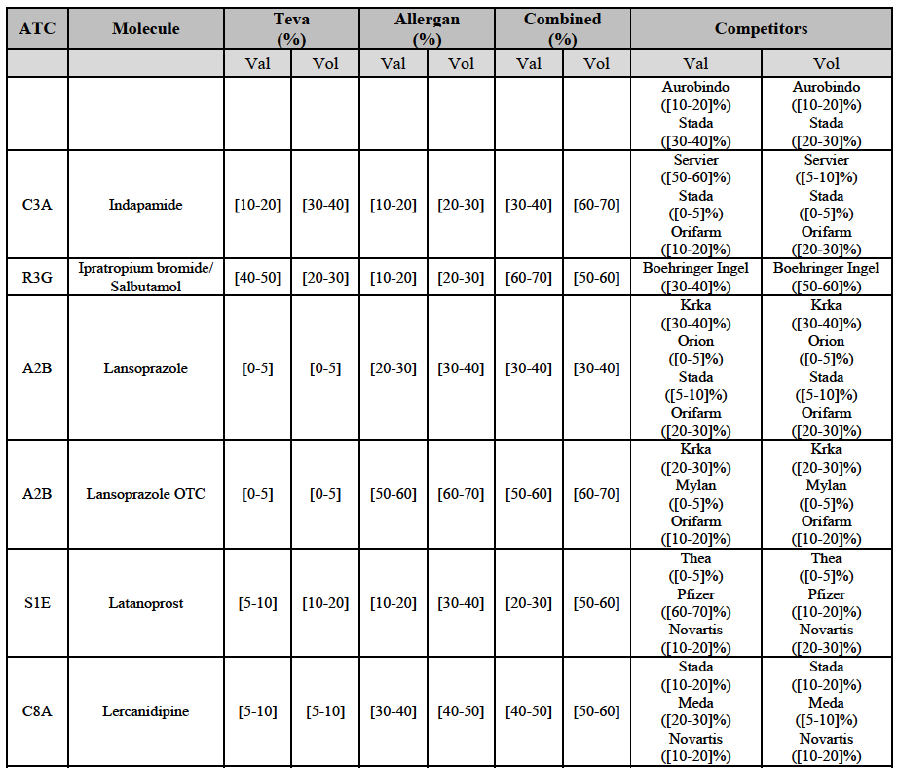

Indapamide (C3A)

(119) For indapamide, the Transaction gives rise to a Group 1 market at molecule level. The Parties’ combined market shares increased over the last three years, up to [50-60]% in value, [70-80]% in volume in 2014, with a significant increment from Allergan Generics' market share. Only one competitor with a market share above 5% in volume would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.90

Ipratropium bromide/Salbutamol (R3G)

(120) For ipratropium bromide/salbutamol, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was [60-70]% in the last three years in value and in 2014 in volume. It is a respiratory product for which Teva enjoys a very strong market position (market share between [20-30]% and [60-70]% in the last three years) and for which Allergan Generics also has a significant position (up to [20-30]% in volume in 2012). Only one competitor, the originator Boehringer Ingelheim, would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.91

Lansoprazole (A2B)

(121) For lansoprazole, the Transaction gives rise to a Group 1 market at molecule level. The Parties’ combined market share was high, in particular in the OTC segment where it ranged from [40-50] to [60-70]% over the last three years. In all possible segments (Rx, OTC or Rx and OTC), only two competitors with a market share above 5% would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.92

Latanoprost (S1E)

(122) For latanoprost, the Transaction gives rise to a Group 1 market at the level of the pharmaceutical form N. The Parties entered in 2012 and their market shares have fluctuated over the last three years. The combined entity was number 1 player with [5060]% of combined market share based on 2012 data in volume. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.93

Lercanidipine (C8A)

(123) For lercanidipine, the Transaction gives rise to a Group 1 market at molecule level. The Parties’ combined market shares increased over the last three years, up to [50-60]% in value and [60-70]% in volume in 2014. The merged entity would by far lead the market, with only two remaining competitors, including the originator Meda, with a market share above 5% in both value and volume. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.94

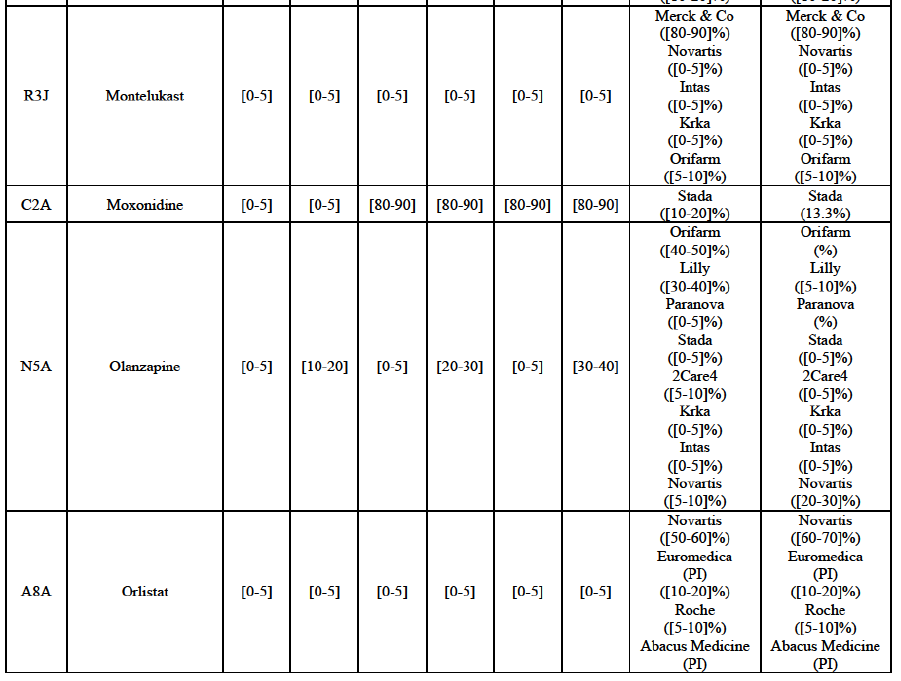

Montelukast (R3J)

