Commission, 21 décembre 2020, n° M.9730

COMMISSION EUROPÉENNE

Décision

FCA/PSA

COMMISSION DECISION

of 21.12.2020

declaring a concentration to be compatible with the internal market and the EEA agreement

THE EUROPEAN COMMISSION,

Having regard to the Treaty on the Functioning of the European Union,

Having regard to the Agreement on the European Economic Area, and in particular Article 57 thereof,

Having regard to Council Regulation (EC) No 139/2004 of 20.1.2004 on the control of concentrations between undertakings1, and in particular Article 8(2) thereof,

Having regard to the Commission's decision of 17.06.2020 to initiate proceedings in this case,

Having given the undertakings concerned the opportunity to make known their views on the objections raised by the Commission,

Having regard to the opinion of the Advisory Committee on Concentrations,

Having regard to the final report of the Hearing Officer in this case,

Whereas:

1. INTRODUCTION

(1) On 8 May 2020 the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (the ‘Merger Regulation’) by which Peugeot S.A. (‘PSA’, France) and Fiat Chrysler Automobiles N.V. (‘FCA’, the Netherlands), controlled by EXOR N.V. would enter into a full merger within the meaning of Article 3(1)(a) of the Merger Regulation.2 PSA and FCA are designated in this Decision as the ‘Notifying Parties’ or ‘Parties’ to the ‘Proposed Transaction’.

2. THE OPERATION AND THE CONCENTRATION

(2) PSA is active worldwide in the manufacture, supply and distribution of passenger cars (‘PCs’) and light commercial vehicles (‘LCVs’) under the Peugeot, Citroën, Opel, Vauxhall and DS brands. Through its subsidiary, Faurecia S.A. (‘Faurecia’), it is also active in the manufacture and supply of various automotive components. PSA also provides ancillary services such as financing solutions for the acquisition of its branded motor vehicles,3 as well as mobility services and solutions.

(3) FCA is active worldwide in the manufacture, supply and distribution of PCs and LCVs under the brands Fiat, Chrysler, Jeep, Alfa Romeo, Lancia, Abarth, Dodge, Ram, and Fiat Professional. In addition, FCA owns the automotive cast components business Teksid S.p.A., the plastic components and modules business Plastic Components and Modules Automotive S.p.A., and the industrial automation business Comau S.p.A. It also provides financing solutions to support the sale of its branded vehicles.

(4) Pursuant to the Combination Agreement signed on 17 December 2019, on the date of closing, all issued and outstanding PSA and FCA shares will be exchanged for shares of a newly incorporated entity based in the Netherlands according to the exchange rate agreed between the Parties.4 The Combination Agreement was amended on 14 September 2020. The amendments were however economic in nature in light of the impact of the Covid-19 pandemic, but did not affect the structure or scope of the merger.5 Since the Proposed Transaction consists of the merger of two previously independent undertakings, it constitutes a concentration pursuant to Article 3(1)(a) of the Merger Regulation.

3. EU DIMENSION

(5) The combined aggregate worldwide turnover of the undertakings concerned exceeds EUR 5 000 million (FCA: EUR 110 412 million; PSA:6 EUR 74 027 million) and the aggregate Union-wide turnover of each of FCA and PSA is above EUR 250 million (FCA: EUR [...]; PSA: EUR [...]). The Parties do not each achieve more than two third of their aggregate Union-wide turnover within one and the same Member State.

(6) It follows that the Proposed Transaction meets the turnover thresholds within the meaning of Article 1(2) of the Merger Regulation.

4. THE PROCEDURE

(7) On 8 May 2020 the Commission received a notification of the Proposed Transaction pursuant to Article 4 of the ‘Merger Regulation’.

(8) During the Phase I market investigation the Commission reached out to a large number of market participants (customers of the Notifying Parties and competitors), by requesting information through e-Questionnaires, telephone calls and written requests for information pursuant to Article 11 of the Merger Regulation.

(9) In addition, the Commission also sent numerous written requests for information to the Notifying Parties and reviewed internal documents of the Parties submitted at this stage.

(10) On 3 June 2020 the Commission informed the Notifying Parties of the serious doubts arising from the preliminary assessment of the Proposed Transaction during a ‘State of Play’ meeting.

(11) On 17 June 2020 the Commission found that the Proposed Transaction raised serious doubts as to its compatibility with the internal market and the EEA agreement and adopted a decision to initiate proceedings pursuant to Article 6(1)(c) of the Merger Regulation.

(12) On 18 June 2020, the Commission provided a number of key documents to the Notifying Parties. The Notifying Parties submitted their written comments to the Article 6(1)(c) decision on 30 June 2020.

(13) On 1 July 2020, at a State of Play meeting, the Commission provided the Notifying Parties with the opportunity to discuss the main issues raised in their Response to the Article 6(1)(c) decision, and indicated the matters on which it planned to focus its further investigative efforts during the Phase II investigation.

(14) On 3 July 2020 the merger review period was extended by 15 working days following the Parties’ request pursuant to Article 20(3) of the Merger Regulation.

(15) During the Phase II investigation, the Commission sent several requests for information to the Notifying Parties.

(16) On 20 July 2020, the Commission adopted a decision pursuant to Article 11(3) of the Merger Regulation requiring the Parties to supply the complete information that had been required by the Commission in two requests for information, one to FCA and one to PSA, sent to the Parties on 26 June 2020.7 The initial time limit to supply the information in both requests for information was 10 July 2020, which the Commission subsequently extended until 17 July 2020.

(17) This decision suspended the time limit referred to in Article 10(3) of the Merger Regulation pursuant to Article 9(1) of Commission Regulation No. 802/2004 from 20 July 2020. By email of 30 September 2020, the Commission informed the Notifying Parties that the suspension of the time limit had expired on 28 September 2020, following the Parties' submission of the required information on that date.

(18) On 28 September 2020, the Commission launched a market test on the commitments submitted on 25 September. On 27 October 2020, the Notifying Parties formally submitted the final version of the commitments.

(19) The meeting with the Advisory Committee was held on 7 December 2020.

5. THE PARTIES’ ACTIVITIES

(20) The Parties’ activities mainly overlap in two areas: (i) Manufacture and sale of PCs; and (ii) manufacture and sale of LCVs. Both Parties also manufacture and sell various automotive spare parts, 8 components and solutions but for the large part, these activities are complementary.9 This activity is, however, vertically related to the manufacture of PCs and LVCs. Finally, both Parties also provide automotive financing and related services.10 The impact of the Proposed Transaction in the LCV and PC markets will be addressed in Sections 6 and 7 of this Decision, whereas the impact on the latter group of activities will be analysed in Sections 9 and 10.

(21) Motor vehicles are manufactured at assembly plants which are usually scaled according to planned production volumes and are layout optimised.11 The assembly process consists of the following steps: (i) Body Shop - contiguous stamping, welding and sealing; (ii) Paint Shop – exterior painting and sealing and (iii) Assembly Shop - both the interior trim of the vehicle and the build-up of the undercarriage / engine dress of the vehicle.

(22) Automotive vehicles are built on ‘platforms’. This term refers to the basic architecture of a vehicle based on a specific set of dimensions. The vehicle platform usually comprises the underbody (chassis, the floor pan and frame), suspension and the axles (front/rear axles and wheel base). 12 A common-platform is a base used in several vehicles. Vehicles based on the same platform share the same sub-frame, front and rear suspension, and a number of other parts except style and personality/decorative features. 13 OEMs tend to concentrate the production of several models on the same platform as a means to achieve economies of scale.14 For this reason, it can be technically easier to manufacture on the same production line vehicles built on the same platform.15 The production activities of the Parties are assessed in Sections 6.2.2.1 and 7.2.1.1.

(23) In order to increase the production capacity of a plant, it is possible to add new production lines for the vehicles already manufactured or for different vehicles. However, the location of a plant might limit the possibility to add buildings with new production lines in order to add production lines and capacity. A capacity increase of an existing plant by [...] could take around [...] and cost between EUR [...].16

(24) As regards the commercial policy, the Parties currently [...].17 Each brand has a CEO (PSA) or Head of Brand (FCA) in charge of products, pricing, sales objectives and communication for the brand and its own sales target and pricing targets.

(25) The Parties distribute their vehicles at wholesale level via a local subsidiary or an independent importer.18 As customary in the sector, retail distribution takes place via independent dealerships. Only exceptionally, FCA and PSA have owned dealers.19 In addition to sales through dealerships, both PSA and FCA also sell part of their vehicles directly, without any intermediary, to customers such as public administrations and corporate fleets.20

(26) The Parties are active worldwide, but their geographic areas of activities are relatively complementary: FCA has a strong presence in the United States, which is one of FCA’s home markets, where PSA no sales, and a significant presence in Latin America, where PSA has limited sales. Both are active in the EEA, but PSA has a slightly stronger presence there.21

6. LCVS

(27) LCVs are commercial vehicles with a gross weight rating of up to 6 tonnes.

(28) The Parties manufacture and sell LCVs in the EEA. PSA manufactures and sells LCVs in the EEA with the brands Peugeot, Citroën and Opel.22 PSA commercialises the Opel models in the United Kingdom under the Vauxhall brand. This Decision will refer to these models as ‘Opel’, regardless of the brand effectively used.

(29) FCA is present in the EEA with the brands Fiat and Fiat Professional. FCA uses Fiat Professional to commercialise its LCV models in Italy and some other countries. This Decision will refer to these models as ‘Fiat’, regardless of the brand effectively used.23

6.1. Relevant markets

6.1.1. Product market definition

6.1.1.1. The Commission’s decisional practice

(30) The Commission’s decisional practice has defined separate markets for the manufacture and supply of PCs on the one hand, and of commercial vehicles on the other hand.24 The Notifying Parties agree25 with the distinction between PCs and commercial vehicles.26 Nothing in the market investigation suggests that this distinction would be incorrect and, therefore, it is retained for the purposes of this Decision.

