GC, 10th chamber extended composition, May 10, 2023, No T-34/21

GENERAL COURT

Judgment

Annuls

PARTIES

Demandeur :

Ryanair DAC, Condor Flugdienst GmbH

Défendeur :

European Commission, Federal Republic of Germany, French Republic, Deutsche Lufthansa AG

COMPOSITION DE LA JURIDICTION

President :

A. Kornezov (Rapporteur)

Judge :

E. Buttigieg, K. Kowalik-Bańczyk, G. Hesse, D. Petrlík

Advocate :

E. Vahida, F.‑C. Laprévote, S. Rating, I.-G. Metaxas-Maranghidis, V. Blanc, A. Israel, J. Lang, E. Wright

THE GENERAL COURT (Tenth Chamber, Extended Composition),

1 By their actions on the basis of Article 263 TFEU, the applicants, Ryanair DAC and Condor Flugdienst GmbH (‘Condor’) seek annulment of Commission Decision C(2020) 4372 final of 25 June 2020 concerning State Aid SA.57153 (2020/N) – Germany – COVID-19 – Aid to Lufthansa (‘the contested decision’).

I. Background to the dispute and events subsequent to the actions being brought

2 On 12 June 2020, the Federal Republic of Germany notified the European Commission of individual aid, under Article 107(3)(b) TFEU and the Communication from the Commission of 19 March 2020 entitled ‘Temporary Framework for State aid measures to support the economy in the current COVID‑19 outbreak’ (OJ 2020 C 91 I, p. 1), as amended on 3 April 2020 (OJ 2020 C 112 I, p. 1) and 8 May 2020 (OJ 2020 C 164, p. 3) (‘the Temporary Framework’), in the form of a recapitalisation of EUR 6 billion (‘the measure at issue’) granted to Deutsche Lufthansa AG (‘DLH’).

3 DLH is the parent company of the Lufthansa Group, which, inter alia, comprises Lufthansa Passenger Airlines, Brussels Airlines SA/NV, Austrian Airlines AG, Swiss International Air Lines Ltd and Edelweiss Air AG.

4 The measure at issue is intended to restore the balance sheet position and liquidity of the undertakings in the Lufthansa Group in the exceptional situation caused by the COVID-19 pandemic. The aid is financed and managed for the German Government by the Wirtschaftsstabilisierungsfonds (Economic Stabilisation Fund, Germany) (‘the ESF’), a public entity that provides financial support at short notice to German companies affected by the COVID-19 pandemic.

5 The measure at issue consists of the following three elements:

– an equity participation of EUR 306 044 326.40;

– a ‘silent participation’ of EUR 4 693 955 673.60, which is a hybrid capital instrument treated as equity under international accounting standards (‘Silent Participation I’); and

– a ‘silent participation’ of EUR 1 billion with the features of a convertible debt instrument (‘Silent Participation II’).

6 The measure at issue is part of a wider series of support measures for the Lufthansa Group, which may be summarised, at the time the contested decision was adopted, as follows:

– a State guarantee of 80% on a loan of EUR 3 billion which the Federal Republic of Germany intended to grant to DLH under an aid scheme already approved by the Commission (Commission Decision C(2020) 1886 final of 22 March 2020 on State Aid SA.56714 (2020/N) – Germany – COVID-19 measures);

– a State guarantee of 90% on a loan of EUR 300 million which the Republic of Austria intended to grant to Austrian Airlines under an aid scheme already approved by the Commission (Commission Decision C(2020) 2354 final of 8 April 2020 on State aid SA.56840 (2020/N) – Austria – COVID-19: Austrian liquidity assistance scheme);

– a loan of EUR 150 million, which the Republic of Austria planned to grant to Austrian Airlines to compensate it for the damage resulting from the cancellation or rescheduling of its flights in the context of the COVID-19 pandemic;

– EUR 250 million in liquidity support and a loan of EUR 40 million which the Kingdom of Belgium planned to grant to Brussels Airlines;

– a State guarantee of 85% on a loan of EUR 1.4 billion granted by the Swiss Confederation to Swiss International Air Lines and Edelweiss Air.

7 On 25 June 2020, the Commission adopted the contested decision, by which it found that the measure at issue constituted State aid that was compatible with the internal market under Article 107(3)(b) TFEU and the Temporary Framework. On 20 November 2020, the Commission published information about that decision in the Official Journal of the European Union (OJ 2020 C 397, p. 2).

8 On 14 December 2021, after the present actions had been brought, the Commission adopted Decision C(2021) 9606 final, correcting the contested decision (‘the correcting decision’).

II. Forms of order sought

9 In the application lodged in Case T‑34/21, Ryanair claims that the Court should:

– annul the contested decision;

– order the Commission to pay the costs.

10 In a response to the measure of organisation of procedure of 11 May 2022, lodged on 26 May 2022, Ryanair claims, in essence, that the contested decision, as rectified by the correcting decision, should be annulled and that the Commission should be ordered to pay the costs.

11 In Case T‑87/21, Condor claims that the Court should:

– annul the contested decision;

– order the Commission to pay the costs.

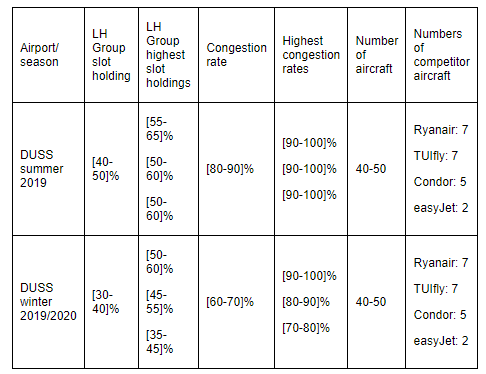

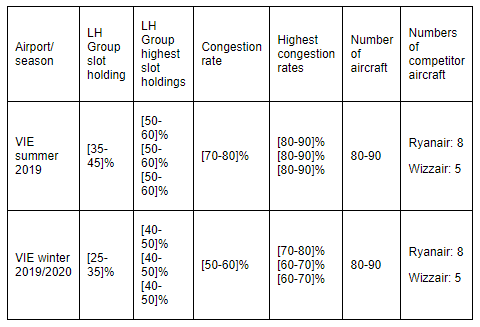

12 By a statement of modification lodged on 22 March 2022, Condor claims in addition that the Court should annul the contested decision, as rectified by the correcting decision, and order the Commission to pay the costs.

13 The Commission contends that the Court should:

– dismiss the actions;

– order the applicants to pay the costs.

14 DLH contends that the actions should be dismissed and that the applicants should be ordered to pay the costs. The Federal Republic of Germany and the French Republic, which intervened only in Case T‑34/21, contend that the action in that case should be dismissed. The Federal Republic of Germany also contends that Ryanair should be ordered to pay the costs.

III. Law

A. Admissibility of the actions

1. Ryanair’s standing to bring proceedings

15 First, Ryanair argues that it is an interested party for the purposes of Article 108(2) TFEU and Article 1(h) of Council Regulation (EU) 2015/1589 of 13 July 2015 laying down detailed rules for the application of Article 108 TFEU (OJ 2015 L 248, p.9) and that it therefore has standing to bring proceedings in order to protect its procedural rights. Second, Ryanair submits that its competitive position on the market has been substantially affected by the measure at issue and that it is also entitled to contest the contested decision on the merits.

16 The Commission does not dispute the admissibility of the action.

17 However, the French Republic maintains that Ryanair has not shown that its competitive position has been substantially affected by the measure at issue.

18 It should be borne in mind that where the Commission adopts a decision not to raise objections on the basis of Article 4(3) of Regulation 2015/1589, as in the present case, it declares not only that the measures concerned are compatible with the internal market, but also, by implication, that it refuses to initiate the formal investigation procedure laid down in Article 108(2) TFEU and Article 6(1) of that regulation (see judgment of 27 October 2011, Austria v Scheucher-Fleisch and Others, C‑47/10 P, EU:C:2011:698, paragraph 42 and the case-law cited). If, following the preliminary examination, it finds that the measure notified raises doubts as to its compatibility with the internal market, the Commission is required to adopt, on the basis of Article 4(4) of Regulation 2015/1589, a decision initiating the formal investigation procedure under Article 108(2) TFEU and Article 6(1) of that regulation. Under the latter provision, such a decision is to call upon the Member State concerned and upon other interested parties to submit comments within a prescribed period which must not as a rule exceed one month (judgment of 24 May 2011, Commission v Kronoply and Kronotex, C‑83/09 P, EU:C:2011:341, paragraph 46).