(124) For montelukast, the Transaction gives rise to a Group 1 market at molecule level. The Parties recently entered (in 2013) and achieved a combined market share of [30-40]% in volume in 2014, with a significant increment from Teva's market share at [10-20]%. [...]. Based on 2014 data, only two competitors with a market share above 5% in volume would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.95

Moxonidine (C2A)

(125) For moxonidine, the Transaction gives rise to a Group 1 market at molecule level. The Parties’ combined market share was above [50-60]% in value and volume in the last three years. Only one competitor would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.96

Olanzapine (N5A)

(126) For olanzapine, the Transaction gives rise to a Group 1 market at molecule level. Olanzapine became off-patent in September 2011. The Parties' combined market share was above [60-70]% in volume in 2013 and [50-60]% in volume in 2014. The average prices reported by IMS for this molecule would have increased between 2012 and 2014 by [130-140]%. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.97

Orlistat (A8A)

(127) For orlistat, the Transaction gives rise to a Group 1 market at molecule level. The Parties recently entered the market (in 2012) and had a combined market share of [3040]% in value and volume in 2014, with a significant increment. In the segment for Rx, the Parties' combined market was [80-90] and [80-90]% in value and volume in 2014. Only one competitor with a market share above 5% would remain. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.98

(128) The Notifying Party submits that the molecule orlistat has been delisted by Teva prior to the announcement of the Transaction. However, Teva's marketing authorisation is still valid, and the Parties acknowledge that it would therefore take up to six months only to come back to the market.99 The Commission considers that the Parties' activities overlap irrespective of Teva's decision to delist the product.

Pantoprazole (A2B)

(129) For pantoprazole, the Transaction gives rise to a Group 1 market at molecule level. The Parties entered recently the market and acquired high combined market shares in two years, ranging from [5-10]% to [50-60]% in value. Only two competitors with a market share above 5%, including the originator Takeda, would remain on the market. In the segment for OTC only, the Parties are the only two generics with significant shares challenging the originator. The market investigation did not bring elements to dispel the strong competitive position of the Parties combined.100

Repaglinide (A10M)

(130) For repaglinide, the Transaction gives rise to a Group 1 market at molecule level. The Parties recently entered (in 2013) and achieved a combined market share of [40-50]% in value and [80-90]% in volume in 2014, with a significant increment from Allergan Generics' market share. Only one remaining competitor (Novo Nordisk, the originator) has a market share above 5% in value and volume. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.101

(131) The Notifying Party submits that the molecule repaglidine has been delisted by Allergan Generics prior to the announcement of the Transaction. However, Allergan Generics' marketing authorisation is still valid, and the Parties acknowledge that it would therefore take up to six months only to come back to the market.102 Therefore, the Commission considers that the Parties' activities overlap irrespective of Allergan Generics' decision to delist the product.

Tolterodine (G4D)

(132) For tolterodine, the Transaction gives rise to a Group 1 market at molecule level. The Parties recently entered (in 2013) and achieved a combined market shares up to 65.2% in value and 83.8% in volume, with a significant increment from Teva's market share. Only one competitor with a market share above 5% would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.103

(133) The Notifying Party submits that the molecule tolterodine has been delisted by Allergan Generics prior to the announcement of the Transaction. However, Allergan Generics' marketing authorisation is still valid, and the Parties acknowledge that it would therefore take up to six months only to come back to the market. 104 Therefore, the Commission considers that the Parties' activities overlap irrespective of Allergan Generics' decision to delist the product.

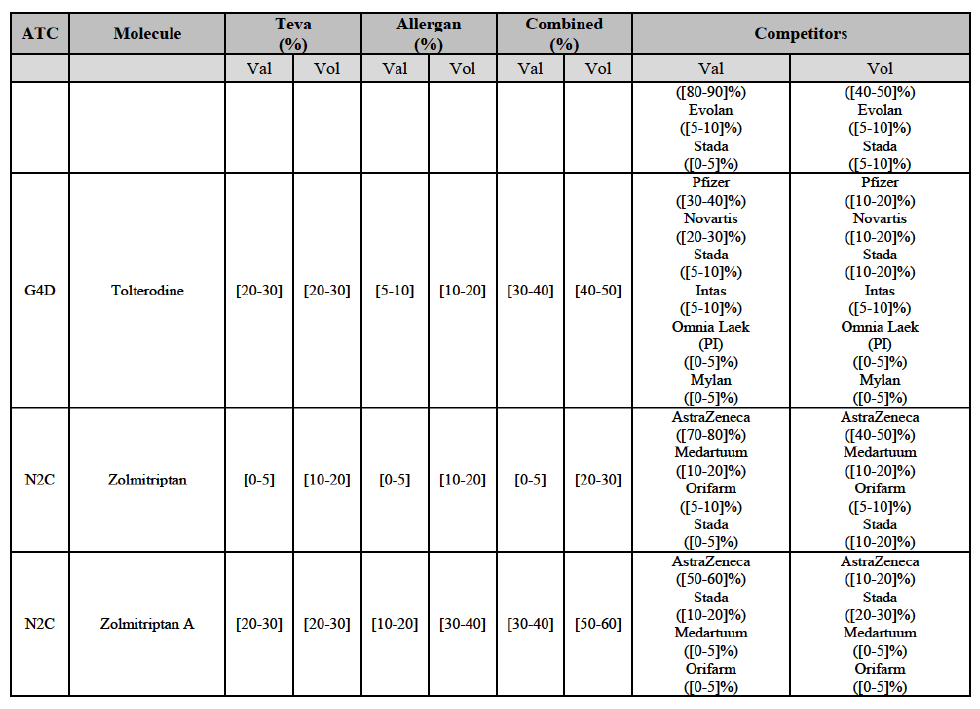

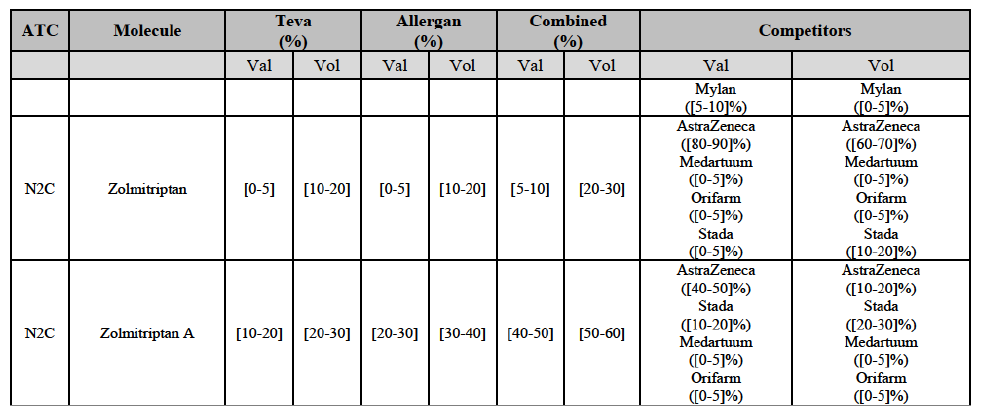

Zolmitriptan (N2C)