(31) Within commercial vehicles, the Commission has previously distinguished commercial vehicles markets based on their weight and considered that (i) LCVs, (ii) medium-size trucks; and (iii) heavy duty trucks constitute separate product markets. 27 The Parties’ activities in commercial vehicles in the EEA only overlap in relation to LCVs.28

(32) Within LCVs, the Commission has considered but ultimately left open whether (i) LCVs should be further sub-segmented into vehicles with a gross weight rating of (a) up to 3.5 tonnes, and (b) between 3.5 and 6 tonnes;29 and whether pick-up trucks should be excluded from the LCV market(s).30 The Parties’ activities do not overlap in the EEA in the manufacture and sale of pick-ups, since PSA is not active in this segment in the EEA.31

(33) In its Article 6(1)(c) Decision, the Commission left open whether the market for LCVs up to 3.5 tonnes should be further segmented by size, as it has done in respect of PCs, and whether pick-up trucks should be considered a separate market or part of LCVs.32 The Commission preliminarily concluded that LCVs between 3.5 and 6 tonnes are not part of the same market as LCVs up to 3.5 tonnes. 33

(34) Finally, the Commission has not concluded whether low-emission vehicles (‘LEVs’) and internal combustion engine (‘ICE’) vehicles should constitute separate product markets and whether LEVs should be further segmented according to (i) technology, e.g., battery electric (‘BEVs’), hybrid electric (‘HEVs’) or plug-in hybrid electric (‘PHEVs’) vehicles) or (ii) the categories defined for combustion engine vehicles (e.g. A, B, C, LCVs, etc.).34 In any case, for the purposes of this Decision, the Commission did not investigate whether low-emission vehicles are a separate market from internal combustion engine vehicles as this will not have any appreciable impact in the assessment of the effects of the Proposed Transaction on the markets in view of the limited sales of these vehicles in the EEA,35 and the fact that FCA is currently not present in any low emission LCV market/segment.36

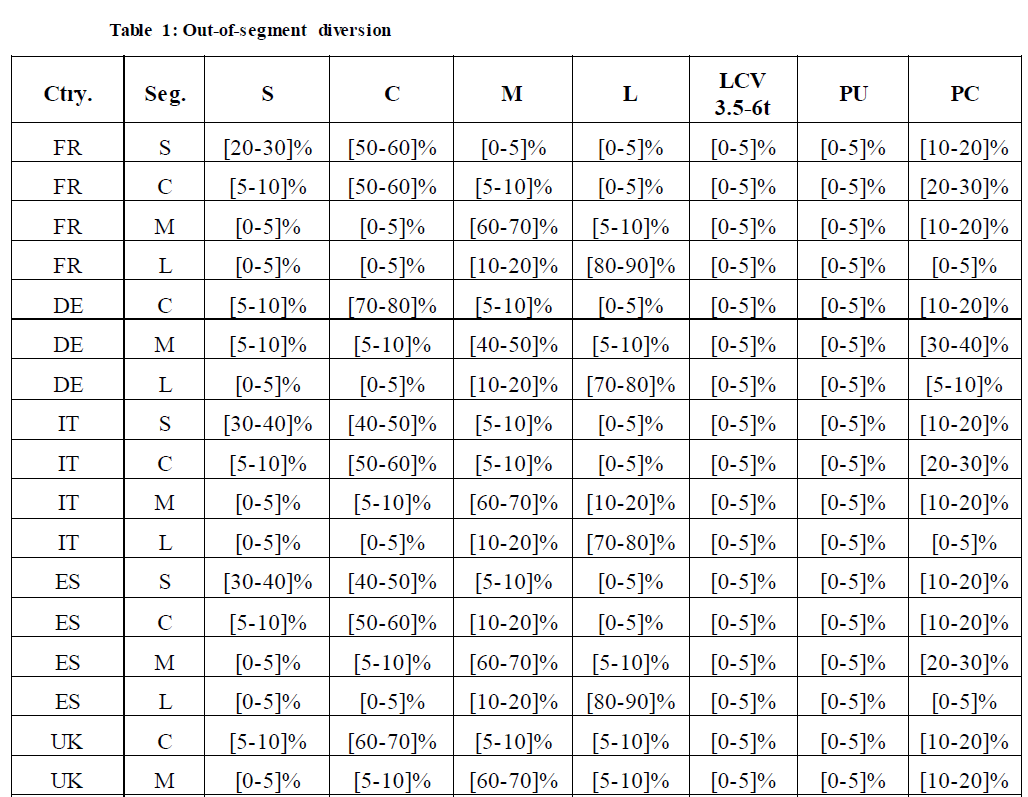

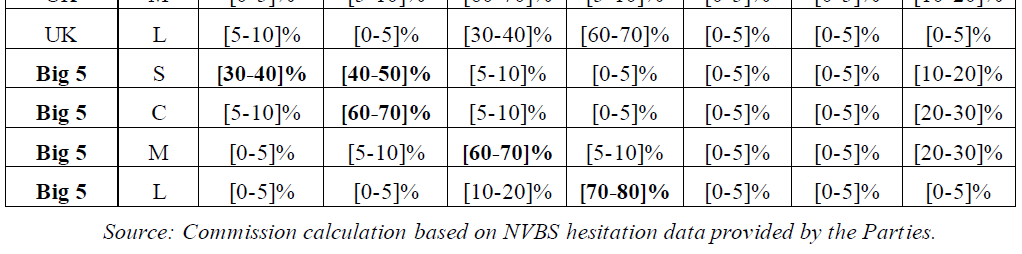

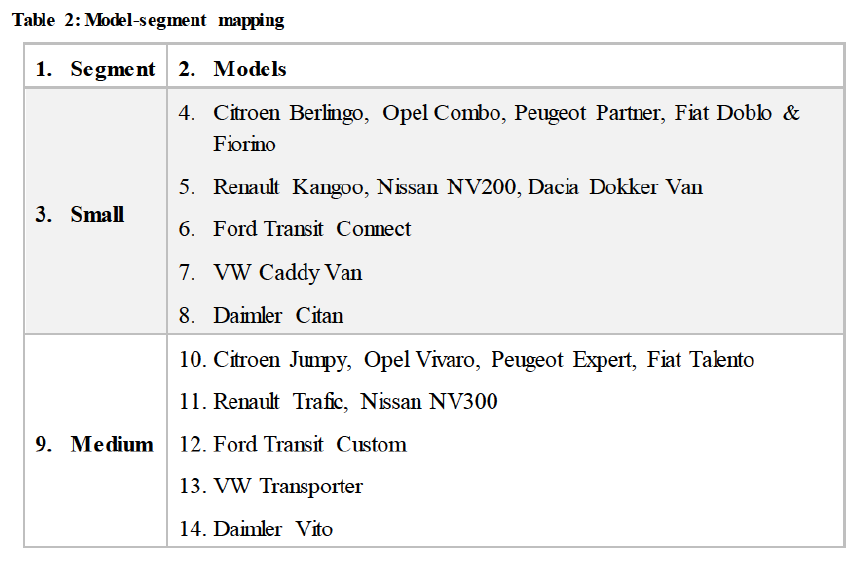

6.1.1.2. Pick-up trucks (‘pick-ups’)

(35) The Notifying Parties consider that the market for LCVs of up to 3.5 tonnes includes pick-ups.37 They note that a large number of respondents in the market investigation of Case COMP/M.8449 – Peugeot/Opel found that pick-ups are mostly considered as commercial vehicles.38

(36) Based on its in-depth investigation, the Commission considers that the market for LCVs up to 3.5 tonnes does not include pick-ups. This exclusion is based both on demand- and supply-side considerations.

(37) The in-depth investigation has shown that there is limited demand-side substitution.

(38) First, LCVs and pick-ups tend to cater for different customer needs. The majority of customers and competitors responding to the market investigation considered that pick-ups should be seen as a separate category from LCVs,39 even if pick-ups can and are used for both commercial and passenger needs.40 A number of respondents specified that pick-ups, when used as commercial vehicles, are employed for different purposes (construction, farming) and in different environments (remote, rural or mountainous areas) than LCVs.41 This also supports the notion that pick-ups cannot be clearly categorised as a passenger or commercial vehicle but should be considered a category on their own.

(39) Second, switching between LCVs and pick-ups appears to be limited. In the in-depth market investigation, a majority of dealers, leasing/rental companies and corporate customers responded that customers do not see pick-ups as an alternative to LCVs. 42 Comments made by respondents suggested that most pick-up customers have considered other pick-up models as the main alternative to their eventual choice.43 This is in line with the results of the New Van Buyer Survey (‘NVBS’), a study that asks purchasers of new vehicles which vehicles they considered as the main alternative to the vehicle actually purchased, i.e. between which models they hesitated. According to this survey, less than 1% of customers of LCVs up to 3.5 tonnes (excluding pick-ups) would divert to a pick-up.44 Similarly, a hesitation study submitted by a market participant for customers in France, Germany, Italy, Spain and United Kingdom shows that most pick-up buyers consider other pick-ups as the main alternative to their ultimate choice and that the marginal amount of customers that did not consider pick-ups as their main alternative hesitated between either LCVs or PCs, confirming pick-ups’ unique positioning between these two segments.45

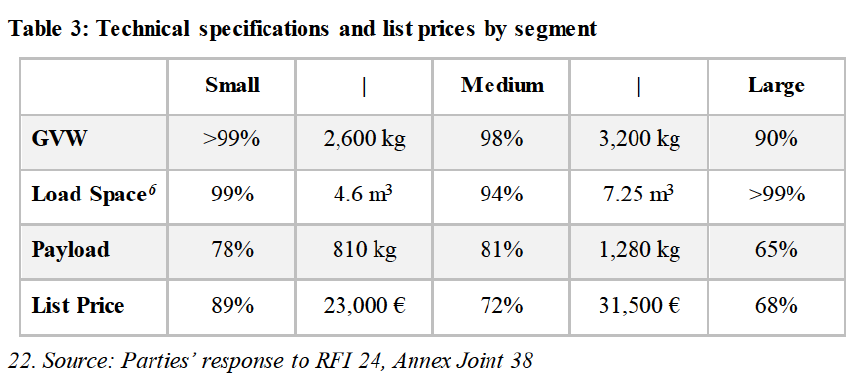

(40) This is further supported by the Parties’ internal documents which show that customers generally do not switch from LCVs to pick-ups and vice versa. Pick-ups compete only with other pick-up models, or to some extent also with SUVs, but not with LCVs.46

(41) Third, pick-ups and LCVs have different technical characteristics. As explained by some competitors during the market investigation, pick-ups are different from LCVs in that they have different dimensions, and do not allow for conversion.47 More generally, they do not protect their load from rain or theft.

(42) Fourth, pick-ups are more expensive, also because they are usually subject to higher taxes than LCVs.48

(43) Fifth, in the Phase I market investigation, a competitor also added that “it is particularly difficult to leverage a brand image acquired in LCV or PC into the Pick-Up truck space”. According to this competitor, OEMs which are strong in pick-ups are often weak in LCVs and vice versa.49 This is supported by the fact that PSA is not present and FCA is not strong in the manufacture and supply of pick-ups in the EEA.

(44) The in-depth investigation has also shown that there is no (or very limited) supply-side substitutability between pick-ups and LCVs. First, pick-ups and LCVs are produced on different production lines and switching production would be difficult, since the chassis is not the same.50 Second, the Parties’ internal documents show the business practice of reporting pick-up sales separately, as a separate category from Small, Medium and Large LCVs.51

(45) In view of the above, the Commission considers that pick-ups are not part of the same product market as LCVs but form a separate distinct product market of their own.