19 In the present case, the Commission decided, at the end of a preliminary examination, not to raise objections to the measure at issue on the ground that it was compatible with the internal market pursuant to Article 107(3)(b) TFEU. Since the formal investigation procedure was not initiated, the interested parties that could have submitted comments during that stage were deprived of that possibility. In order to remedy this, they are entitled to challenge the Commission’s decision not to initiate the formal investigation procedure before the EU judicature. Accordingly, an action brought by an interested party, for the purposes of Article 108(2) TFEU, for annulment of the contested decision would be admissible in so far as that party would be seeking to safeguard the procedural rights available to it under that latter provision (see judgment of 18 November 2010, NDSHT v Commission, C‑322/09 P, EU:C:2010:701, paragraph 56 and the case-law cited).

20 In the light of Article 1(h) of Regulation 2015/1589, an undertaking competing with the beneficiary of an aid measure is an ‘interested party’ for the purposes of Article 108(2) TFEU (judgment of 3 September 2020, Vereniging tot Behoud van Natuurmonumenten in Nederland and Others v Commission, C‑817/18 P, EU:C:2020:637, paragraph 50; see also, to that effect, judgment of 18 November 2010, NDSHT v Commission, C‑322/09 P, EU:C:2010:701, paragraph 59).

21 In the present case, it is not disputed that Ryanair competes with the Lufthansa Group and that, therefore, it is an interested party within the meaning of Article 1(h) of Regulation 2015/1589, having standing to bring proceedings in order to safeguard its procedural rights under Article 108(2) TFEU.

22 As to Ryanair’s standing to challenge the contested decision on the merits, it must be borne in mind that the admissibility of an action brought by a natural or legal person against an act which is not addressed to them, in accordance with the fourth paragraph of Article 263 TFEU, is subject to the condition that they be accorded standing to bring proceedings, which arises in two situations. First, such proceedings may be instituted if the act is of direct and individual concern to them. Second, such persons may bring proceedings against a regulatory act not entailing implementing measures if that act is of direct concern to them (judgments of 17 September 2015, Mory and Others v Commission, C‑33/14 P, EU:C:2015:609, paragraphs 59 and 91, and of 13 March 2018, Industrias Químicas del Vallés v Commission, C‑244/16 P, EU:C:2018:177, paragraph 39).

23 Given that the contested decision, which was addressed to the Federal Republic of Germany, does not constitute a regulatory act under the fourth paragraph of Article 263 TFEU, since it is not an act of general application (see, to that effect, judgment of 3 October 2013, Inuit Tapiriit Kanatami and Others v Parliament and Council, C‑583/11 P, EU:C:2013:625, paragraph 56), the Court must determine whether the applicant is directly and individually concerned by that decision, for the purposes of that provision.

24 In that regard, it is clear from settled case-law that persons other than those to whom a decision is addressed may claim to be individually concerned only if that decision affects them by reason of certain attributes which are peculiar to them or by reason of circumstances in which they are differentiated from all other persons and, by virtue of those factors, distinguishes them individually just as in the case of the person addressed (judgments of 15 July 1963, Plaumann v Commission, 25/62, EU:C:1963:17, p. 107; of 28 January 1986, Cofaz and Others v Commission, 169/84, EU:C:1986:42, paragraph 22; and of 22 November 2007, Sniace v Commission, C‑260/05 P, EU:C:2007:700, paragraph 53).

25 Accordingly, where an applicant calls into question the merits of a decision appraising aid, taken on the basis of Article 108(3) TFEU or after the formal investigation procedure, the mere fact that it may be regarded as a party ‘concerned’ for the purposes of Article 108(2) TFEU cannot suffice to render the action admissible. It must then demonstrate that it has a particular status for the purposes of the case-law referred to in paragraph 24 above. That applies in particular where the applicant’s position on the market concerned is substantially affected by the aid to which the decision at issue relates (see judgment of 15 July 2021, Deutsche Lufthansa v Commission, C‑453/19 P, EU:C:2021:608, paragraph 37 and the case-law cited).

26 In that regard, the Court of Justice has held that demonstration by the applicant of a substantial effect on its market position does not entail a definitive ruling on the competitive relationship between the applicant and the undertakings in receipt of aid, but requires only that the applicant adduce pertinent reasons to show that the Commission’s decision may harm its legitimate interests by substantially affecting its position on the market in question (see judgment of 15 July 2021, Deutsche Lufthansa v Commission, C‑453/19 P, EU:C:2021:608, paragraph 57 and the case-law cited).

27 It is thus apparent from the case-law of the Court of Justice that the substantial adverse effect on the applicant’s competitive position on the market in question results not from a detailed analysis of the various competitive relationships on that market, allowing the extent of the adverse effect on its competitive position to be established specifically, but, in principle, from a prima facie finding that the grant of the measure covered by the Commission’s decision leads to a substantial adverse effect on that position (see judgment of 15 July 2021, Deutsche Lufthansa v Commission, C‑453/19 P, EU:C:2021:608, paragraph 58 and the case-law cited).

28 It follows that that condition may be satisfied if the applicant adduces evidence to show that the measure concerned is liable to have a substantial adverse effect on its position on the market at issue (see judgment of 15 July 2021, Deutsche Lufthansa v Commission, C‑453/19 P, EU:C:2021:608, paragraph 59 and the case-law cited).

29 As regards the factors accepted by the case-law for the purpose of establishing a substantial adverse effect of that kind, it should be borne in mind that the mere fact that an act may exercise an influence on the competitive relationships existing on the relevant market and that the undertaking concerned is in a competitive relationship with the beneficiary of that act cannot suffice for that undertaking to be regarded as being individually concerned by that act. Therefore, an undertaking cannot rely solely on its status as a competitor of the undertaking in receipt of aid (see judgment of 15 July 2021, Deutsche Lufthansa v Commission, C‑453/19 P, EU:C:2021:608, paragraph 60 and the case-law cited).

30 Demonstrating a substantial adverse effect on a competitor’s position on the market cannot simply be a matter of the existence of certain factors indicating a decline in the applicant’s commercial or financial performance, such as a significant decline in turnover, appreciable financial losses or a significant reduction in market share following the grant of the aid in question. The grant of State aid can also have an adverse effect on the competitive situation of an operator in other ways, in particular by causing the loss of an opportunity to make a profit or a less favourable development than would have been the case without such aid (judgment of 15 July 2021, Deutsche Lufthansa v Commission, C‑453/19 P, EU:C:2021:608, paragraph 61).

31 In addition, the case-law does not require that the applicant provide information as to the size or geographical scope of the markets at issue, or as to its market shares and those of the recipient of the aid measure at issue or of other competitors on those markets (see, to that effect, judgment of 15 July 2021, Deutsche Lufthansa v Commission, C‑453/19 P, EU:C:2021:608, paragraph 65).

32 It is in the light of those principles that it is necessary to examine whether Ryanair has adduced evidence to show that the measure at issue is liable to have a substantial adverse effect on its position on the market concerned.

33 In that regard, Ryanair submits that it is the closest and most relevant competitor of the Lufthansa Group. Accordingly, in 2019 it was the second-largest airline on the German and Belgian markets after the Lufthansa Group and the third largest on the Austrian market. In addition, in that same year, it competed directly with the Lufthansa Group on 96 routes departing from or arriving in Germany, 27 of which were operated only by it and the Lufthansa Group, while there were few competitors on the remaining routes. As regards Belgium and Austria, Ryanair is in direct competition with the Lufthansa Group on 46 and 35 routes respectively, certain of which are operated only by it and that group. Moreover, several of the routes concerned are of economic importance in that they connect large cities in Europe and beyond.