(134) For zolmitriptan, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above 60% in volume in 2013 and 2014, with a significant increment from Teva's market share. Only one competitor with a market share above 5% would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.105

Conclusion

(135) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raise serious doubts as to its compatibility with the internal market with respect to the marketing of atorvastatin, epirubicin, eplerenone, felodipine, finasteride, indapamide, ipratropium bromide/salbutamol, lansoprazole, latanoprost, lercanidipine, montelukast, moxonidine, olanzapine, orlistat, pantoprazole, repaglinide, tolterodine and zolmitriptan in Denmark.

IV.2.2.7.b. Pipeline generic pharmaceuticals

[...]

(136) Teva is planning to launch a generic [...] (pharmaceutical form [...]), for which Allergan Generics had a [50-60]% market share in volume ([30-40]% in value) in 2014 on the same pharmaceutical form, and only two other competitors with >5% share in volume were active on the market in 2012-2014.

Conclusion

(137) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the markets for the marketing of [...] in Denmark.

IV.2.2.8. Estonia

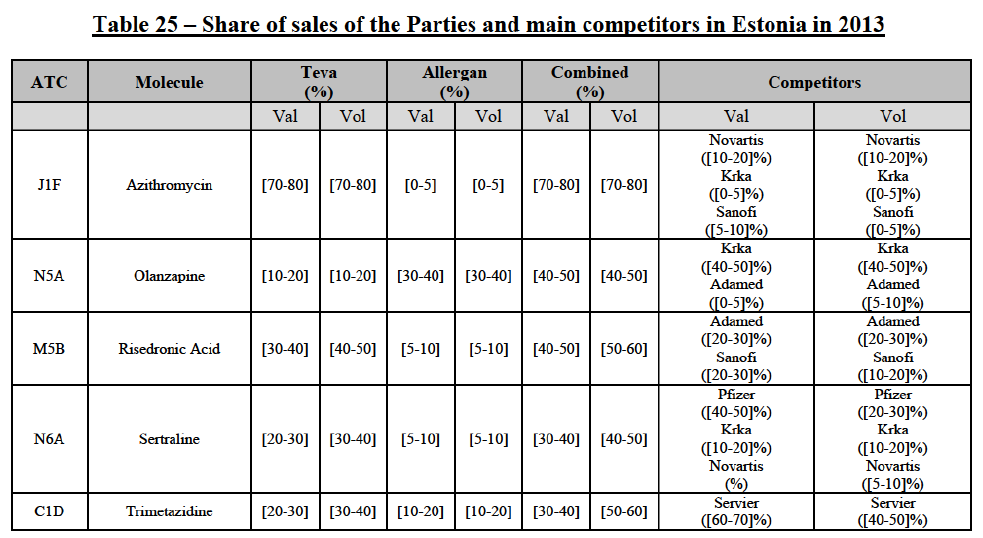

IV.2.2.8.a. Marketed generic pharmaceuticals

(138) The following tables present the market shares of the Parties and their main competitors in 2012, 2013 and 2014 for the Group 1/1+/2 markets for which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market.

(139) The Commission presents below the competitive analysis on these markets, at molecule level, indicating also the ATC3 class to which it belongs, with a possible distinction by pharmaceutical form (at NFC1 level) and between prescribed and OTC sales where relevant.

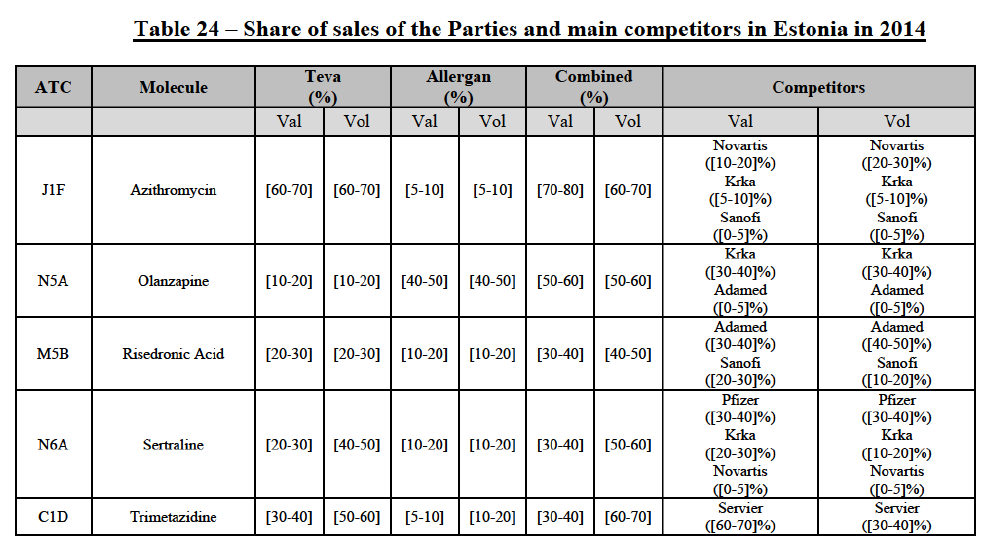

Azithromycin (J1F)

(140) For azithromycin, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was at least [60-70]% in the last three years in value and volume. In 2014, the combined market share of the Parties was [70-80]% in value and [60-70]% in volume, with an increment from Allergen Generics' market share of more than [5-10]%. [...]. Only two competitors with a market share of 5% or above would remain on the market. Furthermore, the market investigation indicated that there would be a negative impact of the Transaction on this molecule.106

Olanzapine (N5A)