6.1.1.3. LCVs of up to 3.5 tonnes: Distinction between LCVs of different sizes

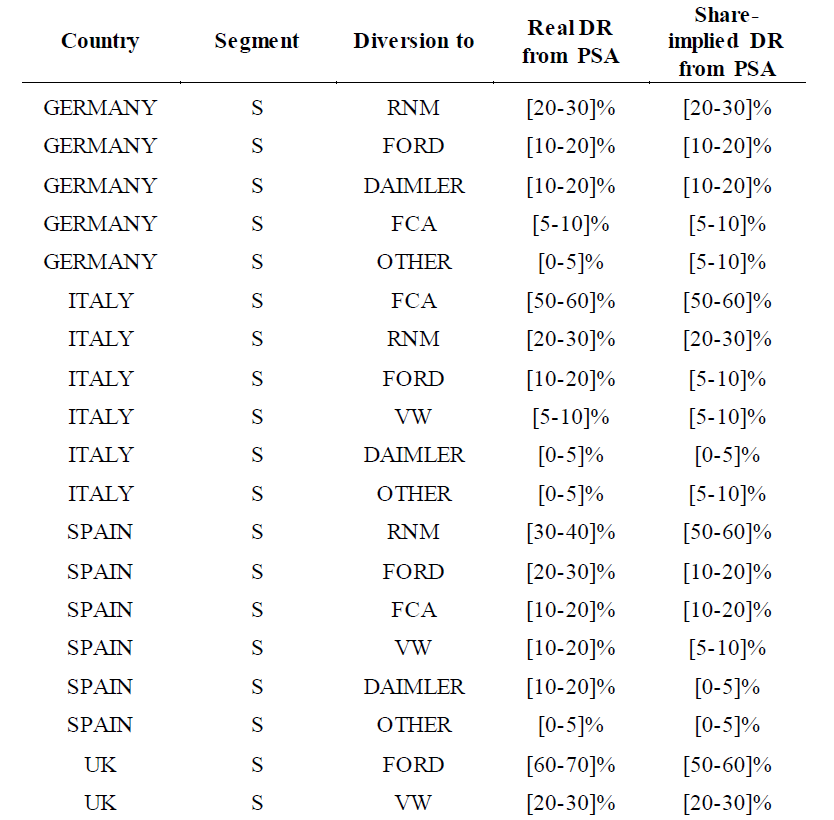

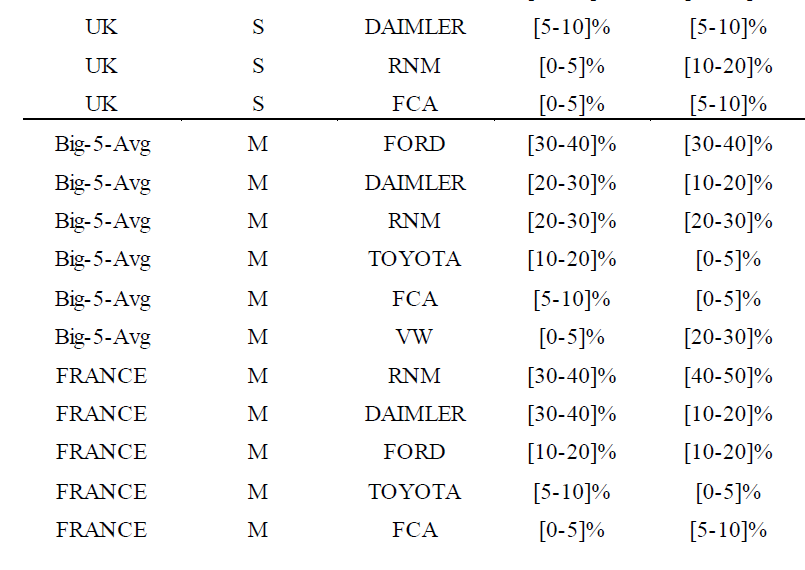

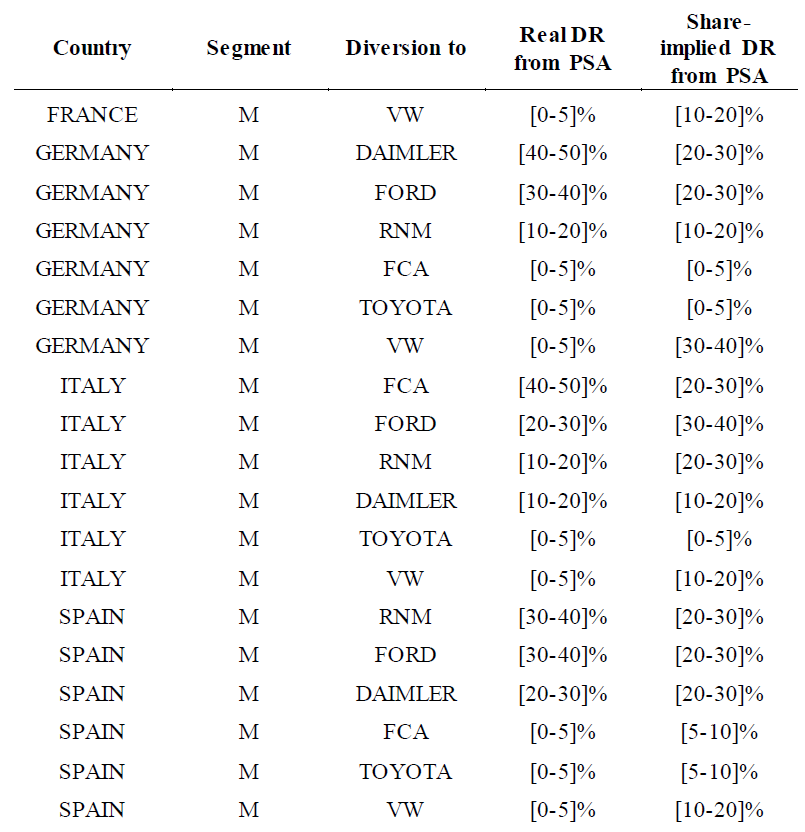

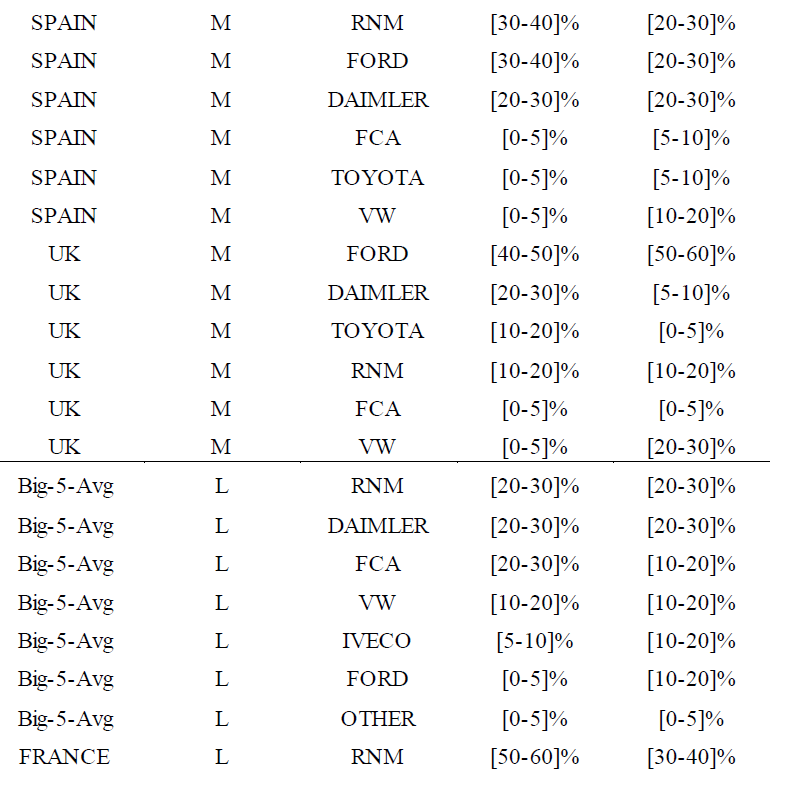

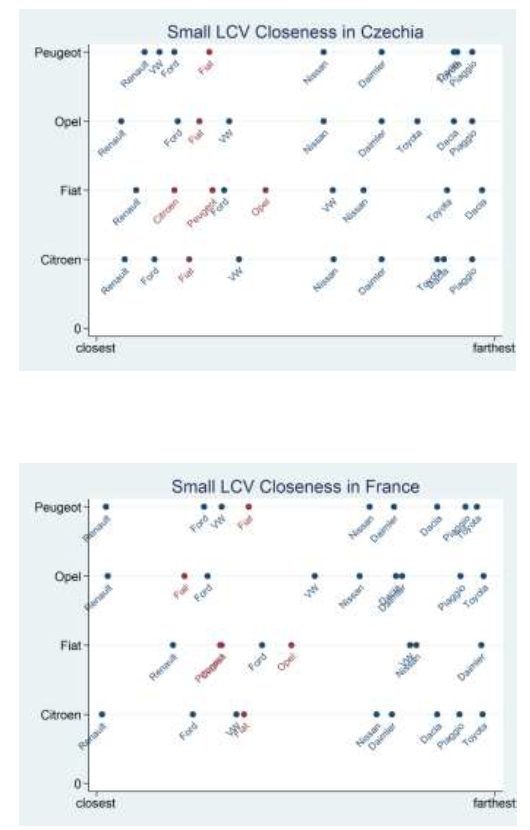

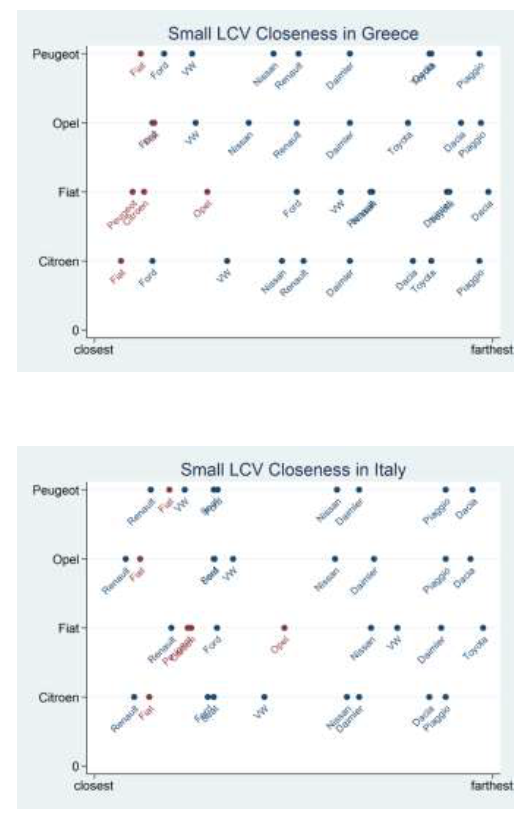

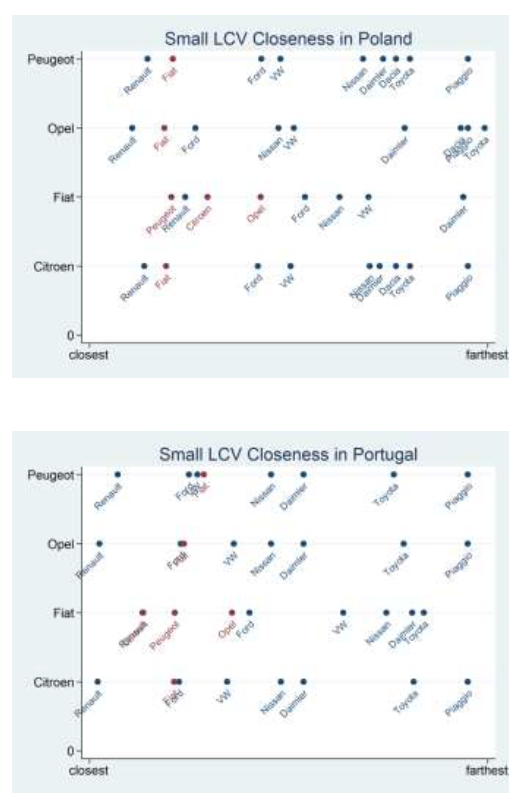

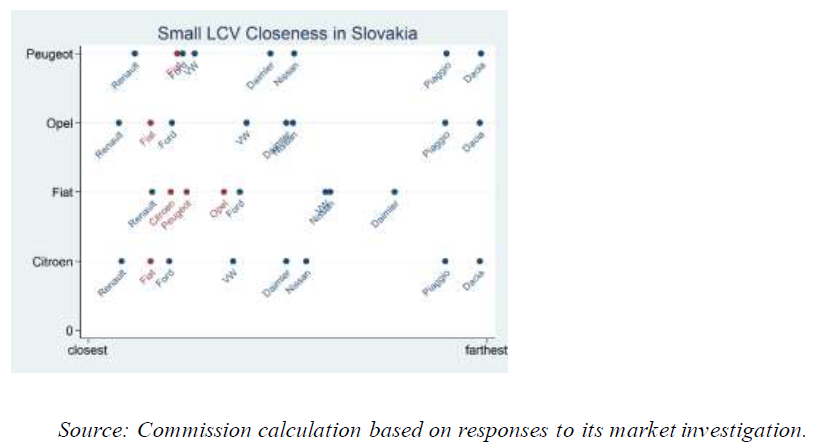

(46) In the Article 6(1)(c) decision, the Commission left open whether LCVs up to 3.5 tonnes should be further segmented by size, as it has done in respect of PCs.52

6.1.1.3.1. The Notifying Parties’ views

(47) The Notifying Parties consider that the market for LCVs of up to 3.5 tonnes should not be further sub-segmented into separate product markets by size of LCV.

(48) From the supply-side perspective, the Notifying Parties consider that there is substitutability between LCVs of different sizes since (i) the main OEMs offer the full range of LCVs; (ii) the technical characteristics (number of seats, load space, payload capacity, towing capacity, etc.) of the different sizes of vehicles overlap; (iii) the price ranges that OEMs set for their offerings do not correspond to different sizes of LCVs; and (iv) vehicles of different sizes are often manufactured on the same platforms in the same plants.53

(49) From the demand-side perspective, the Notifying Parties submit that LCVs of different sizes compete with each other as consumers’ purchasing decisions are based on criteria other than the size of vehicle. Citing results of the NVBS, the Notifying Parties note that size is mentioned by consumers as one of the main criteria for their purchasing decisions only after others like the personal experience with previous models bought or the purchase price.54

6.1.1.3.2. The Commission’s assessment

(50) The Commission considers that LCVs up to 3.5 tonnes can be sub-segmented into three categories (‘small’, ‘medium’ and ‘large’), and that each of those three categories constitutes a separate product market.

(51) This is based both on demand- and supply-side considerations, taking into account the following factors: First, internal documents submitted by the Parties show that this segmentation is used by FCA and PSA in the regular course of their business. Second, there are clear dividing lines between the technical characteristics and prices of the different LCV sizes. Third, there is a wide consensus in the industry on the use of this segmentation, and such a distinction by size is also in line with the Commission’s practice in PCs. Fourth, based on hesitation data and the replies of market participants to the market investigation, there is limited demand-side substitutability. Finally, there is limited or no supply-side substitutability between different LCV sizes. The following sections of this Decision will explain these factors in detail.

A The Parties’ internal segmentation

(52) The internal documents provided by the Parties illustrate that both FCA and PSA regularly distinguish in the course of their business different types of LCVs of up to 3.5 tonnes depending on their size.

(53) PSA distinguishes internally three segments of LCVs of up to 3.5 tonnes: ‘small’, ‘medium’ and ‘large’.55 Each of PSA’s brands has one LCV model in each of the three categories (Citroën Berlingo, Peugeot Partner and Opel Combo are small LCVs; Citroën Jumpy, Peugeot Expert and Opel Vivaro are medium LCVs; and Citroën Jumper, Peugeot Boxer and Opel Movano are large LCVs). [...]. However, for the reasons explained in Section 6.1.1.7, car-derived vans do not belong to the same product markets as LCVs.

(54) FCA also distinguishes segments by size but identifies four categories: ‘small’, ‘compact’, ‘midsize’ and ‘large’.56 FCA’s midsize and large categories correspond to PSA’s medium and large segments. FCA divides the smaller LCV category into two separate segments (small and compact) due to the fact that it manufactures two vans of smaller dimensions: One is the Fiat Doblò, which FCA includes in the compact category together with most small LCVs produced by other OEMs (i.e. with Citroën Berlingo, Peugeot Partner and Opel Combo); the other is the Fiat Fiorino, which is smaller than the Fiat Doblò. However, according to FCA’s internal segmentation, there appears to be only one major brand besides Fiat (Ford, with its Ford Transit Courier)57 that includes in its product offer a van that can be included in this smaller category.58 Moreover, [...].59 As explained in detail in this Section, the Commission considers that vehicles in FCA’s small and compact categories should be considered part of the same Small LCV product market.