34 The French Republic contends, however, that Ryanair has not adduced evidence capable of demonstrating that it is substantially affected by the measure at issue at the relevant airports, as identified in the contested decision. In particular, the measure at issue does not have a substantial effect on Ryanair’s competitive position at the airports of Vienna (Austria), Brussels (Belgium), Hamburg (Germany) and Palma de Mallorca (Spain), where, according to the contested decision, the Lufthansa Group did not have significant market power (‘SMP’). Furthermore, Ryanair is not one of the Lufthansa Group’s main competitors at Munich Airport (Germany), while at Frankfurt Airport (Germany), it has a low level of operations despite the fact that it is the second-largest airline, after the Lufthansa Group.

35 In the first place, the objection put forward by the French Republic raises the question, as a preliminary matter, of whether the evidence adduced by Ryanair and summarised in paragraph 33 above lacks any relevance for the purpose of assessing its standing to bring proceedings in that it does not refer specifically to its competitive position at the airports referred to in paragraph 34 above. That objection results, in essence, from the fact that the Commission identified the relevant markets for passenger air transport services in the contested decision according to the ‘airport-by-airport’ approach. Under that approach, each airport is defined as a distinct market, without differentiating between the specific routes operated to or from that airport.

36 Ryanair argues in the fifth part of its first plea, inter alia, that the Commission was wrong to take that approach and that it should have defined the markets at issue under an approach based on pairs of cities, designated as the point of origin and the point of destination (‘the O&D approach’).

37 In that regard, it should be borne in mind that it is not necessary, at the stage of examining the admissibility of an action, to give a definitive ruling on the definition of the market for the products or services at issue or on the competitive relationship between the applicant and the beneficiary. It is sufficient, in principle, for the applicant to show that, prima facie, the grant of the measure at issue leads to a substantial adverse effect on its competitive position on the market (see the case-law cited in paragraphs 26 and 27 above).

38 Consequently, at the stage of examining the admissibility of an action, where the definition of the market at issue is challenged as to its merits by the applicant, as in the present case, it is sufficient to assess whether the definition of the market at issue put forward by the applicant is plausible, that being without prejudice to the substantive examination of that issue.

39 In the present case, the Court considers that defining the markets for passenger air transport services according to the O&D approach, as advocated by Ryanair, is prima facie plausible. It need only be observed that, as regards the airline sector, the Court has accepted that the Commission could employ that approach in order to define the relevant markets, in particular in the area of merger control (see, to that effect, judgment of 13 May 2015, Niki Luftfahrt v Commission, T‑162/10, EU:T:2015:283, paragraphs 139 and 140 and the case-law cited).

40 The information provided by Ryanair, summarised in paragraph 33 above, is therefore relevant for the purpose of examining its standing to bring proceedings.

41 In the second place, it is apparent from that information, the accuracy of which is not contested by the parties, and which is furthermore confirmed by the evidence provided by Ryanair in these proceedings, that Ryanair and the Lufthansa Group were, before the adoption of the contested decision, in competition on a large number of routes between pairs of cities, defined as points of origin and points of departure (‘O&D routes’) to and from Belgium, Germany and Austria, and that Ryanair and the Lufthansa Group were the only competitors on a considerable number of O&D routes. Nor do the parties contest the fact that Ryanair is the second-largest airline, after the Lufthansa Group, on the Belgian and German markets and the third largest on the Austrian market.

42 In the third place, and in any event, it must be stated that the Commission, in the contested decision, identified Ryanair as one of the main competitors of the Lufthansa Group at several of the relevant airports. Accordingly, it is apparent from paragraphs 188 and 189 of the contested decision that Ryanair was the second- and third-largest competitor of the Lufthansa Group at Frankfurt Airport, in terms of the number of slots held, during the 2019/2020 winter season and the 2019 summer season of the International Air Transport Association (IATA) respectively. It was also the second-largest airline in terms of the number of aircraft based at that airport during those seasons. Similarly, according to the contested decision, Ryanair was the Lufthansa Group’s closest competitor at Düsseldorf (Germany) and Vienna (Austria) airports.

43 In the fourth place, Ryanair submits that it was pursuing expansion goals on the Belgian, German and Austrian markets, launching, respectively, 9, 75 and 28 new routes on those markets in 2019, which is also not disputed. In addition, according to Ryanair, the Lufthansa Group could use the capital obtained through the measure at issue to lower its prices and strengthen its competitive position on the market to Ryanair’s detriment, particularly in the context of the COVID-19 pandemic, which has impacted all airlines.

44 In that regard, it is apparent from paragraph 16 of the contested decision that without the measure at issue DLH risked becoming insolvent, which could have caused the collapse of the Lufthansa Group as a whole. Furthermore, according to a report of May 2020 by the Fondation pour l’innovation politique, submitted by Ryanair and entitled ‘Before COVID-19, air transportation in Europe: an already fragile sector’, the content of which has not been contested by the parties, it was ‘likely that Ryanair and Wizz Air will emerge from the [COVID-19] crisis without too much damage and will even have enough financial resources, especially through indebtedness and the purchase of bankrupt companies, to take part in the probable restructuring of air transport in Europe’. It thus follows that Ryanair was in a relatively strong position in relation to the traditional airlines, such as those belonging to the Lufthansa Group, which faced a risk of insolvency or even exit from the market.

45 The factors set out in paragraphs 33 to 44 above, taken together, show that Ryanair has demonstrated that the grant of the measure at issue led prima facie to a substantial adverse effect on its competitive position on the market by causing, inter alia, the loss of an opportunity to make a profit or a less favourable development than would have been the case without such a measure (see the case-law cited in paragraph 30 above).

46 That finding is not called into question by the objection raised by the French Republic that Ryanair has not shown that the contested decision affects it by reason of circumstances that differentiate it from all the other competitors of the Lufthansa Group.

47 The condition that there be a substantial effect on the applicant’s competitive position is a factor that is particular to that applicant, which must be assessed solely in relation to its market position prior to the grant of the measure at issue or in its absence. It is therefore not a matter of comparing the situation of all the competitors operating on the market in question (see, to that effect, Opinion of Advocate General Szpunar in Deutsche Lufthansa v Commission, C‑453/19 P, EU:C:2020:862, point 58). Moreover, as observed in paragraph 31 above, the Court of Justice has explained that it is not necessary for the applicant to provide information concerning its market shares, those of the beneficiary or of other competitors on that market. It thus follows that, in order to show that there has been a substantial effect on its competitive position, the applicant cannot be required to establish, with supporting evidence, what the competitive situation of its competitors is and to differentiate itself from that situation.

48 In addition, it is important to observe that the case-law cited in paragraph 24 above foresees two different criteria for showing that persons other than those to whom a decision is addressed are individually concerned by that decision, namely that the contested decision affects them ‘by reason of certain attributes which are peculiar to them’ or ‘by reason of circumstances in which they are differentiated from all other persons’. That case-law does not therefore require an applicant to show that, in every case, its factual circumstances are different from those of any other person. It is sufficient that the contested decision affects the applicant by reason of certain attributes which are peculiar to it.

49 That is the case here. All of the factors referred to in paragraphs 33 to 44 above tend to show, in a sufficiently plausible manner, that Ryanair’s position on the markets concerned was characterised by certain attributes peculiar to it, such as its significant presence on those markets, the fact that it is the closest competitor of the beneficiary on certain of them, its plans for expansion on the Belgian, German and Austrian markets, and its relatively strong financial situation in comparison with the weak position of the beneficiary, thus putting it in a position that may allow it to gain market share, in the absence of the aid, to the detriment of the beneficiary.

50 In the light of all the foregoing, it must be held that Ryanair has shown to the requisite legal standard that the measure at issue was liable to have a substantial effect on its competitive position on the market concerned.