(141) For olanzapine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above 50% in 2014 in value (58.6%) and volume ([50-60]%). [...]. Only one competitor with a market share above 5% in value and volume would remain on the market. Furthermore, the market investigation indicated that there would be a negative impact of the Transaction on this molecule.107

Rssedronic Acid (M5B)

(142) For risedronic acid, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above [40-50]% in volume in the last three years, with a significant increment from Allergan Generics' market share. The combined entity was the number 1 player based on 2012-2014 data. Only two competitors with a market share above 5% would remain on the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.108

Sertraline (N6A)

(143) For sertraline, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above 50% in volume in 2014, with a significant increment from Allergan Generics' market share (more than 10%). Only two competitors with a market share above 5%, including the originator (Pfizer), would remain on the market. Furthermore, the market investigation indicated that that there would be a negative impact of the Transaction on this molecule.109

Trimetazidine (C1D)

(144) For trimetazidine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market shares increased over the last three years, up to [60-70]% in volume in 2014. Only one competitor (Servier, the originator) would remain on the market with a market share above 5%. Furthermore, the market investigation indicated that there would be a negative impact of the Transaction on this molecule.110

Conclusion

(145) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the marketing of azithromycin, olanzapine, risedronic acid, sertraline and trimetazidine in Estonia.

IV.2.2.8.b. Pipeline generic pharmaceuticals

[...]

(146) Allergan Generics is planning to launch a generic [...] (pharmaceutical form [...]), for which Teva had a [70-80]% market share in value and [70-80]% in volume in 2014 on the same pharmaceutical form, and only one other competitor with >5% share in volume was active on the market in 2012-2014.

Conclusion

(147) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to the market for the marketing of [...]in Estonia.

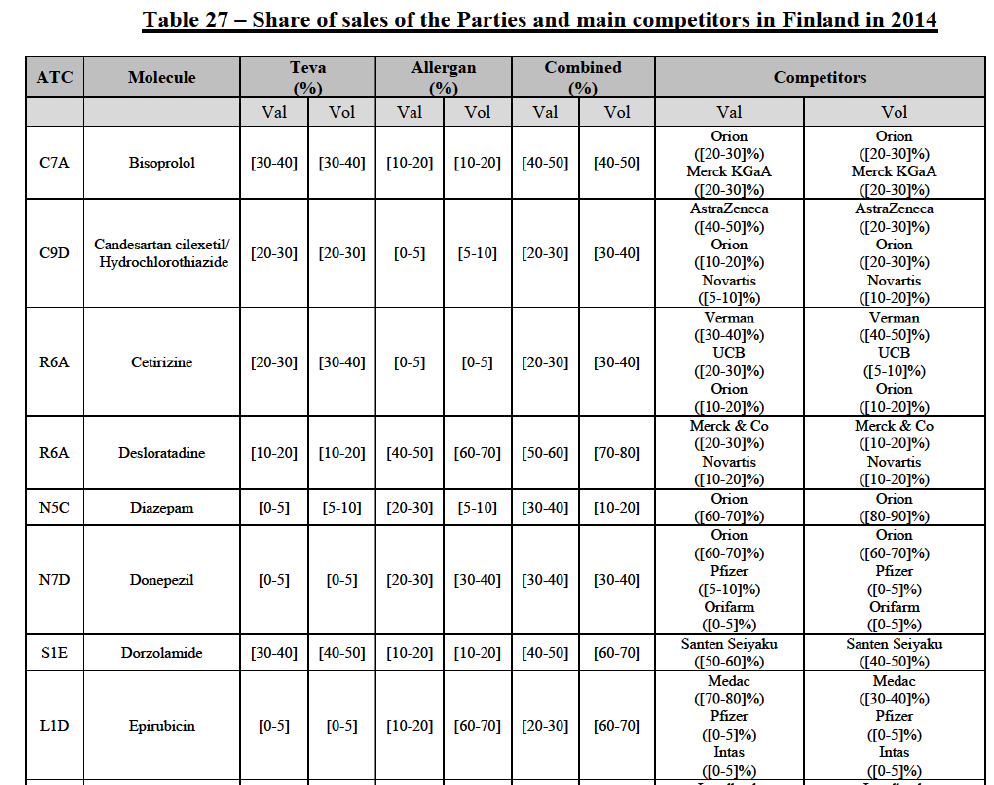

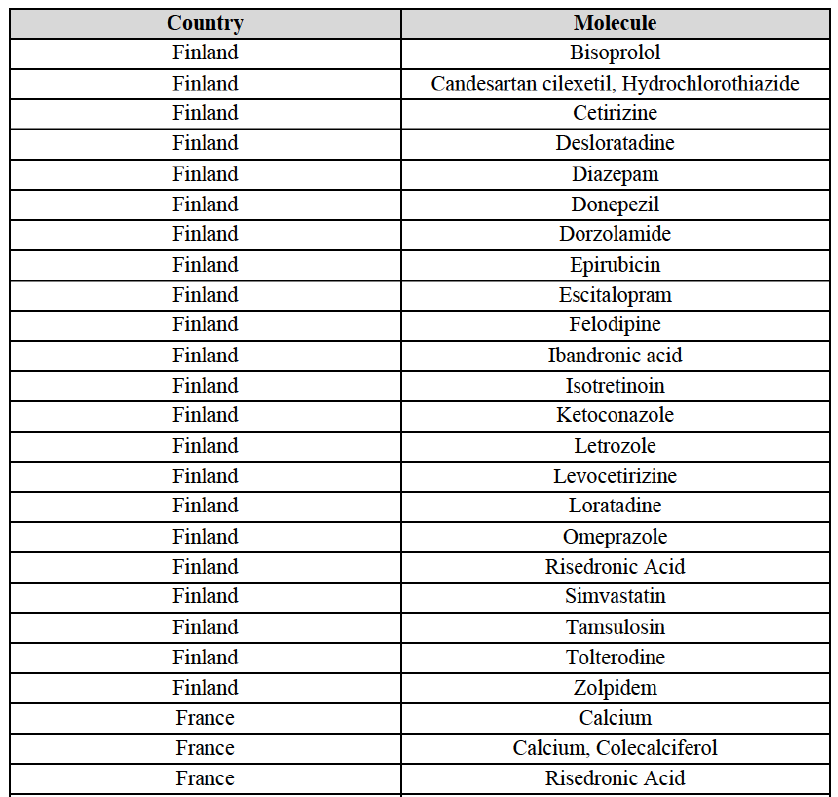

IV.2.2.9. Finland

IV.2.2.9.a. Marketed generic pharmaceuticals

(148) The following tables present the market shares of the Parties and their main competitors in 2012, 2013 and 2014 for the Group 1/1+/2 markets for which the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market.