(55) The internal documents of the Parties show that PSA and FCA use this segmentation consistently in their regular course of business. An example is the graph below, which shows an illustration of how FCA shows in its internal presentations the competitiveness of its LCV fleet in Europe.60

Figure 1: competitiveness FCA LCV models

[...]

Source: Form CO, Annex FCA 35

(56) [...].61

(57) PSA’s internal documents show [...].62 Particularly illustrative are PSA’s internal documents in which LCV partnerships with other OEMs are discussed. [...].63

(58) Finally, PSA and FCA map their competitors’ models in an identical way, allocating each LCV model to the same segment.64

B Different technical characteristics

(59) The Parties’ and their competitors’ models, segmented by size following the segmentation used by PSA (small, medium and large LCVs) is set out in Table 1.

TABLE1

(60) And Table 2 presents the ranges of the main technical parameters of LCVs for each

of these segments (small, medium and large), to the extent they are reported in the IHS data.

TABLE2

(61) As reflected in Table 1, most OEMs manufacture three sizes of LCVs per brand,

essentially one per category. Within each size, OEMs offer different versions/adaptations and options/upgrades and, for this reason, the technical characteristic of each product are defined in ranges rather than in precise parameters, although there is a correlation between size of the model and the rest of technical parameters (the size of the model has a reflection in the maximum number of seats, load space, payload capacity).

(62) The Notifying Parties presented evidence that there is significant overlap as regards load space and payload between the different LCV segments. However, this analysis suffers from at least two flaws: First, it considers LCVs with any number of seats. It is therefore not surprising that it finds that a Small LCV (with 2 seats) can have more load space than the people-carrier version of a Large LCV with 17 seats, but this does not make the 17-seater a good substitute for a Small 2-seater LCV. Second, it covers the fiill range of models, rather than focusing on more common models or analysing the percentage of models that falls within a certain range. If this is done (as the Commission has undertaken in Section 2 of Annex 1 to this Decision (the `LCV Economic Annex')), it becomes obvious that the different types of LCVs fall into essentially non-overlapping ranges for the different technical specifications.

(63) In fact, the Commission does not contest the fact (as submitted by the Notifying Parties) that there may be some limited overlap at the extremes of the ranges of the different categories, e.g. load space or price. This limited overlap is, however, only the consequence of LCVs being differentiated products by nature, meaning that players active in the LCV markets need to adapt and diversify their product offering to cater for the specific needs of different types of customers. This does not mean that there are no clear dividing lines between the various segments and is not incompatible with the definition of separate product markets, as demonstrated by the Commission's decisional practice for PCs, which the Parties do not contest, where the existence of a limited overlap between different segments has not prevented the Commission from regularly and consistently defining separate product markets for each category of vehicles according to a segmentation which is broadly accepted at in dust y-leve1.65 As explained further below in this Section, the same consensus exists in the industry for distinguishing three separate LCV markets by size of the vehicle.

(64) In any case, the Commission considers that although there is a limited overlap between the different segments, in order to determine if there are dividing lines between categories, it is appropriate to observe the entire value range of each technical parameter and to determine where most of the vehicles lie within that range. When doing so, it is clear that each LCV type (Small, Medium, Large) constitutes a well-defined and distinct category in terms of technical specifications.

(65) An indication of this is provided by the 10th, 50th (median) and 90th percentile of total load space within each LCV type, as shown in Table 3.

TABLE3

(66) This table shows that the segments are clearly distinct in termes of load space. For

example, the `typical' vehicle of one segment has almost twice the load space of the ‘typical’ vehicle of the next smaller segment.66 Moreover, when considering 80% of the vehicles within each segment, it is clear that the overlap between the different categories is limited: 80% of Small LCVs have a load space of 2.9 to 4.2 m3, while 80% of Medium LCVs have a load space of 5.2 to 6.8 m3 and 80% of Large LCVs have a load space between 8.6 and 15.1 m3.