51 As to the whether Ryanair is directly concerned by the contested decision, it is important to observe that, according to settled case-law, a competitor of a beneficiary of aid is directly concerned by a Commission decision authorising a Member State to pay the aid when there is no doubt as to that State’s intention to do so (see, to that effect, judgment of 5 May 1998, Dreyfus v Commission, C‑386/96 P, EU:C:1998:193, paragraphs 43 and 44, and of 15 September 2016, Ferracci v Commission, T‑219/13, EU:T:2016:485, paragraph 44 and the case-law cited), as is the case in this instance.

52 Ryanair is therefore entitled to challenge the contested decision on the merits.

2. The standing of Condor to bring proceedings

53 First, Condor claims that it is an interested party for the purposes of Article 108(2) TFEU and Article 1(h) of Regulation 2015/1589 and that it therefore has standing to bring proceedings in the present case in order to safeguard its procedural rights, on the ground that it is a competitor of the Lufthansa Group. Second, Condor submits that its position on the market has been substantially affected by the measure at issue and that it is therefore also entitled to challenge the contested decision on the merits.

54 The Commission does not dispute that Condor is an interested party and that it therefore has standing to bring proceedings in order to safeguard its procedural rights. However, it states that it ‘doubts’ that Condor has shown to the requisite legal standard that it was substantially affected by the measure at issue.

55 In the first place, it is common ground that Condor is a competitor of the Lufthansa Group and that it is therefore an interested party for the purposes of Article 1(h) of Regulation 2015/1589 and Article 108(2) TFEU (see the case-law cited in paragraph 20 above). Consequently, Condor has standing to bring proceedings in order to safeguard its procedural rights.

56 In the second place, as regards whether Condor also has standing to challenge the contested decision on the merits, it must be observed that in order to demonstrate that the measure at issue has a substantial effect on its competitive position on the market, the applicant submits, first, that it is the Lufthansa Group’s only competitor on 51 O&D routes to and from Germany and that it is in direct competition with that group on 79 other routes. In addition, on the 130 routes in total operated by both Condor and the Lufthansa Group, those airlines offered a total of 18.6 million seats, of which Condor offered 6.33 million.

57 Without disputing the accuracy of those figures, the Commission submits that Condor has failed to specify the source for that information and the period to which it relates.

58 While it is true, as the Commission asserts, that Annex C.1 to Condor’s reply, which includes the list of O&D routes referred to in paragraph 56 above, provides neither the source of the data in that annex nor the period to which they relate, it is nevertheless the case that that annex must be read in conjunction with the written pleadings lodged by Condor. In that regard, it is apparent from Condor’s application that the data in question originate from the ‘SRS’ Analyser, an IATA partner, which is an online database containing a large amount of data on various airlines’ routes, schedules and number of seats, as consulted online on 1 December 2020. The Commission does not dispute the reliability of that source. In addition, Condor states in its application that those data relate to the period from April 2019 to March 2020, a period corresponding approximately to the IATA 2019 summer season and the 2019/2020 winter season, and thus to the period examined in the contested decision.

59 The objection raised by the Commission must therefore be rejected.

60 Having clarified that issue, the Court considers, for the reasons set out in paragraphs 34 to 39 above, applied mutatis mutandis, that the information provided by Condor and summarised in paragraph 56 above is relevant for the purpose of examining whether the measure at issue is prima facie liable to have a substantial effect on its competitive position on the market, that being without prejudice to the substantive examination of the definition of the relevant market.

61 It is apparent from that information that Condor and the Lufthansa Group were in competition on a large number of O&D routes to and from Germany, that Condor was the group’s only competitor on many of those routes, and that the number of seats available on the flights operated by Condor on all those routes was substantial.

62 Second, it should be observed, as Condor has done, that, in paragraphs 188, 189, 195, 196 and 202 of the contested decision, the Commission itself identified Condor as being the second- and third-largest airline at Frankfurt Airport, in terms of slots, during the IATA 2019 summer season and the 2019/2020 winter season respectively. Furthermore, again according to the Commission’s findings, Condor was the second-largest airline at Munich and Düsseldorf airports, in terms of based aircraft, and the third-largest in terms of slots at Munich Airport during the IATA 2019 summer season. It thereby follows that Condor, according to the contested decision itself, has been identified as being one of the main competitors to the Lufthansa Group at several of the airports examined in that decision.

63 Third, Condor submits that it had a long-standing commercial relationship with the Lufthansa Group, as shown by the agreement on feeder traffic that it had concluded with that group. In that regard, it is not disputed that Condor, which, inter alia, operates long-haul leisure flights, depends to a large extent on feeder traffic from short-haul flights operated by the Lufthansa Group in order to fill its flights. According to Condor, that group was the only airline operating a network at any of the German airports capable of providing sufficient feeder traffic. According to Condor, which is not contradicted on this point, approximately 25% of all the passengers on any of its long-haul flights use a feeder or a de-feeder flight operated by the Lufthansa Group. The latter also provides 90% of the ‘indirect’ passengers who fly on long-haul flights operated by Condor. It is apparent from those factors that the feeder traffic thus generated by the Lufthansa Group is of particular importance for Condor’s operations.

64 Fourth, as observed in paragraph 44 above, it is apparent from the contested decision that without the measure at issue DLH risked becoming insolvent, which could have caused the collapse of the Lufthansa Group as a whole.

65 However, according to Condor, the measure at issue enabled the Lufthansa Group to remain on the market and even to launch new routes which it did not operate previously.

66 In the light of all the foregoing factors, it should be found that Condor has shown to the requisite legal standard that the measure at issue was liable to have a substantial effect on its competitive position on the markets for the transport of passengers by air.

67 For the same reasons as those set out in paragraph 51 above, Condor is also directly concerned by the contested decision, with the result that it is entitled to challenge the contested decision on the merits.

B. Substance

68 In support of its action in Case T‑34/21, Ryanair puts forward five pleas in law, alleging respectively, first, misapplication of the Temporary Framework and misuse of powers; second, misapplication of Article 107(3)(b) TFEU; third, infringement of certain specific provisions of the FEU Treaty and certain general principles of EU law, namely non-discrimination, the freedom to provide services and freedom of establishment; fourth, failure by the Commission to initiate the formal investigation procedure provided for in Article 108(2) TFEU; and, fifth, infringement of the obligation to state reasons.

69 In particular, the first plea consists of seven parts, concerning, respectively: (i) DLH’s eligibility for the aid under the Temporary Framework; (ii) the existence of other more appropriate measures and whether they entailed fewer distortions to competition; (iii) the amount of the recapitalisation; (iv) the remuneration and exit of the State; (v) whether the beneficiary held SMP on the relevant markets and the structural commitments imposed in order to preserve effective competition on those markets; (vi) the prohibition of aggressive commercial expansion financed by the aid; and (vii) misuse of powers.

70 In support of its action in Case T‑87/21, Condor raises three pleas in law, alleging respectively, first, infringement by the Commission of its obligation to initiate the formal investigation procedure provided for in Article 108(2) TFEU; second, a manifest error of assessment in that the Commission found that the measure at issue was compatible with the internal market under Article 107(3)(b) TFEU; and, third, infringement of the obligation to state reasons. The Court observes that there is a partial overlap in content between the first two pleas. When questioned on that matter at the hearing, Condor confirmed that overlap, indicating that those pleas were raised in anticipation of the Court’s decision on the admissibility of the action and that they concerned, in essence, the same issues. Since the Court has held that Condor is entitled to challenge the merits of the contested decision, those two pleas should be examined together. In essence, four issues are raised, namely the eligibility of the beneficiary for the aid under the Temporary Framework, the amount of the recapitalisation, the prohibition of aggressive commercial expansion financed by the aid, and the existence of SMP on the part of the beneficiary on the relevant markets, as well as the structural commitments.

71 It thus follows that the first plea in Case T‑34/21 and the first two pleas in Case T‑87/21 in part raise questions that are similar, which should be examined together, and in part raise questions that are different. All of those questions may be grouped together into six issues, as follows:

– DLH’s eligibility for the aid (first part of the first plea in Case T‑34/21 and second part of the first plea in Case T‑87/21);

– whether there were other measures that were more appropriate and that created fewer distortions to competition (second part of the first plea in Case T‑34/21);

– the amount of the aid (third part of the first plea in Case T‑34/21 and second part of the first and second pleas in Case T‑87/21);

– the remuneration and exit of the State (fourth part of the first plea in Case T‑34/21);

– the prohibition of aggressive commercial expansion financed by the aid (sixth part of the first plea in Case T‑34/21 and first part of the first plea and second part of the second plea in Case T‑87/21);

– whether the beneficiary held SMP on the markets at issue and the structural commitments (fifth part of the first plea in Case T‑34/21 and first part of the first and second pleas in Case T‑87/21).