(149) The Commission presents below the competitive analysis on these markets, at molecule level, indicating also the ATC3 class to which it belongs, with a possible distinction by pharmaceutical form (at NFC1 level) and between prescribed and OTC sales where relevant.

Bisoprolol (C7A)

(150) For bisoprolol, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was between [40-50]% in value and [50-60]% in volume in the last three years, with a significant increment from Allergan Generics market share ([10-20]%). Only two competitors with a market share above 5%, including the originator (Merck KGaA), would remain on the market. Furthermore, the market investigation confirmed the Parties' leading position in this market.

Candesartan cilexetil/Hydrochlorothiazide (C9D)

(151) For candesartan cilexetil/ hydrochlorothiazide, the Transaction gives rise to a Group 1 market at molecule level. The Parties are among a few generic competitors which entered the market following patent expiry in 2012 and had a market share of more than 5% in volume in 2014 (together with Orion and Novartis). Teva was already pre-Transaction the market leader in volume, with a market share of more than [20-30]%. Furthermore, the market investigation confirmed the Parties' leading position in this market.

Cetirizine (R6A)

(152) For cetirizine, the Transaction gives rise to a Group 1 market at molecule level for cetirizine Rx. The Parties' combined market share would be slightly above [30-40]% in 2014. However, only two competitors with a market share above 5% would remain on the market. Furthermore, the market investigation indicated that it would be difficult for customers to switch to alternative suppliers.

Desloratadine (R6A)

(153) For desloratadine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market shares increased in the last three years, up to [50-60]% in value and [70-80]% in volume, with a significant increment from Teva's market share ([10-20]%). [...]. Only two competitors with a market share above 5%, including the originator (Merck & Co), would remain. In the segment for desloratadine in the pharmaceutical form D, the Parties are the only two generic companies active in this market, competing with the originator. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.

Diazepam (N5C)

(154) For diazepam, the Transaction gives rise to a Group 1 market at molecule level in 2012 and 2013. The Parties' combined market share was [30-40]% in value and [10-20]% in volume. Although the combined market share seems moderate, only one competitor, the originator Orion, would remain on the market with a market share above 5%. The market investigation did not bring elements to dispel the strong competitive position of the Parties combined.

Donepezil (N7D)

(155) For donepezil, the Transaction gives rise to a Group 1 market at molecule level in 2012 and 2013. The Parties' combined market shares ranged from [30-40]% to [50-60]% in value and [30-40]% to [60-70]% in volume in the last three years. In 2014, only one competitor had a market share above 5% in value and volume. The market investigation did not bring elements to dispel the strong competitive position of the Parties combined.

Dorzolamide (S1E)

(156) For dorzolamide, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market shares was [40-50]% in value and [60-70]% in volume in 2014, with a significant increment (more than [10-20]%). Only one competitor with a market share above 1%, the originator, would remain in the market. The market investigation did not provide any elements to dispel the serious doubts arising from the fact that the Parties have a strong combined competitive position.

Epirubicin (L1D)

(157) For epirubicin, the Transaction gives rise to a Group 1 market at molecule level in 2012 and 2013. The Parties' combined market share was, in volume, 50% in 2012 (with an increment of [10-20]%), [40-50]% in 2013 (with an increment of [20-30]%) and [6070]% in 2014 (with an increment of less than [0-5]%). The fluctuation of market shares can be due to the hospitals' tendering system since epirubicin is an oncology product sold to hospitals. Over the last three years, only two competitors with a market share above 5% were active on this market. The market investigation did not bring elements to dispel the strong competitive position of the Parties combined.

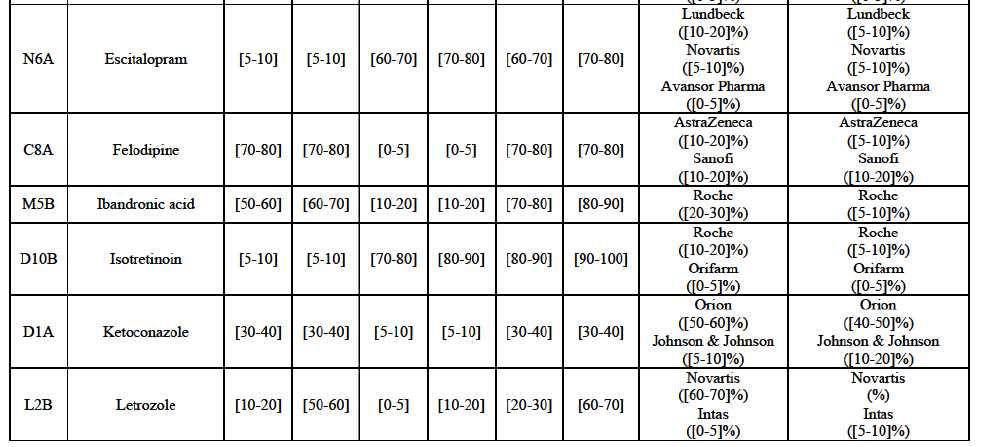

Escitalopram (N6A)

(158) For escitalopram, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share increased over the last three years, up to [60-70]% in value and [70-80]% in volume in 2014. Only two competitors having a market share above 5% in 2014 would remain on the market. Furthermore, the market investigation indicated that the combined share of the Parties would be higher than the Notifying Party's estimate, possibly above [80-90]%, and that there would be a negative impact of the Transaction on this molecule.

Felodipine (C8A)

(159) For felodipine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above [70-80]% in 2014 ([70-80]% in value and [70-80]% in volume). Only two competitors, being the originators (AstraZeneca and Sanofi), have a market share above 5%. The market investigation did not bring elements to dispel the strong competitive position of the Parties combined.

Ibandronic Acid (M5B)

(160) For ibandronic acid, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was [70-80]% in value and [80-90]% in volume in 2014 with a significant increment from Allergan Generics ([10-20]%). Only one competitor (the originator) with a market share above 5% would remain on the market. The market investigation did not bring elements to dispel the strong competitive position of the Parties combined.