(67) Furthermore, as illustrated in detail in the LCV Economic Annex, which constitutes an integral part thereof, there are clear dividing lines between Small and Medium LCVs that can be drawn at a gross vehicle weight (‘GVW’) of 2 600kg (more than 99% of small LCVs have a GVW below 2 600kg, whereas 98% of Medium LCVs have a GVW between 2 600 and 3 200kg and 90% of Large LCVs have a GVW above 3 200. Similar dividing lines can be drawn in terms of load space, payload and prices.

(68) Finally, as regards Notifying Parties’ argument that load space is not mentioned by customers as one of the main reasons for choosing a particular model of new LCV, the Notifying Parties fail to explain how this can constitute evidence for demand-side substitutability across segments when the hesitation data show that the main alternative considered is usually an LCV of the same segment.

C Consensus in the industry

(69) Replies from market participants to the Commission’s market investigation demonstrate that there is a wide consensus across the industry that LCVs up to 3.5 tonnes should be segmented according to size. A majority of the OEMs responding to the market investigation answered that they consider appropriate to distinguish the different types of LCVs of up to 3.5 tonnes based on the space/volume or payload of vehicles, and in particular endorsed a distinction between Small, Medium and Large LCVs, including in each category essentially the same vehicles that the Parties do in their internal segmentation.67 Similarly, a vast majority of importers,68 dealers,69 leasing and rental companies70 and corporate customers71 responding to the market investigation were of the view that sub-segmenting the different types of LCVs of up to 3.5 tonnes based on the space/volume or payload of vehicles along the these lines was appropriate. Many of the respondents highlighted that this segmentation is the usual one in the market.72

(70) In fact, as Table 1 above illustrates, most brands are present in the EEA markets with exactly one LCV in each of the three product categories.73 Market players therefore perceive that providing a diversified product portfolio with one vehicle in each segment meets end-customers’ demands more efficiently than, for instance, offering just one single vehicle across sizes. In the Commission’s view, this consistent industry-wide segmentation is already a strong indication of limited demand-side substitutability between the different segments.74

D Limited demand-side substitutability

(71) The existence of limited demand-side substitutability between these three segments (Small, Medium and Large LCVs) is, in addition to the internal documents where the Parties analyse competitive pressure mainly between vehicles belonging to the same segment, supported by the hesitation data provided by the Parties and the replies by market participants to the Commission’s market investigation.

(72) The Parties have provided hesitation data collected by NVBS. Hesitation data was available for the years [...] for [five Member States]. This data provides useful information in terms of demand-side substitutability as it indicates, for each LCV model purchased by customers, which model was considered as the main alternative. As explained in detail in the LCV Economic Annex, the Commission has calculated diversion ratios by segment on the basis of these data distinguishing between small, compact, medium and large (i.e. in line with FCA’s internal segmentation).75 The result is as follows:

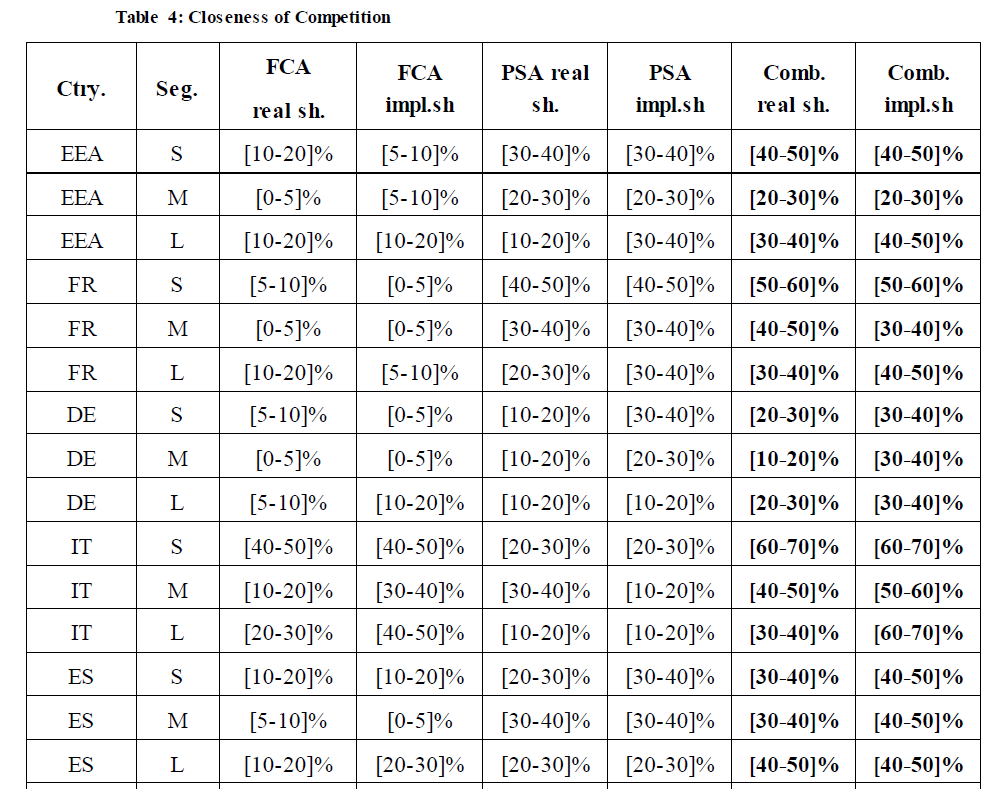

– In the five countries for which NVBS data was available, the vast majority of customers considered another LCV of the same segment as the main alternative: Overall, [70-80]% for Large LCVs, [60-70]% for Medium LCVs, and overall more than [70-80]% for small and compact LCVs together.

– The different LCV segments impose very limited constraints on each other,

with out-of-segment diversion rates below [20-30]% in all cases.

– The only exception to the above is customers of Small LCVs, which considered compact LCVs as their main alternative in a percentage ([40-50]%) significantly higher than the percentage in which customers considered other small LCVs as their main alternative ([30-40]%).

(73) In other words, except between FCA’s small and compact categories, demand-side substitutability between segments appears to be very limited.76 This therefore supports the notion that the product market should be divided into three separate product markets, Small (comprising both small and compact), Medium and Large.

(74) This also demonstrates the irrelevance of the Notifying Parties’ observation that in the NBVS study size is only mentioned by consumers as one of the main criteria for their purchasing decisions only after personal experience with previous models bought or the purchase price. Since LCV customers mainly hesitate between models of the same segment and therefore of similar sizes, it is clear that within each segment the ultimate decision will necessary be based on other criteria as there is not a significant variation in terms of size within a given segment (see Table 3). Conversely, since customers do hesitate mainly between models of the same segment, the information that they do not mainly choose between the different models of the same segment based on size cannot be considered evidence for substitutability across segments.

(75) The responses to market investigation are consistent with this conclusion.

(76) A vast majority of importers77 and a majority of dealers,78 rental and leasing companies79 and corporate customers80 considered that LCVs belonging to different segments are not substitutable from the customer perspective.

(77) Numerous customers highlighted that the size and capacity of the vehicles appear to be the main selection criteria for LCVs and that customers would only consider as alternative other models that match its size/capacity needs. A representative answer was provided by one importer: “LCV decision of purchase is mainly driven by concrete customer needs in terms of cargo volume, payload, engine power etc. Smaller LCV category cannot substitute bigger LCV in the case it doesn't (sic) fit concrete business needs”.81 This representative quote supports the distinction between various categories of LCVs based on their size and capacity.

(78) At the same time, in relation to the substitutability between small and compact, the market investigation broadly confirmed the conclusions of the analysis of the hesitation data: a majority of OEMs,82 importers,83 dealers84 and leasing and rental companies85 indicated they do not see appropriate a further sub-distinction within the smaller LCV category and indicated that small and compact LCVs are substitutable from the end-customer perspective.86

(79) In conclusion, from a demand-side perspective (i) small and compact LCVs should be considered part of the same product market (‘Small LCVs’) and (ii) Small LCVs (including small and compact), Medium and Large LCVs should be considered as distinct and separate product markets.

E Limited supply-side substitutability

(80) There is also limited (if any) supply-side substitutability between Small, Medium and Large LCVs.

(81) According to the Commission Notice on the definition of relevant market for the purposes of Community competition law87 (‘Commission Notice on Market Definition’), supply side substitution is taken into account for the purposes of product market definition when its effects are equivalent to those of demand-side substitution in terms of effectiveness and immediacy which means “that suppliers are able to switch production to the relevant products and market them in the short term without incurring significant additional costs or risks in response to small and permanent changes in relative price”.88

(82) The Notifying Parties consider that models of different segments are often produced in the same plants. However, production in the same plant is not the relevant criterion to assess supply-side substitutability, as the ease and cost of switching instead depends on the parts and machinery used, i.e. on the platform and production line.

(83) The Commission notes that FCA’s and PSA’s models belonging to the same segment [...]. PSA’s Medium LCVs (Citroën Jumpy, Peugeot Expert and Opel Vivaro) are manufactured on the [...] platform. PSA’s Small LCVs (Citroën Berlingo, Peugeot Partner and Opel Combo) are manufactured on the [...] (also referred as “[...]”) platform. FCA’s Small LCVs (Fiat Fiorino and Fiat Doblò) are manufactured on the “[...]” platform. And FCA’s, Citroën’s and Peugeot’s Large LCVs (Fiat Ducato, Citroën Jumper and Peugeot Boxer) are [...] manufactured on the [...] platform.89 Models manufactured by the Parties and belonging to different segments are therefore manufactured on different platforms. They are also produced at different production sites and (consequently) on different production lines.90 The Commission’s in-depth investigation has indeed shown that this is rare for LCVs of different sizes to be built on the same platform.91

(84) The consequence of having different models built on the same platform is that it is relatively easier for OEMs to switch production between them, since they share many of the essential component parts and, very frequently, they are built on the same production line. On the contrary, switching between vehicles built on different platforms is necessarily more complex, and therefore more costly, as their main components and production processes will typically differ.

(85) Consequently, as models of different segments are built on different platforms and different production lines, the Parties’ argument that the main OEMs offer the full range of LCVs is irrelevant, 92 as that fact does not demonstrate in itself any supply-side substitution.93 For that to be the case, it would be necessary that, in case of a small permanent increase in the relative prices of, for instance, Large LCVs, other OEMs could react in the short term without incurring significant additional costs by increasing their production of Large LCVs in the production lines/platforms they use to produce Small or Medium LCVs, an argument that the Notifying Parties have not made.94 Rather, the Notifying Parties have confirmed the exact opposite:

“[I]n order to allow a production line to manufacture a new vehicle, the OEM needs to implement some adaptations of each one of these main stages of the manufacturing process: [ ...] In the body shop: new stamping tools, modification of the common areas and new fitting for the specific parts of the new vehicle; [ ...] In the paint shop: new programs for the painting robots and modification of the assembly stations for the specifics of the paintwork; [ ...] In the assembly shop: configuration of the information systems and modification of the programmes of the assembly stations and the test facilities. [ ...] While the timing and associated cost for the new production to be operational depends on many factors, timing could be approximately [...] and the associated cost could be around EUR [...]”.95

(86) In this sense, it is worth noting that according to the Commission Notice on Market Definition, “[w]hen supply-side substitutability would entail the need to adjust significantly existing tangible and intangible assets, additional investments, strategic decisions or time delays, it will not be considered at the stage of market definition”.