72 It is appropriate first of all to make some preliminary observations before examining those issues and, if necessary, the other pleas raised by the applicants.

1. Preliminary observations

(a) The intensity of judicial review

73 As a preliminary point, it should be borne in mind that the assessment of the compatibility of aid measures with the internal market, under Article 107(3) TFEU, falls within the exclusive competence of the Commission, subject to review by the Courts of the European Union (judgment of 19 July 2016, Kotnik and Others, C‑526/14, EU:C:2016:570, paragraph 37).

74 In that regard, it is settled case-law that the Commission enjoys wide discretion, the exercise of which involves complex economic and social assessments (see judgment of 19 July 2016, Kotnik and Others, C‑526/14, EU:C:2016:570, paragraph 38 and the case-law cited). Article 107(3) TFEU confers on the Commission broad discretion to allow aid by way of derogation from the general prohibition laid down in Article 107(1) TFEU, inasmuch as the determination, in those cases, of whether State aid is compatible or incompatible with the internal market raises problems which make it necessary to examine and appraise complex economic facts and conditions (judgments of 18 January 2012, Djebel – SGPS v Commission, T‑422/07, not published, EU:T:2012:11, paragraph 107, and of 1 March 2016, Secop v Commission, T‑79/14, EU:T:2016:118, paragraph 29). In that context, judicial review of the manner in which that discretion is exercised is confined to establishing that the rules of procedure and the rules relating to the duty to give reasons have been complied with, and to verifying the accuracy of the facts relied on and that there has been no error of law, manifest error in the assessment of the facts or misuse of powers (see judgment of 11 September 2008, Germany and others v Kronofrance, C‑75/05 P and C‑80/05 P, EU:C:2008:482, paragraph 59 and the case-law cited).

75 However, in the exercise of that discretion, the Commission may adopt guidelines in order to establish the criteria on the basis of which it proposes to assess the compatibility, with the internal market, of aid measures envisaged by the Member States. In adopting such guidelines and announcing by publishing them that they will apply to the cases to which they relate, the Commission imposes a limit on the exercise of that discretion and cannot, as a general rule, depart from those guidelines, at the risk of being found to be in breach of general principles of law, such as equal treatment or the protection of legitimate expectations (judgment of 19 July 2016, Kotnik and Others, C‑526/14, EU:C:2016:570, paragraphs 39 and 40). Nevertheless, the adoption of guidelines by which the Commission limits its discretion does not relieve the Commission of its obligation to examine the specific exceptional circumstances relied on by a Member State, in a particular case, for the purpose of requesting the direct application of Article 107(3)(b) TFEU. Consequently, the Commission may authorise proposed aid that departs from those guidelines in exceptional circumstances (see, to that effect, judgment of 19 July 2016, Kotnik and Others, C‑526/14, EU:C:2016:570, paragraphs 41 and 43).

76 Accordingly, in the specific area of State aid, the Commission is bound by the guidelines and notices that it issues, to the extent that they do not depart from the rules in the Treaty (see judgment of 2 December 2010, Holland Malt v Commission, C‑464/09 P, EU:C:2010:733, paragraph 47 and the case-law cited). It is therefore for the Courts of the European Union to determine whether the Commission has observed the rules which it adopted (see judgment of 8 April 2014, ABN Amro Group v Commission, T‑319/11, EU:T:2014:186, paragraph 29 and the case-law cited).

77 Furthermore, in the context of the review conducted by the Courts of the European Union on complex economic assessments carried out by the Commission in the field of State aid, it is true that it is not for those Courts to substitute their own economic assessment for that of the Commission. However, the Courts of the European Union must, inter alia, establish not only whether the evidence relied on is factually accurate, reliable and consistent but also whether that evidence contains all the relevant information which must be taken into account in order to assess a complex situation and whether it is capable of substantiating the conclusions drawn from it (judgment of 24 January 2013, Frucona Košice v Commission, C‑73/11 P, EU:C:2013:32, paragraphs 75 and 76; see, also, judgment of 24 October 2013, Land Burgenland and Others v Commission, C‑214/12 P, C‑215/12 P and C‑223/12 P, EU:C:2013:682, paragraph 79 and the case-law cited). Likewise, the Courts of the European Union must review the Commission’s interpretation of information of an economic nature (see, to that effect, judgment of 22 November 2007, Spain v Lenzing, C‑525/04 P, EU:C:2007:698, paragraph 56).

78 Consequently, although the review carried out by the Courts of the European Union is limited as regards the complex economic and social assessments made by the Commission, as is apparent from the case-law referred to in paragraph 74 above, that review is, by contrast, comprehensive as regards the evaluations made by the Commission which do not involve such assessments or as regards questions of a strictly legal nature.

(b) The probative value of the expert reports

79 In Case T‑34/21, Ryanair relies in various respects on several expert reports, including:

– a report drawn up by Oxera entitled ‘Assessment of the Commission’s analysis of the proportionality of the aid to DLH’ of 21 January 2021 (‘Oxera report I’);

– a report by Oxera called ‘Assessment of the Commission’s approach to determining SMP and competitive distortions’ of 21 January 2021 (‘Oxera report II’);

– the report by the Fondation pour l’innovation politique referred to in paragraph 44 above;

– a report entitled ‘Rating Action: Moody’s downgrades Lufthansa to Ba1, ratings placed on review for downgrade’ of 17 March 2020 by Moody’s (‘the Moody’s report’); and

– a report with the title ‘European Airlines, All is not what it seems’ of 17 April 2020 written by J. Hollins, R. Joynson and D. Maglione of Exane BNP Paribas (‘the Exane report’).

80 The Court, as a preliminary point, must assess the probative value of those reports.

81 In that regard, it should be borne in mind that given that there is no legislation at EU level governing the concept of proof, the Courts of the European Union have laid down a principle of unfettered production of evidence or freedom as to the form of evidence adduced, which is to be interpreted as the right to rely, in order to prove a particular fact, on any form of evidence, such as oral testimony, documentary evidence, confessions, expert reports and so on. Correspondingly, it is settled case-law that the determination of reliability or, in other words, the probative value of an item of evidence is a matter for those Courts. Accordingly, in order to establish the probative value of a document, it is necessary to take account of several factors, such as the origin of the document, the circumstances in which it was drawn up, the person to whom it was addressed and its content, and to consider whether, according to those aspects, the information it contains appears sound and reliable (see judgment of 2 July 2019, Mahmoudian v Council, T‑406/15, EU:T:2019:468, paragraphs 136 and 137 and the case-law cited).

82 In the present case, in the first place, as regards the Moody’s and Exane reports, it should be noted that those reports were not prepared at the request of Ryanair, they have no connection with these judicial proceedings and their authors are third parties whose expertise, reputation and independence with respect to Ryanair are not in dispute.

83 In the second place, as regards the Oxera reports I and II, it should be observed that they were prepared at Ryanair’s request for the purpose of the present proceedings.

84 However, the Commission, the Federal Republic of Germany, the French Republic and DLH neither dispute the probative value of those reports nor challenge the accuracy or veracity of the factual and financial information they contain.

85 In addition, the Court observes that those reports were drawn up on the basis of information that was publicly available or which originated from reputable and reliable sources that were independent of Ryanair. The Oxera reports I and II are based on information from sources such as the Airports Council International (ACI) Europe association, IATA, several ratings agencies such as Moody’s, the Kroll Bond Rating Agency and S&P, the Financial Times, DLH or other airlines, the German authorities and the contested decision itself.