Isotretinoin (D10B)

(161) For isotretinoin, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was [80-90]% in value and [90-100]% in volume in 2014, with an increment of [5-10]% in value and [5-10]% in volume. Only one competitor, the originator Roche, would remain in the market with a market share above 5%. Furthermore, the market investigation indicated that there would be a negative impact of the Transaction on this molecule.

Ketoconazole (D1A)

(162) For ketoconazole, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was [30-40]% in value and [30-40]% in volume in 2014. The Parties are the only two generic companies active in this market, the only remaining competitor being the originator, Johnson & Johnson. The market investigation did not bring elements to dispel the strong competitive position of the Parties combined.

Letrozole (L2B)

(163) For letrozole, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share increased in the last three years, up to [60-70]% in volume, with an increment of more than [10-20]%. Only one competitor, the originator (Novartis), would have a market share above 5% in value. Furthermore, the market investigation the market investigation confirmed the Parties' leading position in this market (above 60%) and the possible negative impact of the Transaction.

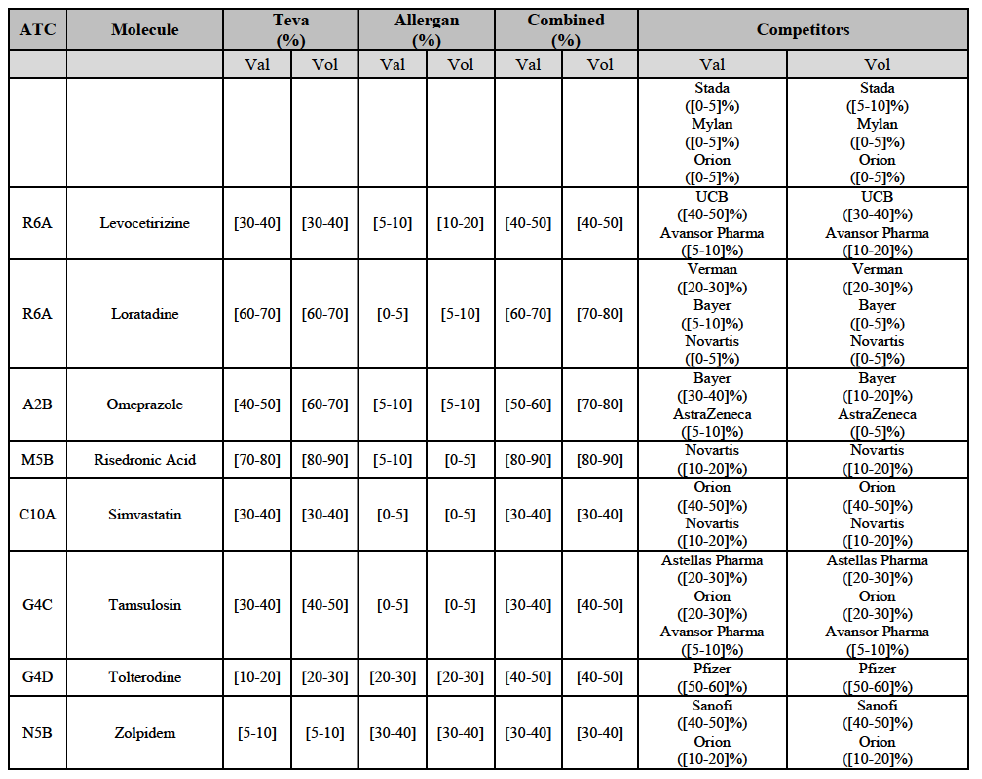

Levocetirizine (R6A)

(164) For levocetirizine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was between [40-50]% and [40-50]% in value and between [40-50]% and [50-60]% in volume, with a significant increment (more than [510]% in 2014). Only two competitors with a market share above 5%, including the originator (UCB), would remain in the market, and only one, the originator, for levocetirizine sold OTC. Furthermore, the market investigation indicated that the combined share of the Parties would be higher than the Notifying Party's estimate, possibly above 70%, and that there would be a negative impact of the Transaction on this molecule.

Loratadine (R6A)

(165) For loratadine, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was [60-70]% in value and [70-80]% in volume in 2014. Only one competitor with a market share above 5% in value and volume would remain in the market. Furthermore, the market investigation confirmed the strong combined position of the Parties and indicated that it would be difficult for customers to switch to alternative suppliers.

Omeprazole (A2B)

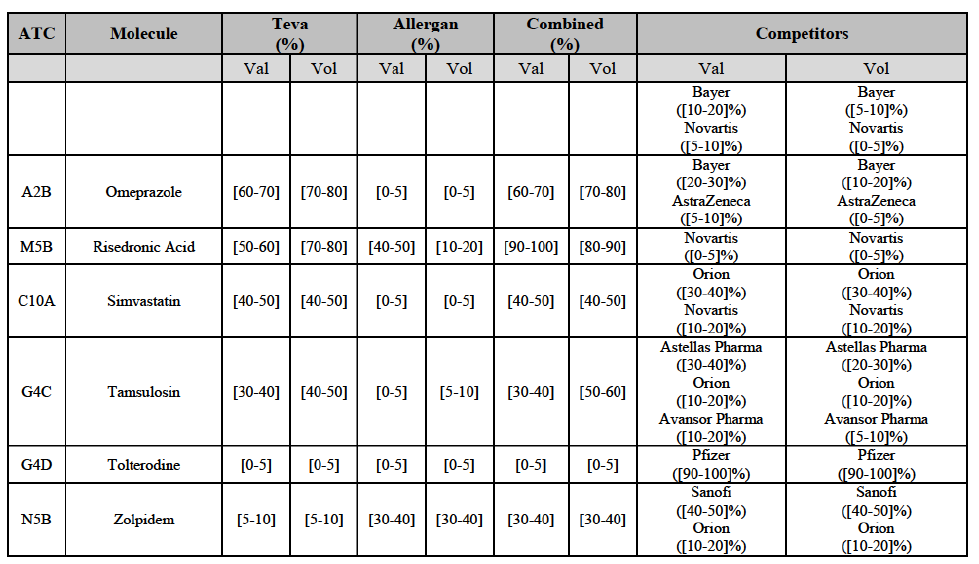

(166) For omeprazole, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share was above [50-60]% in value and [70-80]% in volume in the last three years, with an increment from Allergan Generics growing over the years. Only one competitor, Bayer (one of the two originators), would remain with a market share above 5% in value and volume. The Parties are both active in the Rx and OTC segments. The combined market share of the Parties was even higher for omeprazole Rx, with [80-90]% in value and [90-100]% in volume and only one competitor, the originator, would remain post-Transaction for omeprazole OTC. Furthermore, the market investigation indicated that the Transaction would have a negative impact in the market and that it would be difficult to switch to alternative suppliers.