(87) In fact, many OEMs have indicated in the market investigation that switching production from a given model to a model in a different LCV segment could not be done in short timeframe or without costs.96 For instance, RNM explained that “[t]he manufacturing and distribution of LCVs cannot be switched quickly and cost-effectively from one segment to other segments”.97 Similarly, Iveco indicated as follows: “such a change [from a model in a given segment of LCVs to a model in a different segment of LCVs] will involve a change of platform, which has consequences from a production perspective”.98

(88) Therefore, since switching production from a vehicle in one LCV segment to a vehicle in another LCV segment cannot be done without adapting production lines for producing a different platform, which means significant adjustments which require investments and lead times, the Commission cannot conclude that there is supply-side substitution between small, medium and large LCVs.99

(89) On the contrary, within Small LCVs, FCA has confirmed that [...], which would allegedly make it easier to switch production between those models. In this regard, the Commission considers particularly illustrative the response given by RNM as to the question of whether it would be appropriate to subdivide the Small segments and distinguish these two categories: “Technically, mini-vans and compact vans generally refer to the same type of vehicles, having regards to their platforms and powertrain which are generally identical from one subcategory to another. Although the cabins may differ between the mini vans and compact vans categories for the Fiat (Fiorino vs. Doblo) and Ford models (Transit Courier vs. Transit Connect), respectively, such differentiation does not entail significant switching costs. Lastly, RNM like other OEM used to offer small vans likely to fall into the two categories above, under the same model: e.g. Kangoo L0 and L1-L2”.100

F Conclusion on LCVs up to 3.5 tonnes

(90) In view of all of the above, the Commission concludes that (i) small and compact LCVs should be considered part of the same product market, and (ü) Small LCVs (including small and compact), Medium and Large LCVs should be considered as separate product markets.

6.1.1.4. LCVs between 3.5 and 6 tonnes

(91) The Notifying Parties agree with the distinction between LCVs, medium-size trucks and heavy duty trucks.101 However, they submit that the LCV market includes all LCVs with a gross weight rating of less than 6 tonnes.102

(92) The Notifying Parties base their view on supply-side substitutability. They argue that there is no reason to distinguish between large LCVs with a gross weight rating of less than 3.5 tonnes and the same LCV models with a gross weight rating of more than 3.5 tonnes. [...].103 Similarly, PSA’s Large LCVs (Peugeot Boxer, Citroën Jumper and Opel Movano) can also have a gross weight rating of more than 3.5 tonnes [...].104 According to the Parties, whilst the versions of more than 3.5 tonnes require specific adaptations (special brakes, suspensions and other mechanical parts, a speed limitation device and a tachograph) and a different homologation, these differences can be addressed easily in the production process.

(93) The Parties equally claim that the Large LCV models of the main competitors (Daimler’s Sprinter, RNM’s Master and NV400, Ford’s Transit and VW’s Crafter) have versions with a gross weight rating of more than 3.5 tonnes which are manufactured on the same platform as the versions of up to 3.5 tonnes. 105

(94) The Commission considers that there is limited or no demand-side substitutability between LCVs up to 3.5 tonnes and LCVs between 3.5 and 6 tonnes.

(95) First, in the Phase I market investigation, a vast majority106 of each customer respondent group considered that customers planning to purchase, lease or rent LCVs belonging to one segment (up to 3.5 tonnes or between 3.5 and 6 tonnes) would not consider vehicles in the other segment as an alternative. 107 The reason most often mentioned for this lack of substitutability on the demand-side is the difference in driving licences required for each sub-segment and the differences in size and capacity.108

(96) In fact, according to Directive 2006/126/EC,109 drivers carrying a category B driving licence are authorised to drive “motor vehicles with a maximum authorised mass not exceeding 3 500 kg and designed and constructed for the carriage of no more than eight passengers in addition to the driver”110. The minimum age for category B driving licences is fixed at 18 years. By contrast, the driving of vehicles exceeding a maximum authorised mass of 3 500 kg require other types of licences (category C1, D1, D1E), which require a minimum age of 21 years.1 11

(97) Another reason mentioned by many respondents to the Phase I market investigation was the existence of significant differences in loading capacity for which demand is inelastic.112 In other words, “[a] potential customer will purchase/lease/rent an LCV in order to meet his daily needs. That means, the one who will purchase/lease/rent an LCV with a gross weight rating between 3.5 and 6 tonnes will not consider buying an LCV of up to 3.5 tonnes and vice versa, since capacity is usually one of the primary selection criteria”.1 13

(98) Second, the lack of demand-side substitution between both types of LCVs is supported by the NVBS hesitation data submitted by the Parties,114 according to which less than [...] of customers of LCVs of less than 3.5 tonnes (excluding pickups) would divert to a larger LCV with a gross weight of 3.5 to 6 tonnes.

(99) Third, as explained in Section 6.1.1.3 above, since the Commission considers that Small, Medium and Large LCVs below 3.5 tonnes belong to separate product markets, based on both demand- and supply-side substitutability, it would be counterintuitive that all LCVs below 3.5 tonnes and LCVs between 3.5 tonnes and 6 tonnes would belong to the same product market.

(100) However, when considering supply-side substitutability, some elements provided by the Parties do point towards a certain supply-side substitutability between Large LCVs and LCVs between 3.5 and 6 tonnes. In particular, models commercialised by the major OEMs in the category of Large LCVs up to 3.5 tonnes also have a larger version in the LCV above 3.5 tonnes category, and both versions are manufactured on the same platform. However, the Commission does not have enough information to conclude whether the effects of that substitutability are equivalent to those of demand substitution in terms of effectiveness and immediacy, as the Commission Notice on Market Definition requires.115 In particular, the Parties have not provided specific information on what would be the costs and lead times involved if the mix of production between models below and above 3.5 tonnes was to be adjusted significantly.

(101) In any case, for the purposes of this Decision the Commission does not need to take a position on whether LCVs of gross weight rating between 3.5 and 6 tonnes must be considered a separate market or belong to the same product market as Large LCVs of up to 3.5 tonnes since, under both market definitions the Proposed Transaction does not lead to a significant impediment to effective competition. For the purposes of this Decision, the Commission will therefore assess the effects of the Proposed Transaction on the markets for Large LCVs, LCVs between 3.5 and 6 tonnes as well as on a market comprising both Large LCVs and LCVs between 3.5 and 6 tonnes.

6.1.1.5. Semi-finished LCV products

(102) All LCVs, both finished LCVs (a van) and semi-finished LCV products, can be converted. FCA estimates that [...] of all LCVs (of any size) are converted in some manner into various types of special purpose vehicles, such as camper vans, motorhomes, ambulances, food trucks, hearses, refrigerated vans, luton box vans, tippers, etc.1 16

(103) In many cases, conversions are modifications of a finished van. That is the case for camper vans, i.e. vans which are adapted and fitted for camping purposes, as well as many other converted vehicles such as ambulances, refrigerated vans, isothermal vans, armoured vehicles, and delivery vans.1 17 Conversions of finished vans are generally carried out by third party converters, but the OEM, converter or dealer can sell the converted LCV product to the end customer.11 8

(104) The Parties [...] (i.e. camper vans or motorhomes). Other OEMs do market camper vans directly.119 This is the case for VW with the VW California and Daimler with the Marco Polo. Most OEMs, including the Parties, do not equip and market camper vans but sell standard LCVs to converters which then equip and market the finished camper vans, or any other converted LCV.120 These LCVs for conversion are similar to standard LCVs and differences are limited. 121

(105) In addition to conversions of the finished LCV (the van), OEMs also sell semifinished LCV products to converters. These converters then convert the semifinished LCV products into motorhomes and other special purpose vehicles.

(106) There are three types of semi-finished LCVs:122

– A ‘chassis cab’ is a chassis and driver’s cabin to which the converter adds a rear unit.

– A ‘chassis cowl’ is a chassis and the interior of the driver’s cabin to which the converter adds a rear unit and exterior.

– A ‘back-to-back’ is either (a) the driver’s cabin, or (b) the interior of the driver’s cabin (i.e., the cowl).

6.1.1.5.1. The Notifying Parties’ views

(107) The Notifying Parties consider that semi-finished LCV products form part of an overall LCV market rather than being a separate product market. They argue that there is almost complete supply-side substitutability for all types of semi-finished LCV products.123

(108) [...]. Therefore, every manufacturer that produces LCVs could decide to supply finished and semi-finished LCVs.124

“[...].”125

(109) Manufacturers may make minor production adjustments for finished and semifinished LCV products that facilitate but are not essential to conversion. These limited modifications include a widened rear track, adjusted suspensions to sustain higher load and certain types of specific parabolic leaf springs. 126 [...]. According to the Parties, any LCV manufacturer could introduce these modifications without incurring significant investments or delays. Alternatively, converters can buy semifinished LCV products without these modifications from manufacturers and afterwards make the adjustments themselves or hire third parties to do it for them. 127

(110) Moreover, the Notifying Parties submit that the market should not be segmented according to the type of converter or end use of the finished/semi-finished LCV product. All OEMs supply the same finished and semi-finished LCV products to motorhome converters, other converters and final customers that purchase finished LCVs.128 They also note that all OEMs that offer LCV products sell them to all types of converters, not only to motorhome manufacturers. 129

6.1.1.5.2. The Commission’s assessment

(111) Based on its in-depth investigation, the Commission considers that semi-finished LCV products and finished LCV products belong to the same product market, due to supply-side substitutability.

(112) First, the Commission’s investigation has shown that manufacturers produce semifinished LCV products on the same production lines as finished LCVs.130

(113) Second, nearly all competitors manufacturing finished LCV products also sell semifinished LCV products. To date, not every OEM produces every type of semifinished LCV product. [...] Daimler produce all three main types.131 All major OEMs (i.e., also including Ford, VW, and RNM) offer the chassis-cab. Another OEM as well as soon VW offer the chassis-cowl. Competitors appear to be technically able to produce different types of semi-finished products, also back-to-back with some additional investment.132

(114) Demand for semi-finished LCV products, in particular for the purpose of motorhomes, has been growing.133 This is evidenced by an OEM recently introducing a new type of semi-finished product it previously did not offer (chassis cowl). VW is also planning to introduce chassis cowls.134 This shows that OEMs will likely introduce new types of semi-finished LCV products where a profitable business case exists.