86 Lastly, while it is true that those reports post-date the adoption of the contested decision, the fact remains that they are based on data that existed at the time the contested decision was adopted. In that regard, according to the case-law, the fact that the review carried out by the Court hearing an application for annulment is carried out solely by reference to the elements of fact and of law existing on the date of adoption of the contested decision is without prejudice to the possibility afforded to the parties, in the exercise of their rights of defence, of supplementing them by evidence established after that date, but for the specific purpose of contesting or defending that decision (see judgment of 27 September 2006, GlaxoSmithKline Services v Commission, T‑168/01, EU:T:2006:265, paragraph 58 and the case-law cited).

87 In those circumstances, the Court finds that the reports referred to in paragraph 79 above have probative value.

2. The eligibility of DLH for the aid

88 In Case T‑34/21, Ryanair puts forward three complaints concerning the eligibility of DLH for the aid, alleging, respectively, infringement of the conditions laid down in points 49(a), 49(b) and 49(c) of the Temporary Framework. That third complaint and the arguments raised by Condor in Case T‑87/21 to the effect that the Commission disregarded the conditions set out in point 49(c) of the Temporary Framework overlap. Those complaints should be examined in turn.

(a) Infringement of point 49(a) of the Temporary Framework

89 Ryanair argues in essence that the Commission has not shown that, without the aid, the beneficiary would necessarily become insolvent or face serious difficulties in maintaining its operations, for the purposes of point 49(a) of the Temporary Framework. In addition, the Commission confused the concepts of illiquidity, which arises when an undertaking is unable to pay its debts when they are due, and insolvency, which occurs when the total value of the undertaking’s liabilities exceeds that of its assets.

90 The Commission, supported by the Federal Republic of Germany and DLH, disputes those arguments.

91 Point 49 of the Temporary Framework, which appears in section 3.11.2, entitled ‘Eligibility and entry conditions’, sets out the conditions that a recapitalisation measure granted in the context of the COVID-19 pandemic must fulfil for a potential beneficiary to be considered eligible for that measure.

92 The first of those conditions, laid down in point 49(a) of the Temporary Framework, requires establishing that without the State intervention the beneficiary would go out of business or would face serious difficulties in maintaining its operations. The Commission based its finding that that condition was satisfied on the second situation. In accordance with that same point of the Temporary Framework, those difficulties may be shown by the deterioration, in particular, of the debt-to-equity ratio of the beneficiary of the State intervention or similar indicators.

93 In paragraphs 96 to 98 of the contested decision, the Commission noted that DLH’s impaired equity position severely affected its liquidity and threatened it with insolvency in the short term. That finding was based on internal documents and financial projections for the years 2020 to 2026, provided by the German Government. They showed that DLH’s equity would decrease significantly by the end of 2020 as compared to 2019 and that, despite measures taken in 2020 to obtain liquidity, it would face ‘technical illiquidity’, which meant that the liquid assets available to it would not be sufficient to repay its debts when they became due, something which Ryanair does not dispute. The Commission thus concluded that the measure at issue would prevent DLH’s insolvency and that, consequently, in the absence of a capital increase, it would face serious difficulties in maintaining its operations.

94 It should, in addition, be observed that in the contested decision the Commission pointed to a deterioration in DLH’s debt-to-equity ratio, as provided for in point 49(a) of the Temporary Framework (see Table 1 in paragraph 117 of the contested decision). Ryanair does not dispute those figures.

95 Accordingly, the Commission did not infringe point 49(a) of the Temporary Framework.

96 The argument raised by Ryanair, based on a distinction between the concepts of illiquidity and insolvency, must be rejected as ineffective. Point 49(a) of the Temporary Framework does link eligibility for the aid to those concepts but makes it dependent, inter alia, on the undertaking in question facing serious difficulties in maintaining its operations.

97 As regards the claim that the Commission failed to demonstrate that it was not possible to envisage another, less distortive, measure for targeting the beneficiary’s liquidity problems, that argument overlaps with the issue raised in the second part of the first plea, which will be examined below.

98 The present complaint must therefore be rejected as unfounded.

(b) Infringement of point 49(b) of the Temporary Framework

99 Ryanair complains, in essence, that the Commission infringed point 49(b) of the Temporary Framework in that it did not demonstrate the systemic nature of DLH for the German economy.

100 The Commission, supported by the Federal Republic of Germany and DLH, disputes that line of argument.

101 Point 49(b) of the Temporary Framework provides that the planned recapitalisation measure must be in the common interest. The existence of such a common interest may be shown if the measure at issue is aimed at avoiding social hardship and market failure due to a significant loss of employment, the exit of an innovative or a systemically important company, the risk of disruption to an important service, or similar situations duly substantiated by the Member State concerned.

102 The Commission noted in paragraph 99 of the contested decision that DLH was of systemic importance for the German economy in several respects, namely, notably, for employment, connectivity and foreign trade, and that, therefore, it was in the common interest to intervene. In particular, it is apparent from paragraphs 36 to 38 of the contested decision that, first, DLH is a major employer, with more than 135 000 staff, including 73 000 at the airport hubs in Germany. Second, given that it operates flights to 301 destinations in 100 countries, DLH plays an important role in Germany’s connectivity, not only for short-haul but also for long-haul flights. Third, DLH contributes to a significant part of the volume of foreign trade by air freight in Germany, which is of great importance for an export-oriented economy such as that of Germany. In addition, it is apparent from paragraph 14 of the contested decision that DLH’s air freight services also played a vital role in the transport of protective masks and medical material from China to Europe during the COVID-19 pandemic. Lastly, paragraph 36 of the contested decision shows that DLH’s operations make an important contribution to the budget of the State in the form of social security contributions, income tax payments and taxes on air transport.

103 It must be stated that Ryanair does not dispute those figures, but argues, in essence, that they are not sufficient to show that DLH is of systemic importance for the German economy. According to Ryanair, the concept of a systemically important company within the meaning of point 49(b) of the Temporary Framework must be interpreted as referring to undertakings whose failure would lead to the collapse of the entire sector in which they operate.

104 However, the interpretation advocated by Ryanair cannot succeed. There is nothing in the wording of point 49(b) of the Temporary Framework to suggest that only undertakings whose exit from the market would lead to the collapse of an entire sector are eligible for aid. Furthermore, an overall reading of point 49(b) of the Temporary Framework, and in particular of the examples of cases in which it is in the common interest to intervene, such as the risk of social hardship, of a significant loss of employment or even of disruption to an important service, shows that the interpretation put forward by Ryanair is too restrictive.

105 In support of that interpretation, Ryanair refers in addition to the Commission’s decision-making practice in the financial sector and to the State aid rules applicable in that sector (in particular, the Communication from the Commission on the application, from 1 August 2013, of State aid rules to support measures in favour of banks in the context of the financial crisis (OJ 2013 C 216, p. 1), and Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms, amending Directive 2002/87/EC and repealing Directives 2006/48/EC and 2006/49/EC (OJ 2013 L 176, p. 338). In that regard, it is sufficient to observe that the legality of the contested decision must be assessed solely in the context of Article 107(3)(b) TFEU and the Temporary Framework, and not in the light of an alleged earlier practice (see, to that effect, judgment of 27 February 2013, Nitrogénművek Vegyipari v Commission, T‑387/11, not published, EU:T:2013:98, paragraph 126 and the case-law cited); nor indeed should it be assessed in the light of the Communication from the Commission on the application, from 1 August 2013, of State aid rules to support measures in favour of banks in the context of the financial crisis, or Directive 2013/36, referred to by Ryanair, since they are not applicable in the present case.

106 The other arguments put forward by Ryanair must also be rejected.

107 First, contrary to what Ryanair maintains, the Commission was under no obligation to assess whether DLH could easily be replaced by other airlines. Such a requirement is not set out in point 49(b) of the Temporary Framework, which is the rule allegedly infringed.

108 Second, the fact that the Commission did not provide any market share for DLH in the contested decision in order to prove its systemic importance for the German economy is not capable of invalidating the Commission’s analysis on that point. An undertaking’s systemic importance may be established on the basis of many other factors, such as those summarised in paragraph 101 above, which establish to the requisite legal standard that the condition laid down in point 49(b) was satisfied.