Risedronic Acid (M5B)

(167) For risedronic acid, the Transaction gives rise to a Group 1 market at molecule level. Allergan Generics is the originator of this molecule. The Parties' combined market shares was [80-90]% in value and [80-90]% in volume in 2014. Only one competitor with a market share above 5% would remain in the market. Furthermore, the market investigation the market investigation confirmed the Parties' leading position in this market (above 90%) and the possible negative impact of the Transaction.

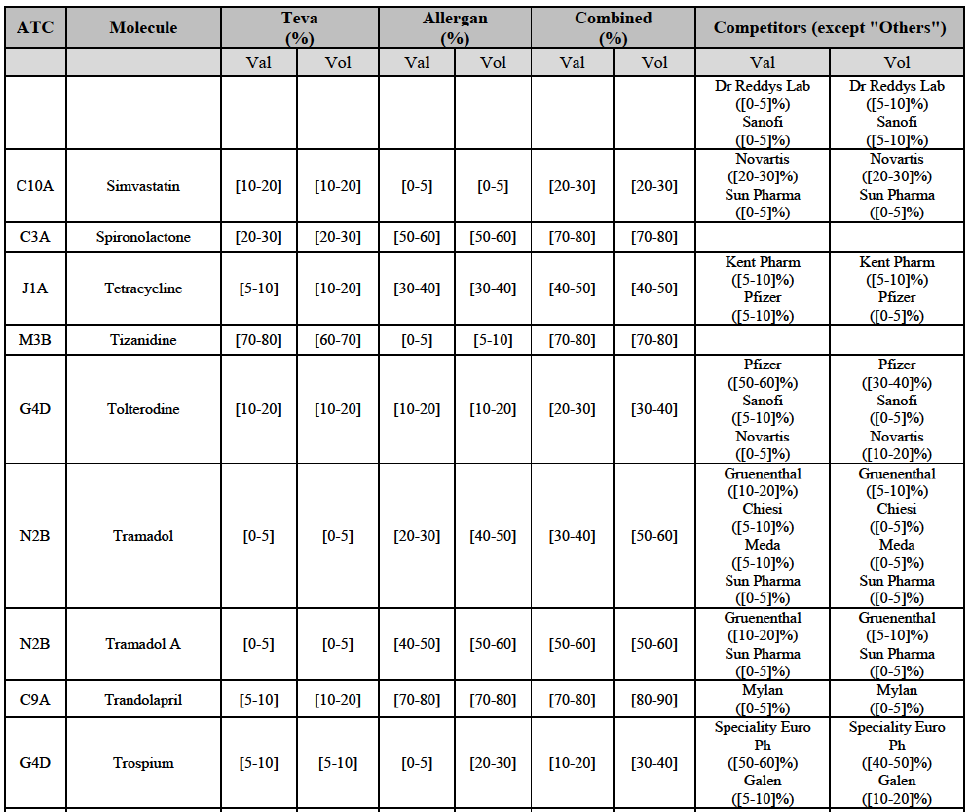

Simvastatin (C10A)

(168) For simvastatin, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share ranged between [30-40]% to [40-50]% in the last three years in value and volume. [...]. Only two competitors with a market share above 5% would remain on the market. The average prices reported by IMS for simvastatin increased by 86% between 2012 and 2014. Furthermore, the market investigation indicated that the Transaction would have a negative impact in this market and that it would be difficult to switch to alternative suppliers.

Tamsulosin (G4C)

(169) For tamsulosin, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market share in the last three years was between [30-40]%-[40-50]% in value and [40-50]%-[50-60]% in volume, with Teva being the market leader. Furthermore, the market investigation confirmed the Parties' leading position in this market and the possible negative impact of the Transaction.

Tolterodine (G4D)

(170) In tolterodine, the Transaction gives rise to a Group 1 market at molecule level. The Parties recently entered (in 2013) and achieved a combined market share of [40-50]% value and [40-50]% in volume at molecule level and [40-50]% value and [40-50]% in volume at the level of the pharmaceutical form B. For all possible segments, the increment of market share is significant (around [20-30]%). In addition, there will be only one remaining competitor with a market share above 5%, which is the originator Pfizer. Finally, the market investigation confirmed the Parties' leading position in this market (possibly above 50%) and the possible negative impact of the Transaction.

Zolpidem (N5B)

(171) For zolpidem, the Transaction gives rise to a Group 1 market at molecule level. The Parties' combined market shares was [30-40]% in value and [30-40]% in volume in 2014. Only two competitors, including the originator, have a market share above 5%. Allergan Generics was the leading generic supplier over the last three years. Furthermore, the market investigation indicated that the combined share of the Parties would be higher than the Notifying Party's estimate, possibly more than [70-80]%, and that there would be a negative impact of the Transaction on this molecule.

Conclusion

(172) In view of the above and of all the evidence available to the Commission, the Commission considers that the Transaction raises serious doubts as to its compatibility with the internal market with respect to bisoprolol, candesartan cilexetil/ hydrochlorothiazide, cetirizine, desloratadine, diazepam, donepezil, dorzolamide, epirubicin, escitalopram, felodipine, ibandronic acid, isotretinoin, ketoconazole, letrozole, loratadine, omeprazole, risedronic acid, simvastatin, tamsulosin, tolterodine and zolpidem in Finland.

IV.2.2.9.b. Pipeline generic pharmaceuticals

(173) The Transaction does not raise serious doubts as to its compatibility with the internal market with respect to pipeline generic pharmaceuticals in Finland.