(115) Third, internal documents of the Parties [...].135

(116) Therefore, in view of the above, there is no separate market for semi-finished LCV products, but these products are part of the Large LCV market.

(117) Based on its in-depth investigation, the Commission also considers that there is no need to sub-segment the sale of semi-finished LCV products by customer type.

(118) The Commission analysed in particular whether [...].136 Motorhome manufacturers are important customers given their large individual orders137 of semi-finished products and because FCA has historically been very strong in the sale of LCV products to motorhome manufacturers (due to FCA having focused on motorhome customers and offered a very good service package). Competitors appear to have started showing interest in motorhome customers later.138

(119) The Commission notes that first, OEMs sell the semi-finished products to both motorhome manufacturers and other converters.139 Semi-finished LCV products supplied to motorhome manufacturers are essentially the same as those supplied to other converters. Some motorhome manufacturers explained that for some motorhome products the chassis has to be specially designed for that purpose, but acknowledged that equally, this also applies for some other end use conversions.140 Ultimately, these are adaptations or variations of the same product.

(120) Second, all OEMs supply different converters; none exclusively supplies motorhome manufacturers.141

(121) Finally, motorhome manufacturers and other converters face the same commercial conditions: [...].142 Whilst the Parties’ internal documents related to marketing analyse sales per customer groups such as motorhome manufacturers and various other specialised converters, 143 the Commission found no evidence that commercial conditions or technical specifications of semi-finished LCV products differ between motorhome manufacturers and other converters.

(122) In view of the above, the Commission considers that semi-finished LCV products are part of the same product market as Large LCVs and that no further sub-segmentation is necessary by customer group.

6.1.1.6. PC versions of LCVs

(123) Some PC models, known as ‘People Movers’, are manufactured on the same platforms as LCVs, although not always on the same production lines.

6.1.1.6.1. The Notifying Parties’ views

(124) The Notifying Parties submit that People Movers and LCVs do not belong to the same relevant market, and that People Movers should be classified as PCs belonging to segment M.

(125) From a demand-side perspective, People Movers and LCVs address different customer groups. People Movers are typically purchased by individual customers, while LCVs generally target B2B clients (professionals). That explains why separate marketing campaigns are organised for People Movers and LCVs. For example, the [...] (the People Mover vehicle [...]) and [...] (the People Mover vehicle [...]) were [...] marketed under the Fiat brand and not under the Fiat Professional brand.144

(126) From a supply-side perspective, the Parties submit that there is limited supply-side substitutability between People Movers and LCVs due to the following reasons:145

– People Movers are produced in significant volumes and require specific R&D, manufacturing and marketing expenses separated from those of LCVs.

– People Movers and LCVs have different structures. For instance, they have different bodies, floors and back ends (People Movers usually have back doors whereas LCVs usually have swing doors).

– People Movers also have different features and equipment. Around [...] of the parts required for the People Movers produced by both Parties are specific, representing a standalone development work stream, separate from that of the corresponding LCVs. In fact the range of People Movers is much more diverse (with more trim versions) than LCVs, and they have a large number of specific parts/features (not generally found in LCVs), such as specific doors, wheels, windows and second and third-row seats.

– People Movers and LCVs are subject to different regulations and safety tests. People Movers are subject to regulations applicable to PCs, which are more demanding and costly than those applicable to LCVs. People Movers also have to comply with stricter emission regulations than LCVs. Complying with those represents additional R&D work, specific parts and investment costs.

(127) As a result of these differences, the manufacturing times for People Movers and LCVs are different (e.g. in [...] the People Mover built on the [...] platform takes [...] times the manufacturing time for the LCV built on the same platform, and the People Mover is partially manufactured on a different assembly line). 146

(128) Switching production and adjusting the assembly line to change the production mix between LCVs and People Movers takes around [...] months and requires additional investment costs. Furthermore, and contrary to the case of car-derived vans (see Section 6.1.1.7 below), it is not possible to convert People Movers into LCVs or viceversa after production either by customers or by third-party fitters, due to the significant differences in terms of structure, functionality and equipment. 147

(129) The differences in production, time and switching costs explain why only some LCV platforms are turned into People Movers, i.e. only those for which there is sufficient sales prospect to justify incurring the additional costs. Higher costs also explain the decline in the production of segment M vehicles, including People Movers (FCA decided to cease production of the People Mover versions of the Fiat Doblò and Fiat Fiorino (Qubo nameplate) [...]).148 Conversely, there are many M-segment vehicles, such as e.g. the VW Sharan, Seat Alhambra or Citroën C4 that are not derived from LCVs.

6.1.1.6.2. The Commission’s assessment

(130) The market investigation did not reveal any evidence suggesting that People Movers should be included in the relevant LCV markets.

(131) Based on the clear lack of demand-side substitutability and limited supply-side substitutability, the Commission considers that People Movers are not part of the same product market as LCVs and should be included in the same product market as other PC models belonging to the M segment.

6.1.1.7. Car-derived vans (‘CDVs’)

(132) CDVs are, from a technical standpoint, PCs with fewer features (e.g. no rear windows or seats). In other words, a CDV is just a simpler version of a PC which is registered as a commercial vehicle (mainly for tax purposes).

(133) [...].149

6.1.1.7.1. The Notifying Parties’ views

(134) The Notifying Parties consider that each CDV belongs to the same product market as the PC from which it is derived (for example, the Fiat Panda van would belong to the same market as the PC Fiat Panda, etc.). The Notifying Parties base their view on the following:

(135) First, both [...].150

(136) Second, according to the Notifying Parties, CDVs only exist to an appreciable extent in a very limited number of EEA Member States where there is sufficient demand for them. This demand is mainly driven by tax benefits applicable to purchases by companies/professionals of commercial vehicles and only marginally driven by customer requirements (e.g., for a compact size with sufficient load capacity).

(137) In France and Italy for instance, companies can recoup VAT for CDVs. This creates the demand for CDVs and, as such, France and Italy together represent approximately [80-90]% of the total EEA CDV segment, with the United Kingdom being the only other country where sales of CDVs are above [...] units.151 The Notifying Parties submit that, if the tax benefits for CDVs were removed, demand for CDVs would decrease instantly and switch mainly to PCs.

(138) Third, whilst some CDV models (the more popular ones) are manufactured directly by OEMs, others are transformed by third party fitters (usually not linked to the OEM) who convert the PC into a CDV. Transforming a PC into a CDV can be done on the vast majority of PC models. [...].152

6.1.1.7.2. The Commission’s assessment

(139) Based on its in-depth investigation, the Commission considers that the markets for LCVs up to 3.5 tonnes should not include CDVs. CDVs should be included in the same product market as their respective PC versions.

(140) From a demand-side perspective, LCVs and CDVs are not substitutable to any appreciable extent.

(141) First, prices of CDVs, even before recouping the VAT, are similar to the prices of their PC equivalents, and are usually cheaper than small LCVs.

(142) Second, LCVs and CDVs are generally not targeted at the same customer base and switching between LCVs and CDVs is limited. This is evidenced in the first place by hesitation ratios according to which purchasers of Small LCVs very rarely hesitate towards CDVs, indicating that Small LCV purchasers do not generally see CDVs as close substitutes).153 In the second place, the replies to the market investigation support this view. Although some respondents to the market investigation indicated that there may be a limited degree of substitution between CDVs and Small LCVs,154 a majority of dealers, corporate customers, importers and leasing companies consider it appropriate to distinguish between CDVs, Small, Medium and Large LCVs.155 As explained by one competitor: “CDVs may not satisfy the same panel of needs as an LCV as a result of their limited usable capacity”.156 Another respondent stated that “these vehicles will have different usage characteristics and therefore different customer types, and therefore should be distinguished”.157

(143) Finally the Parties’ internal documents also support the view that there is limited substitutability from a demand perspective. An internal FCA presentation on LCVs explains that [...]. On the other hand, switching to PC versions of the same vehicle also represents disadvantages such as the higher taxation and the fact that the PC would be less fit for its professional mission.158

(144) Moreover, as explained by one competitor, “LCVs and [CDVs] have very different dimensions and performances”. And another competitor commented that “small LCVs do not have the required size and weight that [CDVs] offer”.159

(145) On the other hand, there is full supply-side substitutability between CDVs and the PC versions of the same model. Both vehicles are produced on the same platform/production line and it is possible to switch production from one to the other without major adaptations of the production line, in the short term and without the need to incur substantial costs. PCs can easily be transformed into CDVs by customers with minor adaptations that can be performed in a very short timeframe and with very limited cost by fitters, which would prevent any OEM from price discriminating against CDV customers. It is also possible to convert back a CDV into a PC without a major cost.160

(146) In view of all of the above, the Commission concludes that CDVs are not part of the same product market as Small LCVs and should be included in the same product market as their respective PC versions.

6.1.2. Geographic market definition

6.1.2.1. The Commission’s decisional practice

(147) In previous decisions, the Commission ultimately left open whether the market for the manufacture and supply of LCVs is EEA-wide or national in scope. However, the Commission held that there appear to be material differences in consumer preferences, prices and tax regimes across Member States, and all these elements suggest that the markets for the manufacture and supply of LCVs of up to 3.5 tonnes could be national in scope.161

6.1.2.2. The Notifying Parties’ views

(148) The Parties consider the geographic market for the manufacture and supply of LCVs to be EEA-wide in scope since: (i) The competitive conditions are largely homogeneous throughout the EEA, (ii) the production of vehicles takes place on an international level; and (iii) customers can purchase PCs and LCVs from companies located anywhere in the EEA.162

(149) First, the Parties argue that the technical, environmental and qualitative requirements for PCs and LCVs are homogeneous throughout the EEA and subject to regulations

at an EEA-level. Directive 2007/46/EC 163 requires third party approval-testing,

certification and production conformity assessment by an independent body appointed by each EEA Member State. Once a vehicle obtains approval (CE certificate) in one Member State, the approval is mutually recognised in all Member States and all the vehicles of its type can be registered in any Member State on the basis of a certificate of conformity issued by the manufacturer. Consequently, PCs and LCVs approved in one country of the EEA can be and are sold throughout the EEA, manufacturers supply the same vehicles across the EEA and there are no country-specific models (or only in a limited number of cases). Also, further regulation of the industry, such as CO2 emissions standards and the gradual ban on fluorinated greenhouse gases from mobile air-conditioning systems in motor vehicles are applied at EEA level. 164

(150) Second, all major manufacturers distribute their vehicles on an EEA-wide basis. Due to large economies of scale, any given vehicle model is produced in very few locations, i.e. one or two locations for the entire EEA market. All PCs and LCVs may be traded free of tariffs within the EEA, so long as they originate in the EEA. Transport costs are not an obstacle for cross-Member State distribution, as they constitute only around 2% of the vehicle’s total cost.165

(151) Third, customers can purchase PCs and LCVs from companies located anywhere in the EEA. Cross-border purchases are facilitated by the internet which has brought about increased price transparency. EU Competition rules, which prohibit restrictions on parallel imports, also facilitate the cross-border purchase of PCs and LCVs. Finally, warranties are provided on an EEA-wide basis, which means that the same level of security is afforded to customers purchasing PCs and LCVs from other Member States.166

6.1.2.3. The Commission’s assessment

(152) The Commission acknowledges that, as regards production, the manufacturing of LCVs is at least EEA-wide in scope. Manufacturing takes place in a centralised way in production sites from where the products are then shipped throughout the EEA (and sometimes also to/from neighbouring countries). Technical, environmental and qualitative requirements for PCs and LCVs are indeed relatively homogeneous throughout the EEA and subject to essentially the same regulations regardless of the Member State where the vehicle will be used and the certification procedure has been harmonised at EEA-level.