109 Third, Ryanair’s argument that the Commission relied on the information provided by the Federal Republic of Germany, without performing its own ‘autonomous’ assessment, has no basis in fact. It is apparent from footnotes 25 and 26 to the contested decision that the Commission also verified certain information by reference to independent sources, such as IATA. In addition, it is apparent from paragraph 99 of the contested decision that the Commission assessed the evidence submitted by the Federal Republic of Germany and found it to be reliable.

110 Fourth, Ryanair complains that the Commission failed to examine the possibility of a reduction in the size or operations of DLH. However, it must be observed that point 49(b) of the Temporary Framework does not prescribe such a condition for eligibility.

111 Consequently, this complaint must be rejected as unfounded.

(c) Infringement of point 49(c) of the Temporary Framework

112 In the first part (third complaint) of its first plea, Ryanair claims in essence that the Commission infringed point 49(c) of the Temporary Framework by reaching the conclusion that DLH was unable to obtain financing on the markets at affordable terms and that, in that regard, the Commission failed to take account of all the relevant factors. Condor, in the second part (first complaint) of its first plea, submits that the Commission’s analysis in that respect is incomplete and insufficient and therefore reveals the existence of serious doubts.

113 The Commission, supported by DLH, disputes those arguments. It contends, in essence, that the applicants have not adduced any concrete evidence that market financing was available to the beneficiary at affordable terms, taking account of the latter’s financing needs and the time constraints.

114 Point 49(c) of the Temporary Framework states that, in order to be eligible for a recapitalisation measure, the beneficiary must, inter alia, be unable to find financing on the markets at affordable terms.

115 In paragraphs 21 to 24 and 100 of the contested decision, the Commission concluded that that condition was fulfilled on the ground, inter alia, that DLH would be unable to obtain financing on the debt markets since investors would not be willing to provide funds without sufficient securities to protect their claims in the event of default. According to the Commission, DLH would not have had sufficient collateral for securitised debt instruments over the entire amount at issue. In addition, the Commission stated that the total amount of EUR 9 billion needed to preserve the continuity of the group’s economic activity during and after the COVID-19 outbreak exceeded the total volume of debt issued in Europe in the preceding months.

116 Ryanair counters, in essence, that the Commission failed to examine whether it was possible for DLH to find at least part of its financing on the markets by offering collateral for securitised debt, such as its fleet of aircraft, its slots or its frequent-flyer programme.

117 In that regard, it must be stated that the question of whether DLH was unable to obtain financing on the markets at affordable terms involves complex economic assessments relating to the beneficiary’s overall financial situation and the functioning of the financial markets, with the result that the review conducted by the Courts of the European Union of that type of assessment is limited. However, in accordance with the case-law referred to in paragraph 77 above, the Courts of the European Union must establish not only whether the evidence relied on is factually accurate, reliable and consistent, but also whether that evidence contains all the relevant information which must be taken into account in order to assess a complex situation and whether it is capable of substantiating the conclusions drawn from it.

118 In the present case, it must be stated, as Ryanair has done, that, in the period preceding the adoption of the contested decision, the Lufthansa Group owned 86% of its fleet of 763 aircraft, that 87% of the aircraft it owned were unencumbered, and that the book value of that fleet was approximately EUR 10 billion. Those findings emerge in a clear, unequivocal and consistent manner from several items of evidence in the file in Case T‑34/21, namely a statement of 19 March 2020 by the chief financial officer of DLH itself, the Oxera report I and the Moody’s and Exane reports. The Oxera report I and the Moody’s report also show that DLH was able to use its fleet as collateral in order to raise funds on the financial markets.

119 Furthermore, the Oxera report I states that the book value of the Lufthansa Group’s spare parts was EUR 2.3 billion at the end of 2019. That report also shows that, taking into account a potential asset value decline of 20% to 50% due to the COVID-19 pandemic and a loan-to-value ratio (LTV) of 40% to 60%, DLH could have raised between EUR 1 and 3.7 billion in debt financing by using its aircraft and spare parts as collateral.

120 The Commission and the interveners do not dispute the accuracy and reliability of those data.

121 In addition, it is apparent from the documents before the Court that Ryanair had drawn the attention of both the German Government and the Commission to that evidence, and in particular to the statement by DLH’s chief financial officer referred to in paragraph 118 above, even before the contested decision was adopted, by letters of 1 April 2020 and 3 April 2020 respectively.

122 In the contested decision the Commission merely asserted that DLH did not have ‘sufficient collateral’ to obtain financing instruments on the markets ‘over the entire amount’ of the aid.

123 However, first, the Commission did not substantiate that assertion in any way. There is nothing in the contested decision to indicate that the Commission assessed the possible availability of collateral, such as DLH’s unencumbered aircraft, their value and the terms for any loans that it may have been possible to obtain on the financial markets against such collateral.

124 Yet that is an important aspect of the condition laid down in point 49(c) of the Temporary Framework. An evaluation of an undertaking’s inability to obtain financing on the markets at affordable terms implies determining, in particular, whether that undertaking could offer collateral allowing it to have access to such financing. Furthermore, the terms for such financing depend, inter alia, on the type and value of such collateral. There is nothing in the contested decision to show that the Commission examined those issues.

125 Second, the Commission’s assertion in paragraph 22 of the contested decision that the ‘collateral’ – not specified in the contested decision – would not be sufficient to cover the ‘entire amount’ of the funds necessary is based on a false premiss, that the financing that can be obtained on the markets must necessarily cover all the beneficiary’s needs.

126 In that regard, it must be observed, as Condor has done, that the Commission’s reference in paragraph 22 of the contested decision to a total amount of ‘EUR 9 billion’, as the amount that DLH would allegedly be unable to obtain on the markets, does not match the amount of the measure at issue, determined at EUR 6 billion (paragraph 26 of the contested decision). Consequently, the Commission in any event based its assertion on a higher amount than that constituting the object of the measure at issue, which calls into question the very basis of its assessment.

127 Furthermore, neither the wording, purpose or context of point 49(c) of the Temporary Framework provide support for the view expressed by the Commission in paragraph 22 of the contested decision.

128 There is nothing in the wording of point 49(c) of the Temporary Framework to show that the beneficiary must be incapable of finding financing on the markets for the entirety of its needs.

129 As regards the purpose of point 49(c) of the Temporary Framework and the context of which it is part, it should be observed that that condition is intended to limit State intervention and, thereby, the use of public resources, solely to those cases where the beneficiary is unable to obtain financing on the financial markets at affordable terms. That purpose would be undermined if public resources were to be spent in order to cover the totality of the funding needed by the undertaking concerned, even though it was capable of obtaining a non-negligible part of its needs, on the markets.

130 That finding is corroborated both by point 44 of the Temporary Framework, which states that recapitalisations must not exceed the minimum needed to ensure the viability of the beneficiary, and, more widely, by the general principle of proportionality, which requires that measures adopted by EU institutions must not exceed what is appropriate and necessary to attain the objective pursued (see, to that effect, judgments of 17 May 1984, Denkavit Nederland, 15/83, EU:C:1984:183, paragraph 25, and of 19 September 2018, HH Ferries and Others v Commission, T‑68/15, EU:T:2018:563, paragraph 144 and the case-law cited).

131 Furthermore, the Court has had occasion to hold that, in presuming that no financial establishment would act as a guarantor for a firm in difficulty, and, therefore, that no corresponding guarantee premium benchmark could be found on the market, the Commission, inter alia, failed to fulfil its obligation to carry out an overall assessment, taking into account all the relevant evidence in the case enabling it to determine whether the beneficiary would manifestly not have obtained the necessary financing on the markets (see, to that effect and by analogy, judgments of 12 March 2020, Elche Club de Fútbol v Commission, T‑901/16, EU:T:2020:97, paragraph 132, and of 12 March 2020, Valencia Club de Fútbol v Commission, T‑732/16, EU:T:2020:98, paragraph 134). It follows that the Commission cannot presume, without substantiating its findings to the requisite legal standard, that an undertaking, such as the beneficiary in the present case, would not have access to the financial markets.