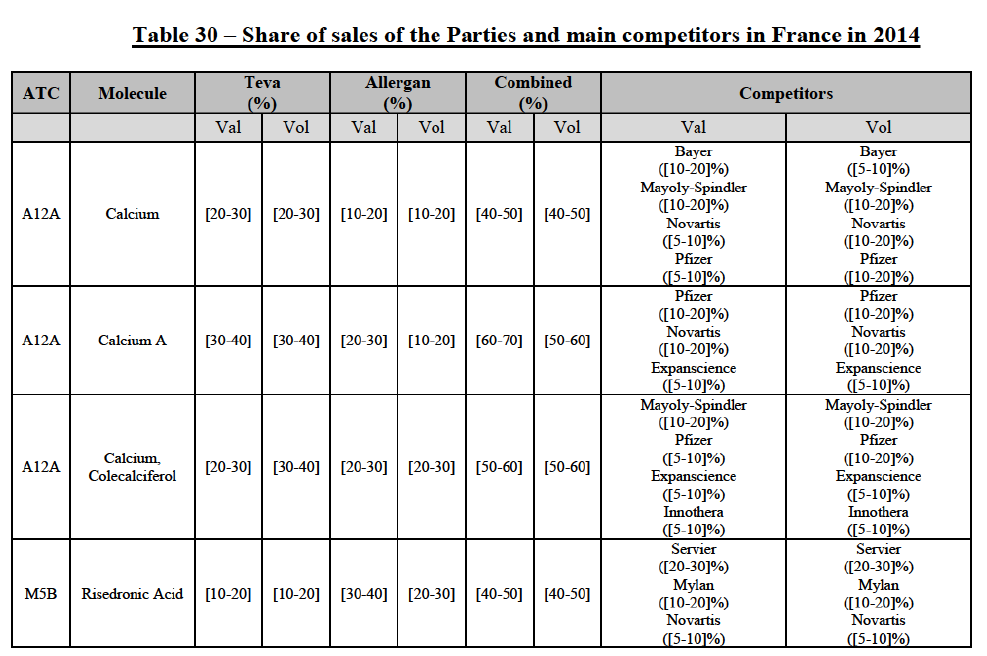

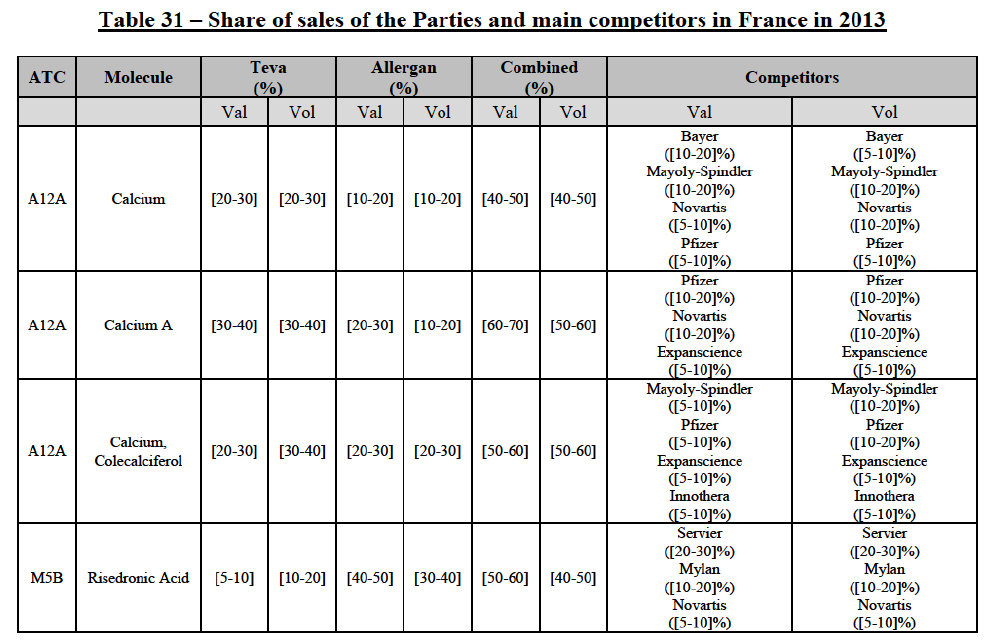

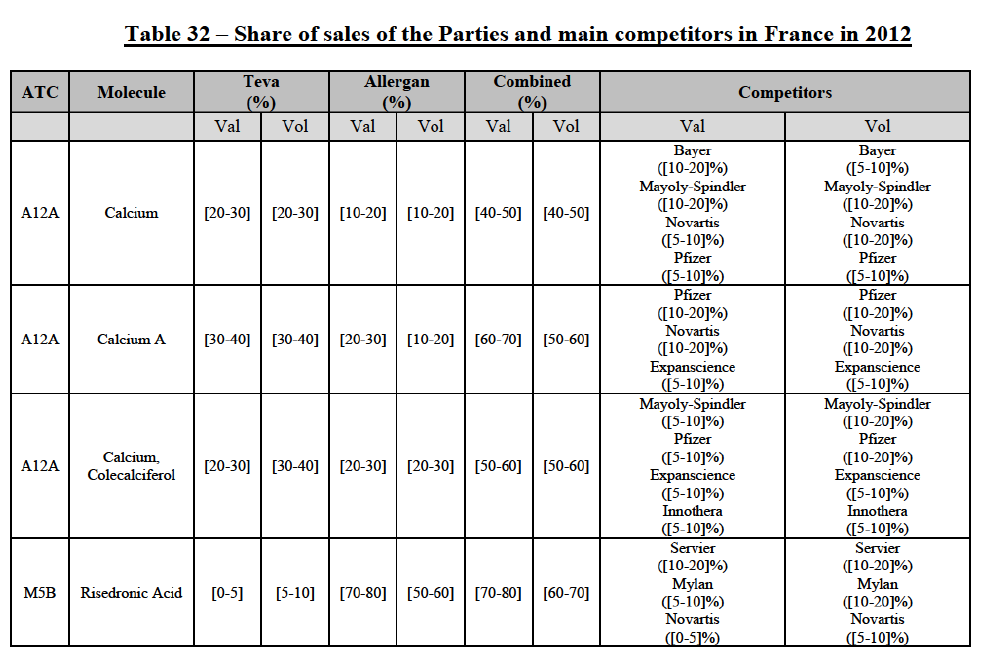

IV.2.2.10. France

IV.2.2.10.a. Marketed generic pharmaceuticals