(153) However, from the demand-side perspective, there are important differences between EEA Member States, which are reflected in substantial differences in the market presence of the different OEMs in each Member State.

(154) First, prices differ between Member States. A majority of each customer group as well as a majority of competitors responding to the market investigation consider that prices of LCVs up to 3.5 tonnes vary between EEA Member States.167 Notably, the differences in tax regimes in different EEA Member States have an impact on the end-prices of LCVs,168 but also other factors such as customer income, commercial strategy (including discounts) and relationships with dealers/importers.169

(155) Second, customer preferences vary across EEA Member States. A majority of respondents to the market investigation highlighted that there are still some differences in customer preferences for PCs and LCVs between EEA Member States. Moreover, as it will be explained in Section 6.2.2.2, some brands enjoy a home advantage in their local country.170 A market participant explained that the results of a survey it had conducted showed that (i) the share of car buyers who had their mind set on a specific model and did not express hesitation towards any alternative varies significantly between Member States, that (ii) the same brands are perceived very differently in different national markets, even though they offer the same models with identical design and quality.171

(156) Third, whilst it is true that the legislation mentioned in Section 6.1.2.2 applies

throughout the EEA, the majority of competitors responding to the market investigation indicated that there are further regulations at national, regional or local level that have an impact on the demand of LCVs. When explaining these differences, a large number of competitors mentioned differences in taxation with a CO2 component: “[w]hile the CO2 fleet regulation is identical there are differences in particular with respect to CO2 based vehicle taxation that drives different market developments (e.g. prohibitive taxation for some vehicles in some countries versus low taxation in others)”. Other examples mentioned include “specific rules for use of cars in cities”, “road tax based on emissions” and governmental incentive schemes.172

(157) Fourth, in spite of the possibility to purchase vehicles at EEA-level, this is not common practice. The majority of corporate customers and leasing and rental companies responded that they purchase vehicles at national, rather than multi-country or EEA-level.173 A majority of dealers responded that they conclude their distribution agreements with manufacturers at national level.174 Moreover, the majority of end-customers purchase their vehicles through the local dealers.

(158) The Parties (rightly) explain that there are no barriers to distributing models produced in one EEA Member State across the entire EEA. However, the Notifying Parties’ arguments fails to explain the persistent heterogeneity in market shares across the EEA, the home advantage that domestic brands may have in certain countries and the corresponding difficulties of foreign brands’ difficulties of expanding in a market with strong domestic players, and the strongly differing national preferences.

(159) Therefore, in view of the above and the available evidence on demand-side substitutability, the Commission considers that the market for the manufacture and supply of LCVs up to 3.5 tonnes appears to be national in scope.175 Nothing in the market investigation suggested that the conclusion should be different for LCVs between 3.5 and 6 tonnes. In conclusion, for the purposes of this Decision, the Commission will analyse the impact of the Proposed Transaction mainly at national level.

(160) However, manufacturing of LCVs takes place in a centralised manner. From the production sites, OEMs ship and distribute their vehicles throughout the EEA and neighbouring countries through their own wholesalers or via importers. Importers purchase their vehicles from manufacturers located all around the EEA, regardless of the location of the production sites. Therefore, conditions for the wholesale supply of automotive vehicles take place mainly at EEA level.176 This means that competition at this level, which is reflected in the EEA-wide market shares, cannot be ignored when assessing the impact of the Proposed Transaction in each national market.

(161) Market shares at EEA level provide a useful insight on the position of the different OEMs on the supply side of the distribution chain, which is a necessary component in order to assess market power. A strong position at the supply level suggests, in the Commission’s view, a higher potential for that OEM to overcome in the medium term any limitations at the level of demand and is therefore more likely to materialise in the medium/long term in higher market shares at national level. By contrast, lower market shares at EEA-level may reflect structural weaknesses that may render more difficult the growth of a brand at national level.177

(162) For this reason, the Commission considers that it cannot assess in the same way two different product markets in the same country in which the Parties have similar market shares where their shares at EEA-wide level are substantially different. Lower combined shares at EEA-level imply that the Parties are likely to be subject to a more intense (potential) competition from other OEMs in the medium/long term at national level. For example, if the Parties were to raise prices in a specific country, whilst the short-term reaction of competitors would likely depend only on their national market shares (as these correlate strongly with diversion ratios, see section 6.2.3.2 of this Decision and section 4.1 of the LCV Economic Annex), their longterm reactions are likely to depend also on their EEA-wide shares: A competitor with a successful model may try to expand its presence in a specific country following a price increase in that country (either by using its spare capacity or by re-allocating sales away from less profitable markets), for example by increasing its marketing efforts or expanding its dealership network. Disregarding completely this component in the assessment would risk misrepresenting the economic reality on the market.

(163) The Commission therefore acknowledges the presence of some degree of out-of-market constraints from other countries. Even so, it has to be noted that geographic out-of-market constraints are limited for Small LCV as the Parties are strong in Small LCV across the EEA. Such constraints are a much more significant factor for the few Medium and Large LCV markets in which the Parties are strong, given their more moderate shares at EEA-level (and the corresponding presence of several strong competitors in these segments).

6.1.3. Conclusion on relevant markets for LCVs

(164) In view of the findings in Section 6.1, the Commission will assess the impact of the proposed transaction in the following national markets (in all cases excluding pickups):

(a) Small LCVs up to 3.5 tonnes (including both small and compact segments and excluding CDVs) (‘Small LCVs’),

(b) medium LCVs up to 3.5 tonnes (‘Medium LCVs’),

(c) large LCV up to 3.5 tonnes including semi-finished products (‘Large LCVs’),

(d) LCVs between 3.5 and 6 tonnes (including semi-finished products) (‘LCVs above 3.5 tonnes’); and

(e) Large LCVs and Large LCVs above 3.5 tonnes combined.

(165) Although the Commission will assess these markets at national level, since the conditions of wholesale supply are determined at EEA-wide level, competition at this level – which is reflected in the EEA-wide market shares – will also be taken into account in the competitive assessment.

6.2. Competitive assessment: horizontal non-coordinated effects

6.2.1. Legal test for the assessment of horizontal non coordinated effects

(166) The legal test for the assessment of horizontal non-coordinated effects is set out in the Merger Regulation and in the Guidelines on the assessment of horizontal mergers under the Council Regulation on the control of concentrations between undertakings (‘Horizontal Merger Guidelines’).178 This test will be used by the Commission in the competitive assessment of the effects of the merger in the PC markets (Section 7.2), in the LCV markets (Section 6.2) and in the markets for wholesale and retail distribution for PCs and LCVs, spare parts, components and solutions, automotive financing and other ancillary and related activities (Sections 8, 9 and 10).

(167) Under paragraphs 2 and 3 of Article 2 of the Merger Regulation, the Commission must assess whether a proposed concentration would significantly impede effective competition in the internal market or in a substantial part of it, in particular through the creation or strengthening of a dominant position. In this respect, a merger may entail horizontal and/or vertical effects.

(168) Horizontal effects are those deriving from a concentration where the undertakings concerned are actual or potential competitors of each other in one or more of the relevant markets concerned. Vertical effects are those deriving from a concentration where the undertakings concerned are active on different or multiple levels of the supply chain.

(169) The Horizontal Merger Guidelines distinguish between two main ways in which mergers between actual or potential competitors on the same relevant market may significantly impede effective competition, namely non-coordinated and coordinated effects.

(170) The Horizontal Merger Guidelines describe horizontal non-coordinated effects as follows: “A merger may significantly impede effective competition in a market by removing important competitive constraints on one or more sellers who consequently have increased market power. The most direct effect of the merger will be the loss of competition between the merging firms. For example, if prior to the merger one of the merging firms had raised its price, it would have lost some sales to the other merging firm. The merger removes this particular constraint. Non-merging firms in the same market can also benefit from the reduction of competitive pressure that results from the merger, since the merging firms’ price increase may switch some demand to the rival firms, which, in turn, may find it profitable to increase their prices. The reduction in these competitive constraints could lead to significant price increases in the relevant market”.179

(171) Therefore, a merger giving rise to such non-coordinated effects might significantly impede effective competition.

(172) Generally, a merger giving rise to such non-coordinated effects would significantly impede effective competition by creating or strengthening the dominant position of a single firm, one which, typically, would have an appreciably larger market share than the next competitor post-merger.180

(173) However, under the substantive test set out in Article 2(2) and (3) of the Merger Regulation, also mergers that do not lead to the creation or the strengthening the dominant position of a single firm may create competition concerns. Indeed, the Merger Regulation recognises that in oligopolistic markets, it is all the more necessary to maintain effective competition.181 This is in view of the more significant consequences that mergers may have on such markets. For this reason, the Merger Regulation provides that “under certain circumstances, concentrations involving the elimination of important competitive constraints that the merging parties had exerted upon each other, as well as a reduction of competitive pressure on the remaining competitors, may, even in the absence of a likelihood of coordination between the members of the oligopoly, result in a significant impediment to effective competition”.182

(174) The Horizontal Merger Guidelines list a number of factors which may influence whether or not significant horizontal non-coordinated effects are likely to result from a merger, such as the large market shares of the merging firms, the fact that the merging firms are close competitors, the limited possibilities for customers to switch suppliers, or the fact that the merger would eliminate an important competitive force.183 That list of factors applies equally regardless of whether a merger would create or strengthen a dominant position, or would otherwise significantly impede effective competition due to non-coordinated effects. Furthermore, not all of these factors need to be present to make significant non-coordinated effects likely and it is not an exhaustive list.184