132 In the present case, the Commission failed to assess whether the beneficiary could have raised a non-negligible part of the necessary financing on the markets. It therefore failed to take into account all of the relevant evidence for the purpose of examining the condition laid down in point 49(c) of the Temporary Framework.

133 None of the arguments put forward by the Commission calls that finding into question.

134 First, the Commission’s argument that it would have been impossible for DLH to obtain possible financing on the markets, including against the collateral referred to in paragraphs 118 and 119 above, in a short period of time and in the financial context affected by the COVID-19 pandemic, cannot succeed. The contested decision does not show that the Commission analysed the time required for obtaining possible financing on the markets against that collateral. In addition, according to the statement by DLH’s chief financial officer of 19 March 2020, the Lufthansa Group was ‘financially well equipped to cope with an extraordinary crisis situation such as [the COVID-19 crisis]’, in particular because it owned ‘[86%] of the Group’s fleet, which is largely unencumbered and [had] a book value of around [EUR] 10 billion’. Moreover, the Oxera report I factors in a significant decrease in the value of its collateral precisely because of the pandemic.

135 Second, the Commission criticises the applicants for failing to demonstrate that DLH could obtain such financing on the markets ‘at affordable terms’. However, it is for the Commission to demonstrate, as required by point 49(c) of the Temporary Framework, that the beneficiary is not able to find financing on the markets at affordable terms. An applicant cannot be required to carry out tasks which, properly speaking, belong to the instruction and investigation of the case (see, to that effect and by analogy, judgment of 9 April 2019, Qualcomm and Qualcomm Europe v Commission, T‑371/17, not published, EU:T:2019:232, paragraph 171). In the present case, the contested decision did not in any way examine the conditions in which the beneficiary could have obtained financing, if at all, on the markets against the abovementioned collateral.

136 Furthermore, as Ryanair submits, the Commission’s argument amounts to imposing an unreasonable burden of proof on the applicant by requiring it, in reality, to produce a private funding offer addressed to DLH in order to establish the conditions in which such financing would have been available to it. However, it is not permissible to impose an unreasonable burden of proof on an applicant (see, to that effect and by analogy, judgment of 8 July 2008, Huvis v Council, T‑221/05, not published, EU:T:2008:258, paragraph 78).

137 Accordingly, it must be found that the Commission failed to take account of all the relevant evidence that must be taken into consideration in order to assess the compliance of the measure at issue with point 49(c) of the Temporary Framework.

138 Consequently, the complaint made by Ryanair based on an infringement of point 49(c) of the Temporary Framework must be upheld, as must, as a result and a fortiori, that of Condor alleging the existence of serious doubts in that regard, without it being necessary to examine their other arguments put forward in relation to this issue.

3. The existence of other measures that were more appropriate and less distortive to competition

139 Ryanair argues in essence that the Commission infringed point 53 of the Temporary Framework in that it failed to examine whether the measure at issue was the most appropriate and the least likely to distort competition. Accordingly, the Commission did not compare the recapitalisation instruments available and did not analyse the distortions to competition generated by the measure at issue or by ‘other possible aid instruments’.

140 The Commission, supported by DLH, contests Ryanair’s arguments.

141 Section 3.11.3 of the Temporary Framework, entitled ‘Types of recapitalisation measures’, contains points 52 and 53. Point 52 sets out the recapitalisation measures that the Member States may adopt during the COVID-19 pandemic, namely equity instruments, in particular the issuance of new common or preferred shares, and instruments with an equity component (referred to as ‘hybrid capital instruments’), in particular profit participation rights, silent participations and convertible secured or unsecured bonds.

142 Point 53 of the Temporary Framework states:

‘The State intervention can take the form of any variation of [those] instruments, or a combination of equity and hybrid capital instruments. … The Member State must ensure that the selected recapitalisation instruments and the conditions attached thereto are appropriate to address the beneficiary’s recapitalisation needs, while at the same time being the least distortive to competition.’

143 In paragraphs 104 to 108 of the contested decision, the Commission described the recapitalisation measure at issue, explaining that it was a combination of equity and hybrid capital instruments. It observed, in particular, that the silent participation was a flexible instrument as regards the participation of the silent partner in the profits and losses of the beneficiary or in its decision-making. The Commission also explained that neither the ESF nor DLH had any interest in the ESF holding more than 20% of the equity capital, which is why they had chosen the specific structure of the recapitalisation at issue. According to the Commission, the combination of the instruments chosen would make it possible to restore the capital structure of DLH and allow it to return as soon as possible to the capital markets, while limiting the State participation to the minimum necessary to protect the financial interests of Germany, without acquiring control over DLH.

144 In the present case, it must be stated, as the Commission has done, that a recapitalisation measure and the conditions attached thereto may be regarded as being appropriate to address the recapitalisation needs of the beneficiary concerned, while being the least distortive to competition, in terms of point 53 of the Temporary Framework, as long as they meet the various requirements laid down for that purpose in that framework, which relate to the amount of the recapitalisation, the remuneration and exit of the State, governance and the prevention of undue distortions to competition, and to the exit strategy of the State from the participation resulting from the recapitalisation. The reference in point 53 of the Temporary Framework to the ‘conditions attached [to the measure at issue]’ refers to requirements, such as those mentioned in the previous sentence, whose very purpose is to ensure that the measure at issue and the conditions attached thereto do not exceed what is appropriate to address the recapitalisation needs of the beneficiary concerned, while being the least distortive to competition. Consequently, if the abovementioned requirements are satisfied, the recapitalisation instrument chosen must be regarded as complying with point 53 of the Temporary Framework.

145 As a result, this complaint is tributary to the arguments raised by Ryanair in the other parts of its first plea, which concern some of the other requirements referred to in paragraph 144 above, namely the amount of the recapitalisation (third part of the first plea), the remuneration and exit of the State (fourth part of the first plea), and also governance and the prevention of undue distortions to competition (fifth and sixth parts of the first plea). The merits of the present complaint are therefore dependent on the review of those other parts of the first plea, which are examined below.

146 In so far as Ryanair, in the reply and at the hearing, also appears to criticise the Commission for having failed to examine whether a type of aid measure other than a recapitalisation would have been more appropriate and less likely to give rise to distortions to competition, it must be held, without prejudice to the admissibility of that line of argument, that it is too general and abstract. In its written pleadings, Ryanair simply referred to ‘other possible aid instruments’, without, however, explaining exactly what those other instruments were and why they would be more appropriate and less distortive to competition than the notified measure. At the hearing, Ryanair stated that in its view the Commission should have taken account of ‘the entire universe of alternative funding options that were available’ and ‘all available options’, while referring, without any further explanation, to bridging or short-term loans as a possible alternative to the notified measure.

147 However, according to the case-law, the Commission is not required to take a decision on every other possible aid measure. It is not required to prove, positively, that no other conceivable aid measure, which by definition would be hypothetical, would be more appropriate and less distortive to competition (see, to that effect and by analogy, judgment of 6 May 2019, Scor v Commission, T‑135/17, not published, EU:T:2019:287, paragraph 94 and the case-law cited).

148 It is true, as Ryanair states, that the Court of Justice has also held that when there is a choice between several appropriate measures, recourse must be had to the least onerous, and the disadvantages caused must not be disproportionate to the aims pursued (see judgment of 22 January 2013, Sky Österreich, C‑283/11, EU:C:2013:28, paragraph 50 and the case-law cited). However, there is nothing in the present case to indicate that the Commission was faced with a choice between several appropriate measures, as set out in that case-law.

149 Accordingly, the argument that Ryanair seems to put forward, which is summarised in paragraph 146 above, must be rejected as unfounded.

4. The amount of the aid

150 In the third part of its first plea, Ryanair, in essence, raises three complaints concerning the amount of the aid, related, first, to the interpretation of point 54 of the Temporary Framework, second, to the application of that point to this case, and third, to certain public statements made by DLH. That last complaint and a similar one raised by Condor in the second part of its first plea overlap.

(a) Interpretation of point 54 of the Temporary Framework